The impact of US tariffs on global real estate

As investors position their portfolios for greater geopolitical and economic uncertainty, US trade tariffs will have a varying impact on global real estate, with US properties potentially most exposed while certain international real estate markets may fare better.

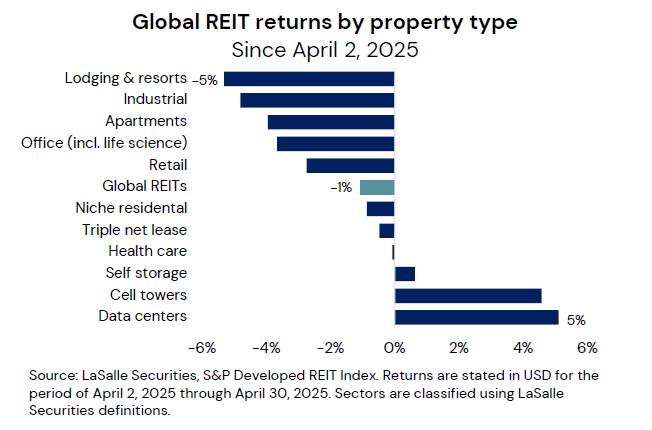

Examining the performance of listed real estate since 'Liberation Day' reveals a relatively benign impact so far.

Despite an initial drawdown of nearly 10%, the overall listed REIT market was down only marginally in April, though the dispersion of property sector performance has been wide.

An adverse investor reaction was the most focused in property directly exposed to a potential trade war such as industrial and logistics properties or those which are more economically sensitive in nature, such as hotels and lodgings, as the chart below reveals.

In terms of which countries will be the hardest hit, it seems tariffs could hit US real estate the hardest, for two important reasons.

First, the strongest headwinds in many exporting nations will be largely contained to specific industries, compared to potentially generalised challenges in the US.

A second reason is that the US Federal Reserve may have to balance risks of higher unemployment against those of higher prices, while in other countries, the short-term impact of tariffs could actually drive local goods prices lower. This may give central banks outside the US more wiggle room to offset a weaker economy with monetary policy easing.

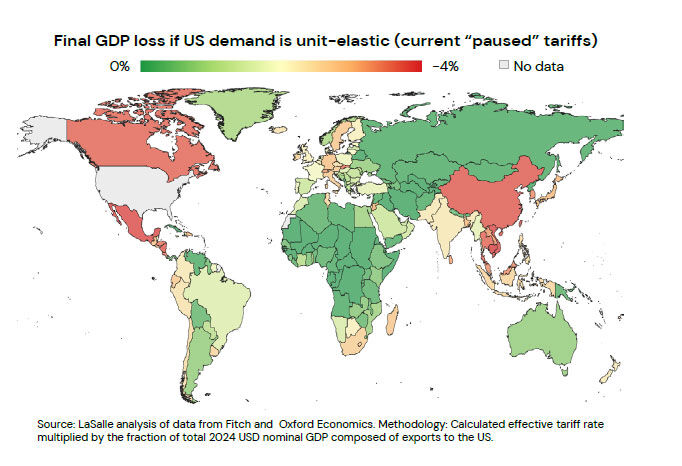

To separate relatively harder-hit from less-hit ex-US markets, LaSalle tracks the level of applied tariffs and a country's exports to the US as a share of the exporting country's GDP. On this basis, the map below shows that China, Southeast Asia, Canada and Mexico may be the most impacted, while Australia and Europe potentially could be less so.

The nature of the exports themselves also matters. It may be difficult to find viable substitute suppliers for many complex, high-value goods such as semiconductors, or for raw materials such as rare earths. Countries whose exports have fewer substitutes may be more insulated from the trade war, such as Australia, which has abundant rare earth materials which many other countries lack.

This geographic variation in the impact of the tariffs has been evident in the performance of US and ex-US listed real estate markets. The shift in US trade policy has led to the largest REIT share price declines being registered in the US (see the chart below).

European REIT markets, including the UK, have been relative winners given the potential pro-growth developments in fiscal policy and a more limited direct impact from US trade policy. Asia Pacific REIT market performance has been more mixed in this period, with Japan and Australia notable outperformers, particularly compared to Hong Kong.

For sectors that could be directly affected by US trade tariffs, for example industrial and logistics real estate, the impact may be short-lived.

While near-term fundamentals have been pressured, the long-term context of logistics real estate is one of positive structural growth, which means this impact takes the form of a downgrading, not a devastation, of the sector's prospects.

Moreover, in the long run, global economic fragmentation could lead to greater supply chain redundancy and therefore increased aggregate space demand.

Other examples of real estate sectors facing impacts directly tied to tariffs include US power centres exposed to discretionary expenditure on largely imported goods. Other directly affected sectors could include sectors with a high degree of economic sensitivity, such as hotels, which are likely to see an outsized negative hit to demand in the event of an economic downturn.

Meanwhile, economic impacts should be muted on sectors with low fundamental sensitivity to GDP growth, such as medical offices, cell towers and data centres. Relative impacts are potentially the reverse for sectors with a high degree of interest rate sensitivity.

An economic downturn usually leads to lower interest rates - although recent market movements suggest that is not necessarily a given.

The impact of lower rates on the more interest-rate sensitive parts of the real estate market could enable them to absorb some or even all the effect of softer demand. These property types are generally those with longer leases, such as the mainstream commercial sectors.

Overall, global real estate is well positioned to weather the current environment of greater economic uncertainty and trade tensions. Real estate possesses inherent structural characteristics that provide resilience. Values are underpinned by defensive and durable cash flows, often secured by long commercial leases.

In addition, healthy conditions in global real estate markets will support REITs. Falling supply levels, an upward repricing process and conservative overall leverage levels in most segments of global REITs could all favour the performance of global real estate in the months and years to come, despite growing uncertainties around global trade and geopolitical uncertainties arising from ongoing wars.

REIT valuations appear undemanding, and less stretched than those of several other major asset classes, especially large-cap equities. Real estate has underperformed general equities in recent years, cumulatively underperforming by around 30% since the end of 2021.

As the environment has shifted, it is possible that real estate's underperformance could reverse over the short to medium term and REITs could potentially outperform equities which are facing increased volatility given the new government in the US and rising geopolitical tensions.

Matthew Sgrizzi is CIO and portfolio manager at LaSalle Investment Management Securities

Get stories like this in our newsletters.