A beginner's guide to investment products

- Aim to achieve your goals and be open to adjusting your current lifestyle.

- Understand the reasons for an adviser's recommendations.

- Be active in your questioning.

A good financial adviser will only recommend suitable investments applicable to your financial objectives. These could be shares, property, managed funds, fixed income and cash.

As part of this process, the adviser may need to refer you to other professionals, such as solicitors for estate planning matters, stockbrokers for buying shares/equities, and accountants for setting up business structures and tax advice.

The following discussion examines the popular investment categories and strategies that an adviser will explore with you.

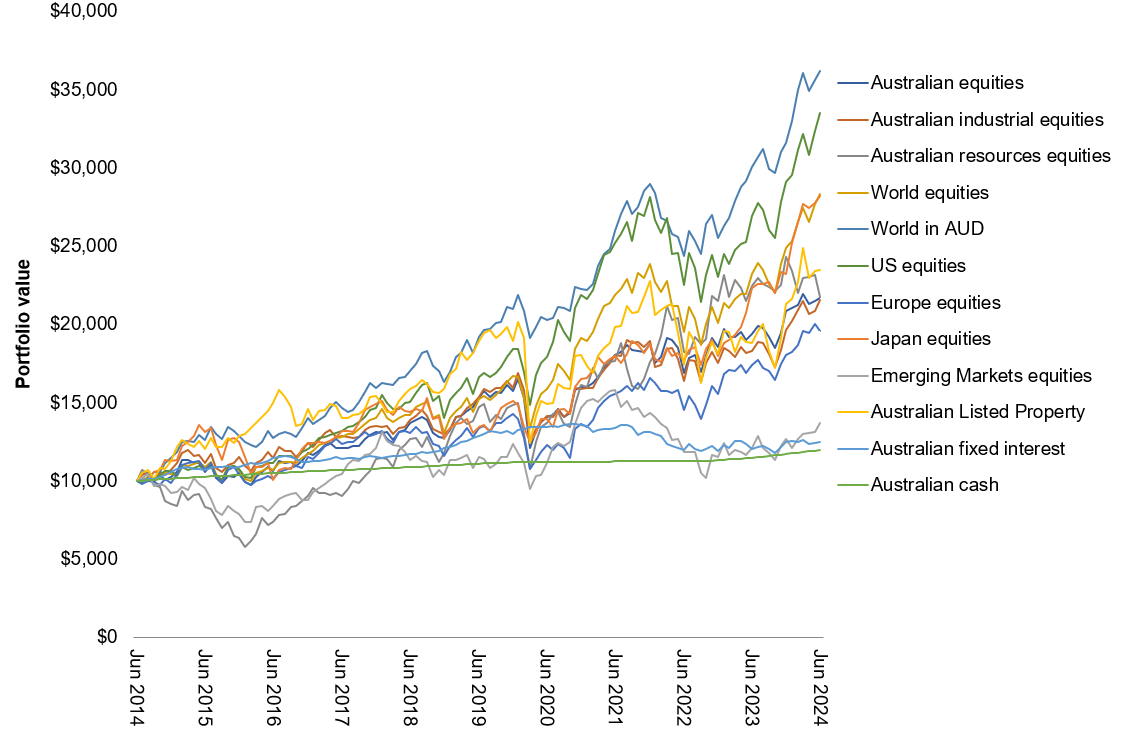

It's important to look at whatever investments you choose as a long-term investment venture, and avoid becoming fixated on short-term performance.

The table below shows how various asset classes have fared over a 10-year period, based on an initial investment of $10,000. The key takeaway is that they all grew over this period, even though there were peaks and valleys along the way.

Performance of various asset classes over 10 years

Cash reserves

The purpose of holding a cash reserve is to reduce the likelihood that longer-term growth investments will need to be sold at unideal times to meet short-term capital requirements.

Investing directly in shares

Share investing is generally a long-term exercise, typically for at least seven years. Historically, shares have outperformed all other asset classes over the medium to long term. While values may have risen over the long term, they often experience periods of short-term volatility, causing share prices to fluctuate.

Investing in managed funds

When you invest in a managed fund, you don't own the underlying assets directly. Instead, you own 'units' in the fund. Managed funds allow investors to pool their money with an investment manager who has extensive research resources and experience. This allows you to take advantage of growth investments, such as Australian and international shares through the power and scale of pooled funds.

A regular savings plan and managed funds

A regular savings plan using a managed fund would enable you to invest your surplus income on a flexible basis and allows you to benefit from buying units of investment at different prices to help reduce the risk of mistiming the market.

