Should you buy, hold or sell Nick Scali shares?

Nick Scali Furniture (Nick Scali) was established over 60 years ago and is now one of Australia's largest importers of furniture.

Many will know Nick Scali for their lounge ads on TV, however they also sell other furniture including armchairs, dining tables and chairs, bedding, dressers, and have a wide range of accessories associated with these categories.

The company has stores across Australia and in 2017 entered the New Zealand market, opening its first showroom in Wellington.

In 2021, Nick Scali acquired the Plush brand, picking up 43 additional store locations to go alongside their 64 Nick Scali branded showrooms in Australia and New Zealand (ANZ).

More recently, Fabb furniture was acquired by the group in the UK, adding 21 locations there and marking its first foray into that market. The company is run by its founder and major shareholder Nicholas D Scali.

Nick Scali strategy

We consider Nick Scali to be a best-in-class retailer, frequently highlighting its capability to outperform its competitor set in ANZ (mostly recently reporting flat sales in a down market).

The company's strategy has also included adding new incremental stores in the ANZ market, however it's the recent acquisition of Fabb in the UK that adds an exciting new growth avenue.

Purchased for a nominal equity value of just GBP2, Fabb provides a footprint of over 20 stores in good retail locations across the UK, a market with very similar characteristics to ANZ.

The business has struggled to make any significant profits for over a decade, with the owners lacking any meaningful retail experience and the appearance of no real strategy to drive profits or growth.

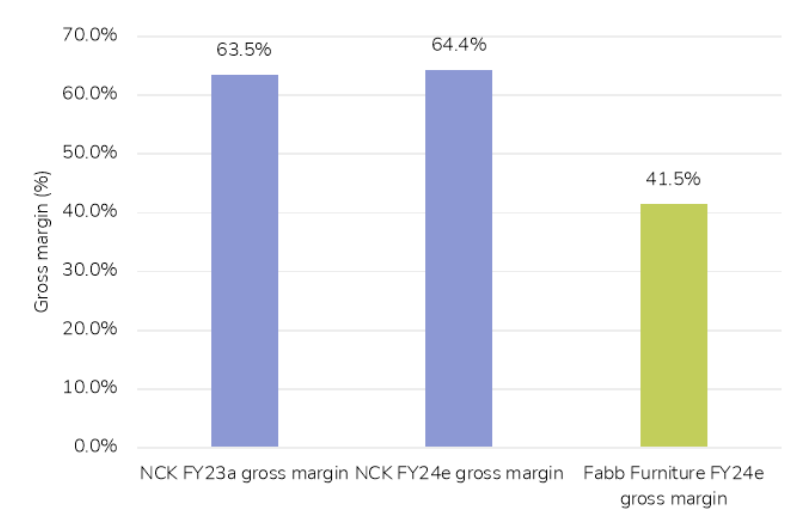

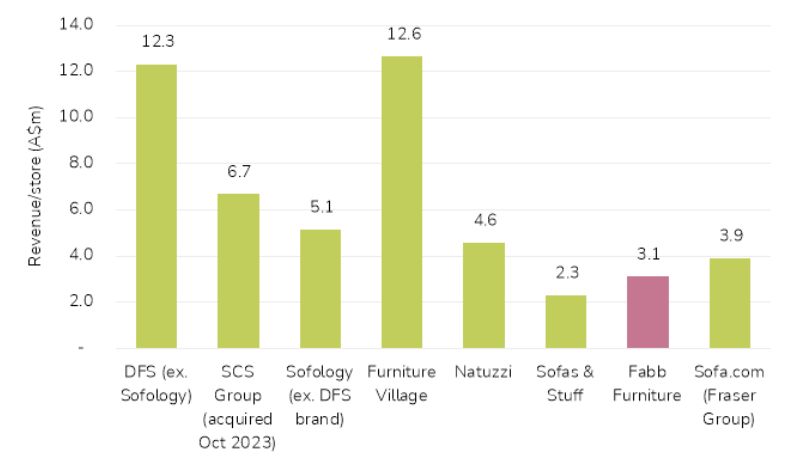

As a result, sales per store and margins within the Fabb business are low and much lower than Nick Scali's.

Management believes they can lift margins up to nearer their current group margin level by ranging their Nick Scali product in the Fabb stores, leveraging their existing supplier relationships to obtain lower-cost product and improved store layouts and efficiencies.

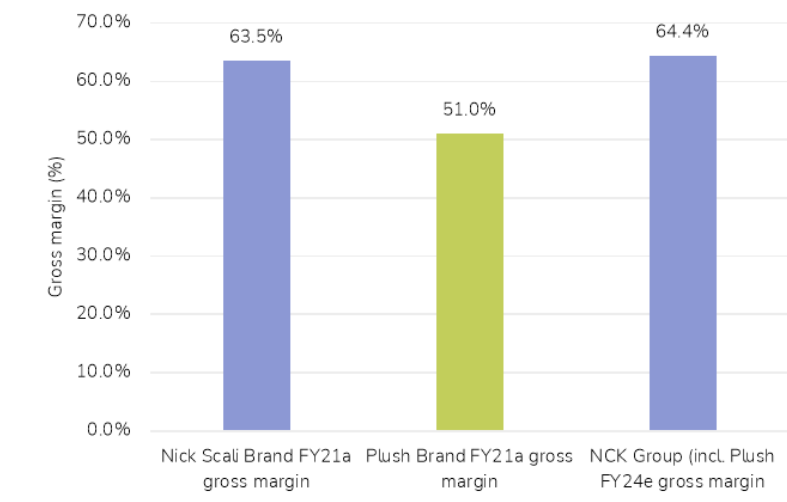

The great thing about this strategy is that we know it can work, as Nick Scali has already executed the same strategy with the Plush business they bought back in 2021.

