Being loyal to your lender could cost you $119k

Australian homeowners with a mortgage are paying a high price for their loyalty and apathy, with lenders increasingly prioritising new borrowers over existing customers by way of lower interest rates.

The latest data from the Reserve Bank shows that the gap between the variable interest rates being offered by lenders on new loans compared to outstanding loans - often dubbed the 'mortgage loyalty tax' - grew to 51 basis points in December.

For comparison, the gap was 40 basis points in December 2021 and 33 basis points in December 2019.

As Angus Gilfillan, chief executive of digital mortgage broker Finspo explains, there are a couple of reasons behind the steady growth in the home loan loyalty tax in recent years.

"In late 2021, new fixed rates started increasing from their record low levels and lenders started competing more heavily on variable rates for new customers, leaving existing customers on their relatively higher rates.

"And when the RBA started increasing the official cash rate in May 2022, lenders generally passed on the full interest rate increase to existing customers but tended not to increase the price for new customers by the same amount."

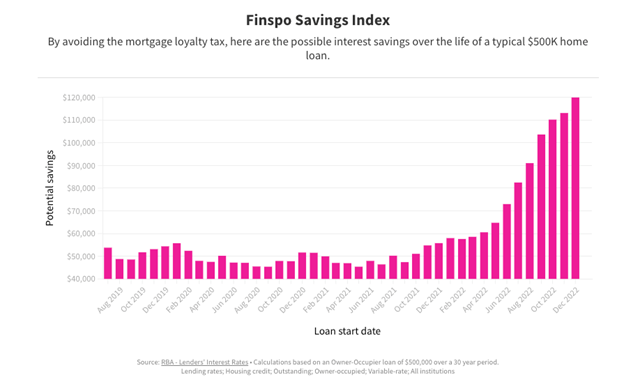

The price of loyalty

At first glance 51 basis points might not seem like a huge gulf between two interest rates, but over the life of a loan it could translate into a difference in the tens or even hundreds of thousands of dollars.

Take, for instance, an owner-occupier with a $500,000 mortgage being paid off over 30 years with principal and interest repayments. According to the Finspo Savings Index, by avoiding a loyalty tax of 51 basis points, that borrower could save up to $119,971 (or $378 each month) over the course of the loan.

And it appears that plenty of mortgage customers are choosing to walk away from their existing lenders in favour of a better deal. Borrowers refinanced $19.1 billion worth of loans in December, figures from the Australian Bureau of Statistics show, which was just shy of the $19.4 billion record set in November.

But how can borrowers work out if they're paying more than they should be - and potentially benefit from refinancing - in the first place?

"Refinancing can be a great way to ensure you get a competitive rate on your home loan, however, a great place to start is knowing what rate you are currently paying and how your rate stacks up compared to what new customers in the market," says Gilfillan.

"If you are on a variable rate for more than a year or two and haven't reviewed your loan with an expert like Finspo, chances are you are paying a loyalty tax. The longer it has been since you had your loan reviewed, the bigger the likely tax you are paying (and saving you could achieve by fixing it)."

Smaller lenders offer sharpest rates

For those variable rate borrowers who haven't shopped around in recent years, there are likely to be plenty of interest rates on the market more competitive than their existing rate. However, that doesn't mean that it's worth signing on with the first lender offering a sharper rate.

"Refinancers should be looking beyond the big four banks, with our database showing the most competitive rates are being offered by online lenders and smaller lenders like mutual and customer-owned banks," says Claire Frawley, personal finance expert at financial comparison website Mozo.

Frawley also says that borrowers who have built up equity in their homes should look out for offers providing rate discounts for lower loan-to-value ratios (LVRs) - discounts that tend to be available for LVRs below 70% or 60%.

Beyond the interest rate on offer and other potential refinancing perks like cashback deals, there are a few other considerations that Frawley recommends borrowers take into account before switching.

"When refinancing it's really important to look at the length of your existing loan and make sure you are either refinancing for the same amount of time or shorter. Extending the length of your home loan could undo all your hard work of refinancing to a lower interest rate.

"An offset account is one feature to seriously consider when looking for a new home loan, as it can lower the amount of interest you pay on your loan."

Can all borrowers refinance?

As beneficial as refinancing can be, the reality is that it won't be an option available to all Australians with a mortgage.

In fact, the number of homeowners who will find it harder to take out a new loan with a different lender is likely to have increased over the past year. As Frawley explains, higher interest rates will have constrained the borrowing capacity of many of those looking to refinance.

"As interest rates continue to rise, so does the serviceability buffer applied to new customers, leaving many borrowers at a roadblock."

A drop in property values will also have pushed some mortgages over the 80% LVR mark. While that in itself doesn't completely rule out refinancing as a possibility, would-be refinancers in that situation would likely be required to take out lenders mortgage insurance to do so - an extra cost that would reduce the financial benefit of switching.

Gilfillan says that there may still be actions that borrowers who are not currently in a position to refinance can take to potentially reduce their loan costs though.

"Even if you're not able to refinance your loan today, there's still a lot you can do with your existing home loan such as renegotiating with your current lender, or looking at your loan term."

Interested in learning more about refinancing? Check out our run through on how to refinance your home loan and get a better interest rate, or see how much you could stand to save on your existing loan with the help of this mortgage switching calculator from ASIC's MoneySmart.

Get stories like this in our newsletters.