Exchange-traded funds (ETFs)

An exchange traded fund (ETF) is a type of managed fund that you can buy or sell on an exchange such as the Australian Securities Exchange (ASX). When you invest in an ETF you don't own the underlying securities, you own units in the ETF and the ETF provider owns the shares or assets.

ETFs portfolios are designed to replicate specific indexes such as the S&P/ASX 200 or the S&P 500 in the US market. ETF portfolios may include Australian shares, international shares, fixed income securities, listed property trusts or a combination of asset classes.

Gearing your investments

Gearing your investments simply means borrowing money to invest. Gearing may be used to accelerate the wealth-creation process by allowing you to make larger investments than would otherwise be possible. The borrowed money can be invested in a number of ways, including shares, property and managed investments.

Caution! You may have to deal with a margin callA poorly performi ng market generally means losses, which will be magnified by gearing. Losses can result in margin calls. A margin call is a situation where the lender will contact you to add money or securities to your account. Generally, this happens if the value of your portfolio falls below an agreed percentage of the loan. |

Investment bonds

Investment bonds (sometimes referred to as 'insurance bonds') allow you to avoid the annual tax return associated with many investments because tax is paid on the earnings by the investment fund itself. If these bonds are held for 10 years or more, you are able to withdraw the value of the bond with no further tax payable. Each year, contributions can be up to 125% of the previous year's contribution without restarting the tax-free period.

If the investment is withdrawn before 10 years, you will receive a tax rebate that can be used to offset any additional tax payable. Insurance bonds are frequently used to help pay for children's education.

Managed accounts

A managed account or separately managed account (SMA) is a portfolio of assets that is administered by a professional manager to achieve specific income and/or growth objectives on behalf of you, the investor.

Superannuation

Superannuation is one of the most tax-effective ways to accumulate wealth and save for retirement. Superannuation aims to maximise the growth and tax benefits of your investment dollar and is among the most attractive investment structures currently available.

Here are some popular strategies to increase your wealth in superannuation:

- Increasing your concessional contributions. These are pre-tax contributions paid into your superannuation account that are subject to a lower, or concessional, tax rate (e.g. your employer's compulsory contributions). Currently, there's a yearly cap of $30,000 (this includes your superannuation guarantee (SG) and salary sacrifice contributions).

- Making non-concessional contributions (NCCs). These are contributions made by you to the superannuation environment for which you are not entitled to a tax deduction-NCCs are made using after-tax income and limited to $120,000 per year.

Why make NCCs?You may have money on which you've already paid tax. So, why would you put this money into a superannuation environment where it will be taxed again? Because the earnings on your contributions will be taxed at 15% in a superannuation environment as opposed to potentially more if it's invested outside superannuation. If you are self employed If you are self-employed or work on a contractual basis, you may not receive employer-sponsored (that is, SG) contributions to superannuation. Therefore, NCCs can be a worthwhile way to increase your superannuation savings. |

Carry-forward or 'catch-up' concessional contributions

It may be possible to carry forward unused concessional contribution (CC) cap amounts from previous financial years and use them to make additional or 'catch-up' CCs in the current and/ or future financial years. The current CC cap is $30,000 for the 2025-26 financial year.

Your eligibility is based on having:

- a total superannuation balance (TSB) of less than $500,000 on June 30 of the previous financial year, and

- unused CC cap amounts from up to five previous years, after which they expire.

This potentially allows you have a higher CC cap in the current financial year if you didn't use up the applicable cap in one or more of five previous years.

The bring forward rule

The bring-forward rule The bring-forward rule enables people under age 75 to make up to three years' worth of NCCs to their superannuation in a single income year. Essentially, they are bringing forward their annual caps and can put up to $360,000-three times the current $120,000 annual NCC-into their superannuation in a single financial year and not pay additional tax.

What is the superannuation guarantee?The superannuation guarantee (SG) requires your employer to contribute a minimum percentage of your earnings to a superannuation fund. The rate is 12% for the 2025-26 financial year. |

Government co-contribution

This gives low-income earners the opportunity to have their personal superannuation contributions matched by 50 cents for each dollar contributed, by the Australian government up to a maximum of $500.

Spouse contribution

You are allowed to contribute on behalf of your spouse to their superannuation fund and receive a tax rebate. Eligible spouse contributions are treated as after-tax contributions. This means that because they are made after tax has already been taken out, there is no more tax to pay when the contribution is initially made. The partner making the spouse contribution may be eligible to receive a tax offset of up to $540 in each financial year.

Downsizer contribution

The downsizer contribution provides a possible way to help manage retirement income. From January 1, 2023, individuals aged 55 or older may be able to choose to make a downsizer contribution into their superannuation of up to $300,000 from the proceeds of selling their home. However, there are a number of eligibility requirements which can be found on the ATO's website (ato.gov.au).

