How to borrow money when you're self-employed

It's possible for the self-employed to get finance at a reasonable rate

Living the dream of being your own boss may be costing you that other dream - home ownership.

If you're one of our 1.2 million sole traders or 2.1 million business owners, then you'll know what I'm talking about: you've got no PAYG pay slips to prove your income, more than likely it fluctuates from month to month and your last tax return, which you probably lodged 12 to 18 months ago, does little to reflect where your business is now.

So if you prove your income, how do you convince a lender to give you a home loan?

The good news is that low-doc loans are making a comeback and, surprisingly, you don't have to pay through the nose to get one.

Canstar's analysis has found that, on average, a standard variable low-doc home loan will cost 0.63% more than the non-low-doc product. For a three-year fixed residential loan, the difference between low-doc and non-low-doc is 0.45% on average.

Of course, that's assuming you get a loan that falls under the protection of the national consumer credit protection code.

There are many private lenders offering low- and even no-doc loans for non-coded purposes (think solicitor loans) but as Yannick Ieko, CEO and founder of Low Doc Loan Experts, says, "you can easily hit double digits for a non-coded no-doc loan".

Before the GFC you could have picked up a traditional low-doc loan on the back of a one-day ABN and an income self-declaration form but, as Ieko says, things have tightened up somewhat.

"The paperwork required will vary from just an accountant declaration to things such as BAS statements, trading account statements and personal account statements," he says.

"Main-street banks are more likely to require all of the above while some non-bank lenders will be satisfied with just the accountant's letter."

As a specialist low-doc mortgage broker, Ieko says getting approval comes down to finding a low-doc lender that is favourable to your circumstances, as lenders do differ.

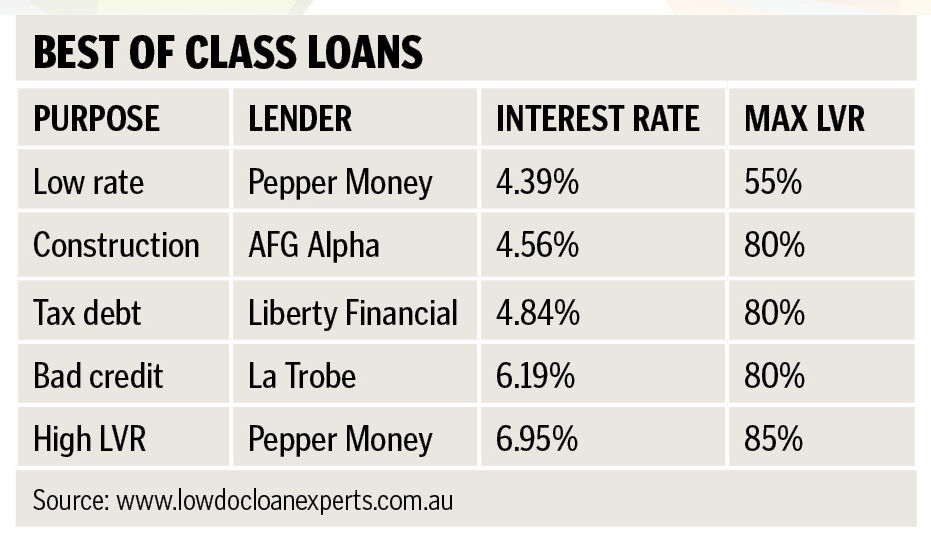

"Non-bank lenders are likely to offer a higher loan-to-value ratio and to require less paper to evidence the income," he says. "Some of them are also able to assist with a wider range of purposes, such as the payment of tax debt or construction loans."

You could argue that loans such as these encourage applicants to fudge figures (some of you may remember the tax office's "low-doc loan project", which raised $23 million in tax penalties in 2006 on the back of applicants who inflated income figures to lenders) but Ieko says it's a very different market today.

"Income is still verified, credit history is still checked, security is still professionally valued, and all the non-income-evidencing normal hoops and loops that apply to other loans are still part of the process."

While margins on interest rates may not be excessive, Canstar data does show that low-doc home loans tend to charge higher set-up fees than standard home loans.

The other point to note is whether or not the lender will allow you to refinance to a standard home loan once you've proven your serviceability. Some don't.

Get stories like this in our newsletters.