Managed fund fees - how much and getting what you pay for

- The more fees you pay, the higher your investment returns must be to make up for them.

- While there are many types of fees, you can group them together to derive your overall total expense ratio.

- Paying higher fees does not get you better investment returns. Managed funds are investment pools run by investment experts.

- Every extra 1% you pay in fees each year will cost you 10% of your potential investment over a 10-year period.

- The indirect cost ratio (ICR) is another term used to describe investment fees.

To understand how much you are really paying in managed fund fees, you have to demystify the different types of fees funds might charge you. The good news is that it is not as complex as it seems.

Your aim in selecting a managed fund is to find one that will make you as wealthy as possible by the time you withdraw your money, without exposing you to too much unnecessary investment risk along the way. To do this, your fund must earn consistently strong rates of investment returns - year in, year out.

Fees affect your investment returns

To give you a better chance of building your retirement savings, it helps if your managed fund charges reasonable fees. Why? Because what you get in your pocket is what's left from the investment returns after all the fees are taken out; it is no more complicated than that. So the higher the fees, the higher the returns have to be to leave you with more money in your pocket.

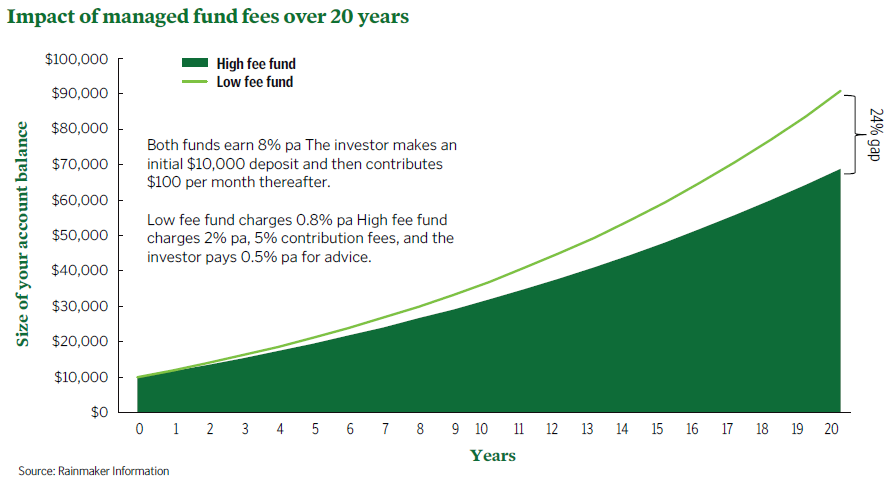

An example will highlight why this is so important to understand. If two investors achieve identical investment returns but one pays only 1% in fees each year while the other pays 2% in fees each year, then the member in the fund with the higher fee will have 10% less in their account after 10 years and 19% less after 20 years.

So paying higher fees can cost you big money. And this means if you are paying higher fees, you should make sure you use the managed fund shrewdly so that you more than make up the fees through better investment mixes that lead to higher investment returns.

All about the fees

There are six main types of managed fund fees you should know about:

- Establishment fees, also known as entry or upfront fees, may be paid when you set up your managed fund account.

- Contribution fees may be paid each time you make a deposit

- Management fees are paid to your fund's responsible entity to manage the fund. This fee usually includes the feeds paid to the investment managers. This fee is sometimes call the indirect cost ratio (ICR).

- Performance fees are bonus fees paid if the managed fund's investment performance is very high (for example, it exceeds its benchmark by, say, five percentage points).

- Adviser service fees may be paid to your financial adviser or broker each year for the advice and support they provide.

- Buy/sell spreads are transaction fees the investment manager may charge when you buy more units in the managed fund or redeem units.

These different fee types mean that the different people involved with your managed fund are getting a different share of your fees. For example, in many managed funds, the investment managers may only be receiving one-third of the total fees you are paying, which means there is no point blaming them for your high fees because they are rarely the cause of the problem.

A fee people love to hate is the contribution fee. This fee, if you are paying it, usually goes to your financial adviser or broker to cover the cost of talking to you and providing some basic financial advice. You can often get a discount on this fee if you ask for it or if you are contributing a large amount of money into your managed fund.

When a managed fund or a financial adviser or broker is willing to discount fees for you, this is sometimes called dialling down your fees. But if the fees dial down so much that the fund, adviser or broker don't believe they are being properly paid, then don't expect too much service from them. It's one of those balancing acts you have to navigate when choosing a managed fund.

There are some tricks of the trade you should watch out for when it comes to fees and charges.

For example, beware of managed funds that try to confuse you by talking about fees charged to the fund and how they are different from fees charged directly to you. Anything that comes off the top of your investment return before you receive it is a fee to you - no ifs, no buts. Funds that do this aren't being dishonest, but they aren't being as transparent as they should be either.

Do not chase high returns by paying high fees because there is no evidence that paying higher fees buys better investment returns. Instead, research shows that paying higher fees usually only gets you more investment choices.

