What to look for in a retirement product

There are six main factors that will indicate whether your super fund is good for retirees.

- After you retire, strong returns and low fees matter more than ever.

- You will pay up to two-thirds of all the fees you will ever pay to your super funds after you have retired.

- Because being a retired super fund member is more complicated than when you were still working, you need a super fund that will guide you through these issues and explain things to you.

Performance and investment choice

After you've retired your investment returns matter even more than when you were in your accumulation phase because you probably won't be able to make new contributions. You'll be completely reliant on your investment earnings to grow your account balance or protect it as much as possible from falling too quickly.

You probably won't be chasing high returns either because you'll instead be more focused on stable, reliable returns. This is why most retirees invest their superannuation into diversified growth, balanced or moderate investment options.

But you might still want to chance your arm with some money in asset classes such as international shares.

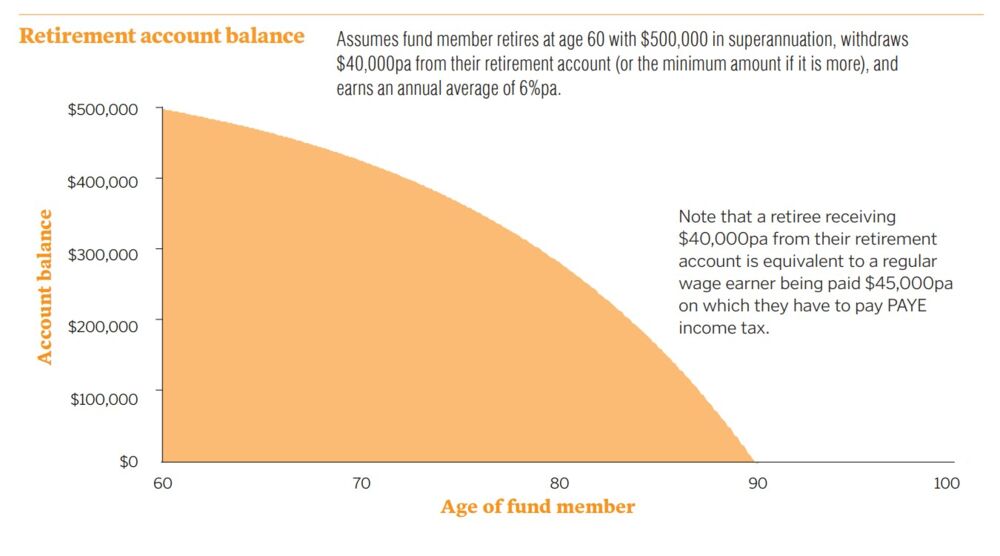

Because you have to withdraw a minimum of 4% from your retirement account each year, if you retire at age 60 with $500,000 in superannuation, if you earn only an average 6%pa, your account balance should be able to hold its value for many years longer than you expect.

Even if you withdraw at least $40,000pa as an income stream, your superannuation would likely still last until you were 82, after which you would be able to claim the age pension.

Apply for the age pension

When you retire and swap your superannuation account for a retirement account, don't forget to also apply for your age pension. Because age pension payments are made by Services Australia and not through your super fund, it's important that you don't just assume the super fund will do this for you.

Minimum amount you must withdraw from your super fund each year

Once you set up your retirement account with your super fund, you will be required to withdraw a minimum amount each year. This minimum amount is 4% of your account balance if you're younger than 65, rising to 5% if you're age 65-74, 6% if you're age 75-79, progressing up to 14% each year if your age is 95 or older.

Good value fees

Fees matter more than ever after you've retired for two very important reasons:

1. When you retire you'll probably have the most money in your superannuation account that you'll ever have in your life, so even seemingly low fees translate into large costs in dollars terms.

2. Of all the fees you will ever pay to your superannuation funds throughout your life, you'll pay up two-thirds after you've retired. Even if you pay the average retirement product fee of 1.1% on the average retirement account balance of about $235,900, that converts to almost $2600 in cold hard cash being taken from your account - equivalent to a month's full rate age pension. There are many smartly run full-featured retirement products that charge fees as low as 0.7%, and using one of these could save you almost $950 in fees each year; enough to pay for your car's annual registration and CTP insurance.

Online tools and education support

Being a retired super fund member is more complicated than when you're still working because of the web of social security, age pension, taxation, investment and superannuation rules. To help retired super fund members sort through these, many of Australia's best funds for retirees now host explainer fact sheets, podcasts, videos and webinars on their websites, on YouTube and podcast apps.

Many funds for retirees also have online calculators to help you plan, manage and understand your account balance, the pace at which it's reducing or growing and how this is impacted by your choice of investments. Some of these topics can be complex, so one of the hallmarks of a good super fund for retirees will be how well they explain these issues.

Flexible income stream products

When you retire you need regular income from your superannuation, and perhaps the age pension, to live on, help pay your bills and cover other regular expenses. There are different types of purpose-built retirement products tailor-made for this, ranging from account based pensions that provide you with investment-linked returns and lots of investment choice, to various forms of annuities that, while they might limit your investment choice, they guarantee that you'll keep receiving regular

income rain, hail or shine.

A good super fund for retirees provides its retired members with a range of these product choices and will help you understand which ones are best suited to your needs.

Account access

When you've retired you will most likely be much more engaged with your super fund, regularly reviewing your account balance and investment performance and withdrawing money from it. To do this you need your account to be easy to access.

And if you access your account via your desktop computer, smartphone or over the phone, you need to be confident that it's secure and safe. All super funds provide digital access to your accounts, but some do it better than others, are more intuitive and easier to understand.

Financial advice

When you're planning your retirement, or you've retired, you are much more likely to need financial advice from your super fund, or the support of your own financial adviser. A good super fund for retirees is one that gives you access to these services for a low reasonable cost.

| What to do when it's time for you to retire |