Income streams

Having adequate income throughout your retirement is a fundamental part of enjoying this stage of life. Retirement income streams are a popular way of receiving regular tax-free income payments in retirement.

Here's a list of potential retirement income streams:

- Account-based pension (ABP)-an ABP is an income stream paid from your superannuation savings and can only be purchased with money held in superannuation. It provides tax-effective retirement income as well as the opportunity to achieve tax-free capital growth and earnings on your investment. There are minimum amounts that you must withdraw each year, based on your age and a set percentage of your account balance as at June 30 each year. The prescribed minimums or "drawdown rates", can be found on the Moneysmart website (moneysmart. gov.au). Search for "retirement income account-based pensions".

- Lifetime pension or annuity-a guaranteed lifetime income stream. In some cases, it may also be payable to your spouse if you die. These are purchased with non-superannuation money.

- Life expectancy or fixed-term pension or annuity-a guaranteed income stream payable for a fixed term that you choose, which can be based on your life expectancy.

Insurance cover

Personal insurance, such as life (death) cover, total and permanent disability (TPD), trauma and income protection, is a key part of an overall financial strategy. These types of insurance are designed to protect you or your family's current living standards in the event of death or disablement, trauma, an illness or injury that prevents you from earning an income.

Here's a list of the types of cover a financial adviser may look at recommending:

- Income protection-provides a monthly income benefit in the event that you are unable to work as a result of sickness or accident.

- Life and TPD-life cover pays a lump sum if you die or are diagnosed with terminal illness and have 12-24 months (depending on the insurer) or less to live. TPD provides a lump sum payment if you suffer an illness or injury that totally and permanently prevents you from working again.

- Trauma-payment of a lump sum in the event that you are diagnosed with/suffer from a major medical condition (e.g. a heart attack) covered by your insurance policy.

ConsiderLife insurance often relates to unplanned events, which can have serious emotional and financial impact on your current lifestyle. |

Life insurance 'riders'

Some life insurance policies offer riders such as a child trauma or critical illness cover. This provides a payment to you if your child suffers a specific medical condition and you need to take time off work to look after them. It also applies if your child passes away.

A knowledgeable adviser will provide information about these riders to help you make an informed decision.

Purchasing income protection, life and TPD insurance inside or outside superannuation?

The insurances listed above can be purchased either inside or outside of superannuation.

Default funds are used by employers to make superannuation payments if employees have not nominated a superannuation fund or do not have an existing or 'stapled' fund. As part of the federal government's MySuper requirements, default funds must offer simple, cost-effective products.

Further, there is a legislative obligation on default funds to provide a minimum level of insurance cover. However, members under age 25, or whose account balance is under $6,000, will have to specifically 'opt-in' to be able to qualify for automatic (default)

insurance through their superannuation fund.

However, once you are age 25 and over and you do not make contributions over a certain time period or your balance falls below $6,000, your fund may cancel your insurance after supplying due notification.

Further, depending on your choice, there are considerations that a good financial adviser should bring to your attention.

Purchasing income protection, life and TPD insurance inside or outside superannuation?

The insurances listed above can be purchased either inside or outside of superannuation. However, depending on your choice, there are considerations that a good financial adviser should bring to your attention.

Centrelink and social security

An adviser will analyse your financial strategy and decide if it is necessary to take into account any Centrelink benefits that you may be eligible to receive.

Centrelink applies an assets test and an income test to determine the amount of social security benefits you may be eligible for. The lower calculated benefit payable under each of these tests will be the actual benefit received. If the lower calculated benefit is nil, no benefit is payable.

Here's a list of some potential benefits you may be eligible to receive:

- Age Pension-a safety net for people who are unable to fully provide an income for themselves in retirement. The Age Pension can be part or whole, depending on your income and assets.

- Commonwealth Seniors Health Card-available to independent but low-to-middle income retirees who have reached Age Pension age or Service Pension (a payment for veterans and their partner's) age.

Estate planning

Estate planning is the process of making sure your assets are distributed in accordance with your wishes after your death. If you don't have a Will, this process can be complicated, or the distribution of your assets may not reflect your intentions. For instance, your children, dependants or intended charity may receive less than you wanted.

Other estate planning considerations include powers of attorney, trusts and non-estate assets.

The Financial planning and families section of this guide contains a more detailed discussion of these aspects in a family context.

Taxation

In order for an adviser to provide advice on the tax consequences of their recommendations, they must be registered with the Tax Practitioners Board (tpb.gov.au).

| Getting your head around financial planning jargon |

| How much does financial advice cost? |