The Good Investment Guide fee calculator

If you wish to compare managed fund fees, you should use The Good Investment Guide fee calculator, which converts all the fees you are paying into a single dollar amount.

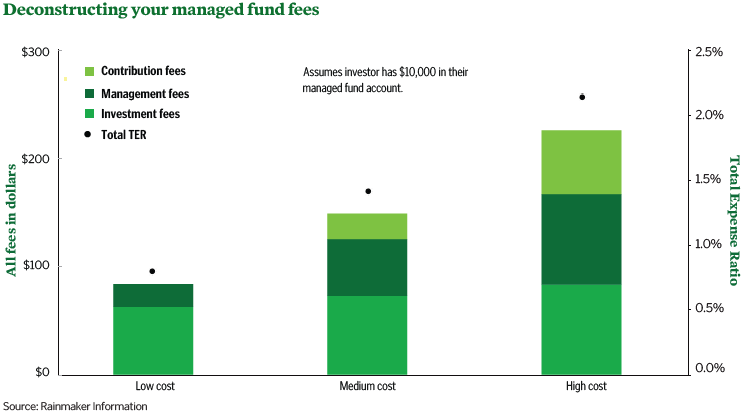

It then applies that amount to your overall account balance to come up with your total fee as a percentage of your account balance. We call this percentage your total expense ratio or TER. Knowing the different fees charged by different managed funds means you can calculate the different TERs. It is important to realise, however, that a TER does not indicate the future performance of a managed fund - but we do know that higher fees rarely lead to better investment returns, and many of Australia's top-performing managed funds usually have low fees anyway. Why pay higher fees if you don't have to?

The TER calculator demonstrates that the biggest fee culprit is the management fee, because it is usually the highest, while the fees with least impact are usually the contribution fees. This is because contribution fees, while they sound nasty, apply to contributions and not the account balance. This means they are not a major problem unless you pay

them when making a big initial deposit, such as transferring in a retirement lump sum.

If you want to receive a deal on your managed fund fees, you will get the best results if you dial down the management fees. It is, of course, good if you can dial down the other fees, too, but it's the management fees that you should worry about first.

While the average managed fund member across Australia pays a TER of about 1.5%, this covers everybody. This means that if you are in a managed fund charging less than 1%, you are in a very sharply priced fund. However, some very expensive funds can charge more than 2%. If you are paying high fees then you should be getting something very special, such as top-quality financial advice, a great range of extra features and lots of investment choices - and these features should be translating into higher returns.

What to expect from your managed fund

Your fund must describe the fees it charges in the product disclosure statement (PDS) in an easy-to-read table in the key features statement. This can usually be found towards the front of your investor booklet. Look for the section on fees and charges. If you don't have this booklet, check out your managed fund's website or call them and ask for a copy to be sent to you.

If your managed fund doesn't have a section in its PDS or website that describes all the fees, this is a red flag suggesting you should use another fund. The Commonwealth Treasury and ASIC have devised a template for funds to follow. It is compulsory for managed funds to use this template when describing their fees, so if a fund you are thinking about using isn't following these fee disclosure guidelines, then do not join. Poor fee disclosure is a very bad sign in a managed fund.

Also remember that your fund's rate of return described in your member statement is the figure left after all the fees are taken out (or it should be). If your rate of return is low, it may be that you are paying too much in fees. Conversely, just because fees are high doesn't necessarily mean your rate of investment return after fees is low either.

Indirect cost ratio

Some managed funds no longer declare investment fees and instead refer to indirect cost ratios (ICR). They use this term because these charges may not be paid directly by you to the managed fund, but indirectly because the investment manager's fee is deducted from the investment return before the unit price is calculated. For example, the investment manager may achieve a 10% investment return for the managed fund but their fee is 1%, so the net return applied to the managed fund is 9%. When you see an ICR, just think of it as another way to describe the embedded investment fee.

Managed fund fee types

| Description | Applies to | Who gets it | What's normal | Negotiable |

| Establishment How much it costs to set up your account. |

Initial deposit | Your financial adviser or broker | 0 to 5% | Yes |

| Contribution How much it costs each time you contribute money into your managed fund. |

Contributions | Your financial adviser or broker | 0 to 5% | Yes |

| Management How much it costs to stay in the managed fund. |

Account balance | The fund, but sometimes shared with the adviser | 0.5% to 1.5% | Usually |

| Investment or indirect cost ratio How much you have to pay to your investment manager. |

Account balance | Investment manager | 0.15% to 1.5% | Rarely |

| Performance Bonus fee paid to your investment manager if they do very well. |

Account balance | Investment manager | 0.1% to 0.5% | Rarely |

| Buy/sell spread How much it costs to enter or withdraw money from the managed fund. This is a form of contribution or exit fee. |

Account balance | Fund and investment manager | Up to 0.30% | Rarely |

| Who runs a managed fund? |

| Managed fund units and unit prices explained |