Strong outlook ahead for this bedding retailer

This week's Hot Stock is courtesy of Chris Batchelor from Skaffold.

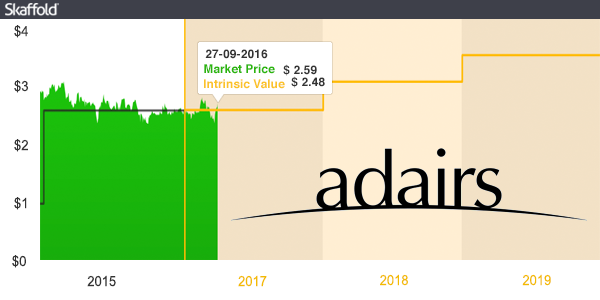

Adairs (ASX:ADH)

Key statistics:

Closing share price 27-9-16: $2.590

52-week high: $2.780

52-week low: $2.140

Most recent dividend: 6.5c

Annual dividend yield: 4.44%

Franking: 100%

Adairs (ADH) is a leading independent retailer of manchester in Australia. It sells a range of bedroom, bathroom and homewares products through 130 stores across Australia competing with the big department stores Myer and David Jones as well as specialty retailers like Bed Bath N' Table and Pillow Talk. Adairs is continuing to roll out new stores and has also established a concession format within three Myer stores branded UHR. In addition to the physical stores it has also established an online presence that now accounts for 8% of sales and grew by 64% last year.

2016 marked Adairs first full financial year as a listed company. It was floated by Brett Blundy's BB Retail Capital in June last year at $2.40 and has risen 8% to $2.59 but followed a mountain terrain path with a peak of $2.95 and valley of $2.25. The volatility is exacerbated by the tight ownership with the top three shareholders accounting for 50% of the issued shares. It is also a relatively small business with a market capitalisation of $430 million.

The results presented in August showed a business that is performing strongly. Same store sales revenue increased by 12% plus there were an additional 13 stores opened. After tax profits increased by 19% although cash flow from operations declined slightly on the back of a build up in inventory. Revenues and profits were also well above what was forecast in the prospectus.

Adairs imports most of the products it sells. They are sourced from manufacturers primarily in China but also in places like India, Turkey and Portugal. Being an importer a falling currency eats into their profit margins. Despite the fall in the currency over the past 12 months, it managed to maintain a healthy gross profit margin of 61%, which was only a reduction of 1% from the previous year.

Market analysts are forecasting earnings per share growth of 13%pa over the next three years. Given the strong track record of management and the growth achieved despite the currency headwinds last year, these forecasts seem achievable. Return on equity is high at 30%, and this combined with a sensible dividend policy means that the value of the business is forecast to grow at 17%. With the share price currently trading around fair value there is plenty of upside for this recent entrant to the listed retailers space.

Chris Batchelor is a chartered financial analyst from Skaffold.

Get stories like this in our newsletters.