Adventure retailer Kathmandu reaches for new peaks

Key statistics: ASX: KMD

Closing share price 18.01.17: $1.830

52-week high: $2.070

52-week low: - Most recent dividend: 7.522c

Annual dividend yield: 25.66%

Franking: 85%

Kathmandu is a New Zealand company with listings on both the NZ and Australian stock exchanges.

It is a retailer of outdoor wear and equipment, with 65% of revenue derived in Australia, 33% in New Zealand and a minor amount in the UK. Among adventure enthusiasts it is well known for its gear as well as for its big sales three times a year.

This reputation for discounting got the company into a bit of trouble in 2015.

Too much discounting can become a vicious cycle as customers are no longer willing to pay full price, necessitating more discounting to move stock.

Heavy discounting and a build-up of stock led to Kathmandu profits falling 51%. Earnings per share hit their lowest level since 2010.

This culminated in a hostile takeover offer bid from New Zealand competitor Briscoe, which was ultimately rejected by the board and shareholders.

Shareholders felt the offer was an opportunistic grab at a low point for the company. They put their faith in new CEO Xavier Simonet and his strategy to turn the business around.

So far that faith is being rewarded and the prospects are looking up. 2016 saw a strong turnaround in the business.

Kathmandu profits rebounded by 72%, although they are still less than in 2013 and 2014, debt was reduced and so was inventory. Simonet has introduced more discipline around discounting, focusing on maximising gross profit rather than revenue.

The all-important measure of cash flow was also strong during 2016 and, indeed, has been strong overall for the past 10 years. Cash generated from operations exceeds reported profits, making room for additional investment in the business as well as the payment of dividends.

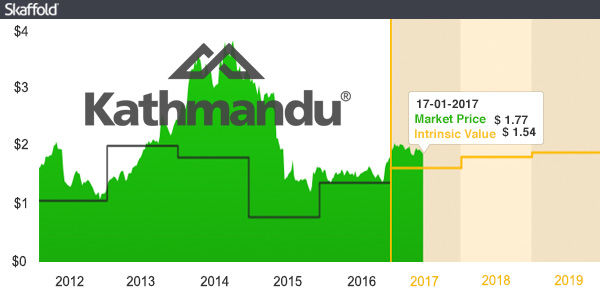

Unsurprisingly, the share price has followed a similarly rugged trail as profits. It peaked around $3.60 in 2014, then plunged into the valley in 2015, down to $1.11, followed by a gradual ascent back up to today's level of $1.77.

Earnings per share are forecast to grow at a steady 6%pa over the next three years. While 6% growth will not provide an adrenalin rush, the stock is priced attractively at a forecast price-earnings ratio of 10.5 and the intrinsic value is forecast to increase at 8%pa, as seen in the chart below.

Retailing is a challenging business. There is strong competition from a wide range of competitors as well as new business models that are challenging traditional ways of retailing.

Kathmandu has weathered the storm to date and under Simonet is shedding any excess baggage it shouldn't be carrying and provisioning for a long, steady, upward trek.

Data accurate as at January 16, 2017.

Get stories like this in our newsletters.