They lifted the Plush margin up in line with group margin within three years.

Management also believes that opportunity exists to improve the revenue per store via refreshed products, a store refurbishment program and some basic retail merchandising such as planograms.

While the sales culture within the Fabb group is reportedly good and store locations favourable, lack of strategic planning and poor store layouts are believed to have hindered sales velocity.

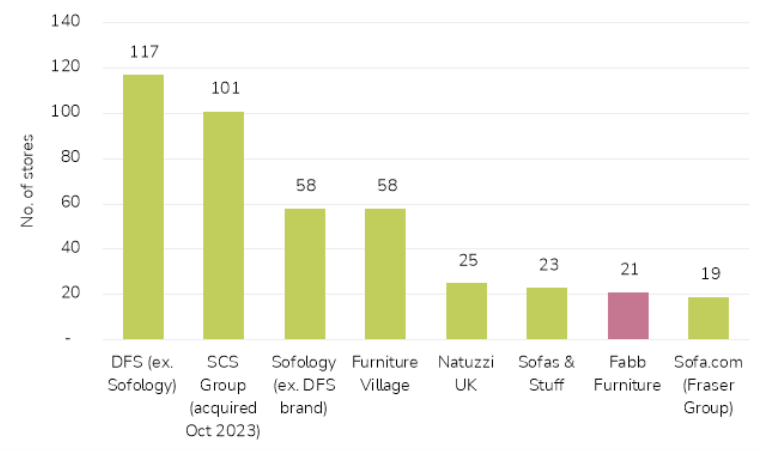

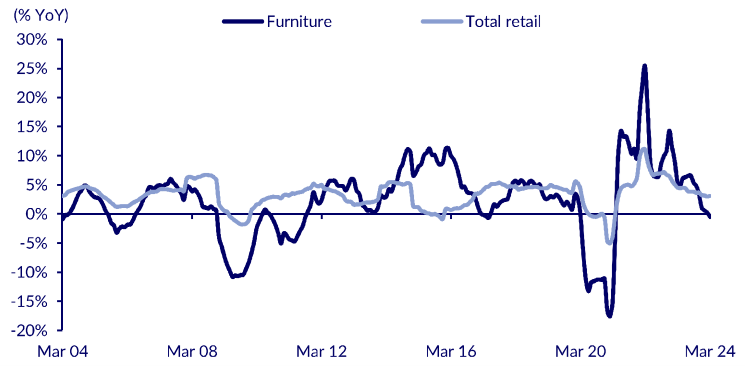

Below we can see where Fabb sits in relation to their local market and the opportunity for the new owners to materially improve Fabbs' top line.

Outlook

While Fabb is currently only a relatively small part of the Nick Scali portfolio, we can envision it becoming larger over time.

The population of the UK is much larger compared to Australia and while the average spend per person is slightly lower, it is similar.

This large addressable customer base is serviced by a more fragmented industry of players, with the opportunity for Nick Scali to roll out new stores (given their history of success in ANZ) and even make bolt on acquisitions of players a similar size to Fabb.

Large players in the space have a similar store number to that of Nick Scali in ANZ, which we believe could be a longer-term store target.

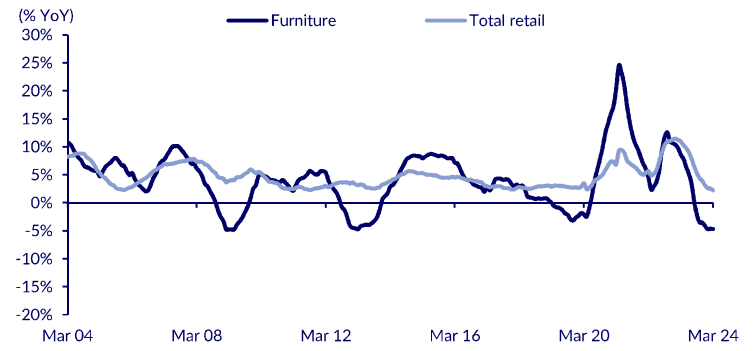

We feel Nick Scali has taken an opportune time to make its entry into the UK market, making a relatively small outlay to establish a beachhead there while retail activity levels have been quite soft.

As can be seen below, it has been somewhat similar here in Australia, with sales activity nearer to trough levels rather than a peak.

Nick Scali should be heading into relatively easier comparable sales periods in both markets in the months ahead.

Meanwhile, the prospect of some household relief via tax cuts in Australia and possibly the prospect of lower interest rates towards year-end should also help sales over the next 12 months.

Returns

Nick Scali has a strong history of growing earnings and thus returns, delivering a 16% compound annual growth rate (CAGR) over the past five years prior to dividends.

We think the days of growth are not over, given this exciting new market roll out of its successful Nick Scali range of lounges and furniture.

We think, in time, there is no reason the UK business couldn't be the same size as ANZ is currently.

Recommendation

Nick Scali currently trades on a 12-month forward price-to-earnings multiple of 14.9x, 5% above its 10-year average.

It is forecast to yield a dividend of 66 cents per share for a yield of 4.5%. While growth in FY25 will be impacted by the refurbishment program at the Fabb stores in the UK, we forecast a resumption to strong growth from FY26.

We believe that Nick Scali shares can trade to $20, a 25% return from current levels, as investors become more comfortable with their improved growth profile and deliver a multiple re-rating. Buy.

Get stories like this in our newsletters.