Should you buy, hold or sell Roche shares?

Roche possesses several features that make it stand out as an attractive investment.

Why you should buy Roche shares

In addition to it being a dividend aristocrat (the dividend has grown every year for over 30 years) with a current dividend yield of 4%, it also has a diversified source of strong cash flows supported by patented pharmaceuticals.

We expect it to generate about $AUD26 billion per annum over the next few years even after accounting for annual research and development (R&D) spending of $AUD23.6 billion (~7.5% free cash flow yield).

The balance sheet is strong, with a net debt to EBITDA ratio of less than 1x in 2022.

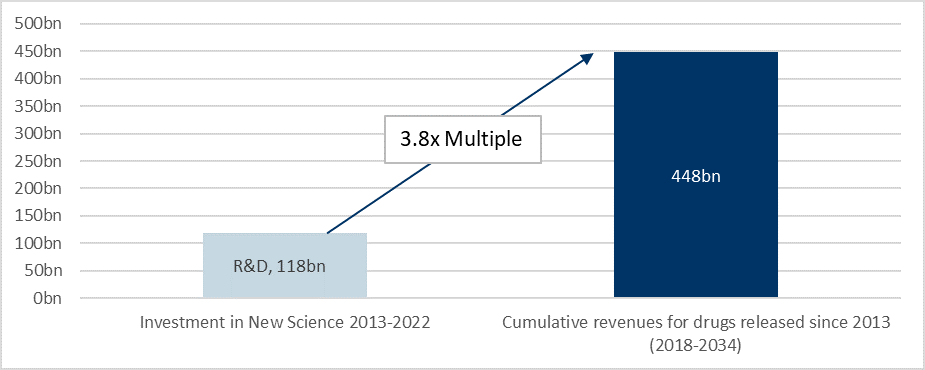

The value of New Science

Pharmaceutical companies strive to strike a fine balance between maximising cashflows from existing patent protected drugs ("Existing Science") and investing in the development of innovative new drugs ("New Science").

The money spent on New Science for pharmaceutical companies is significant. In 2020, European and US majors spent collectively $AUD164 billion on R&D of new drugs, equivalent to approximately 18% of revenues. Working out the effectiveness of R&D efforts is therefore critical in determining the value of a pharmaceutical company.

What Roche does

Roche is the largest pharmaceutical company by sales in Europe and the third largest in the world. Headquartered in Switzerland, the company has a diverse portfolio of innovative and life-changing medicines that treat a range of debilitating ailments from various forms of cancer to rheumatoid arthritis and multiple sclerosis.

One example is Ocrevus (10% of 2022 group sales), the most popular drug for treating Multiple Sclerosis (MS) in the world. It was first approved in 2017 and since then has significantly helped slow the progression of MS symptoms for hundreds of thousands of patients globally (there are 2.8 million people suffering from the disease worldwide).

Strategy and outlook

For 10 years starting in 2013 the company has spent a total of $AUD206 billion on R&D, (see Chart). To judge the productivity of these investments, we have taken the cumulative revenues generated by drugs that went into circulation after 2013.

The forecast period for sales extends to 2034 and the cumulative expected sales for the period are $AUD785 billion. This implies that investment in New Science has yielded 3.8x of revenues with reasonable certainty (all drugs in the analysis are already released, protected by patents and generating sales that are unlikely to deviate significantly from the projections).

With an average cashflow margin of 33%, it means that Roche is at the very least able to recover fully 1.2x the amount of money invested in New Science.

Returns

New Science for the past decade carried a 3.8x multiple of sales on investment or roughly 1.2x multiple of cashflows on investment. We expect the company to spend on average $AUD25.6 billion per annum on R&D over the next decade. The PV of this spending is equal to $AUD184 billion.

Bringing it all together, the fair value of Existing ($AUD343 billion) and New Science ($AUD220 billion, $AUD184 billion at 1.2x multiple) is equal to $AUD565 billion, or $AUD708 per share.

Today's share price in effect suggests 10 years of R&D spend will yield no commercially viable New Science in a stark contrast to the previous decade, making Roche an investment with a very attractive positive skew.

Get stories like this in our newsletters.