Fairfax and Domain: sum of the parts worth more than the whole?

Recently we saw the much-awaited spin-off of Domain from Fairfax Media. Domain Holdings Australia now trades on the ASX under the ticker DHG. Fairfax Media continues to own 60% of Domain, and we are upbeat on the shares, and the related ongoing value driver(s).

We remain of the view that the sum of the parts (Fairfax+Domain) will prove to be worth far more than the whole.

We believe that Domain will be increasingly priced for the valuable media property that it is. Fairfax retains a 60% holding in Domain, and will therefore benefit from any valuation uplift, as well as some positive tailwinds (despite a challenging environment) in other parts of the business.

This in our view seems very low, and the market is clearly not allowing for any improvement in the advertising cycle. That aside, earnings gains are also likely to come from further cost cutting, as well as the leveraging of the company's digital assets. This is also without allowing for the wild card of media reform leading to potential value enhancing M&A activity.

It also must be remembered that Fairfax has another high quality digital investment in Stan, a 50/50 joint venture with Seven. The business is similarly placed to Domain in so far as it is growing strongly, and is well positioned behind the incumbent streaming player in Netflix.

The traditional print publishing business in Australasia certainly remain under pressure, but management's efforts in controlling costs while steering the direction towards the digital space is starting to bear fruit. This was in evidence at the full year results, which delivered the best earnings performance in three years.

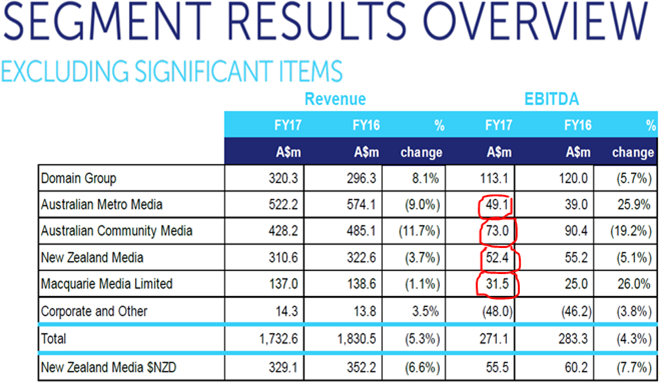

Lower circulation volumes likewise led to reductions in traditional advertising but all print divisions reported substantial double digit growth in the digital space, as Fairfax continued to ramp up the focus here. On the cost side, Fairfax has continued to make improvements in reducing expenses, having right-sized some units, not to mention streamlining some operational areas to improve efficiencies. A case in point is the AMM unit which saw a substantial transformation in EBITDA, reporting a 25.9% year-on-year increase to $49.1 million. Overall, the transformation efforts have reduced expenses by 5.7% to $1.46 billion.

An alternative for management to unlock value will be via acquisitions especially with the company's war chest from the spin-off of Domain. The investment in Stan also waits in the wings as a considerable value driver longer term.

Disclosure: Interests associated with Fat Prophets declare a holding in Fairfax.

Get stories like this in our newsletters.