Should you buy, hold or sell Pro Medicus shares?

Pro Medicus (ASX:PME) is a leading global provider of radiology information systems (RIS), Picture Archiving and Communication Systems (PACS) and advanced visualisation solutions.

Founded in 1983, the company has become an industry leader in the US radiology imaging software segment with Visage Imaging.

The opportunity for growth

The market is still dominated by proprietary solutions from imaging hardware providers including GE, Philips and AGFA.

However, the older solutions are facing compatibility issues and are increasingly struggling to work with the large files produced by the latest imaging technology. This is resulting in long wait times to view and review radiology images and in turn reducing productivity of radiologists.

With the ongoing development of new technology, image file sizes are continuing to increase and this is forcing providers, both hospitals and out-patient practices, to upgrade their imaging enterprise infrastructure.

For Pro Medicus, this is creating a steady flow of potential customers seeking a new enterprise imaging solution like Visage that is compatible and efficient in processing radiology images.

The advantages

Visage has a clear advantage - its speed and ease of use. It uses streaming technology which provides immediate access to images and allows the images to be easily viewed and manipulated, without having to wait for the file to load.

This has led to an increase in productivity amongst radiologists, with Visage accepted by many radiologists as the leading solution. Increased radiologist productivity is key for many hospitals and out-patient practices worldwide which are facing a shortage of radiologists and a growth in demand for medical imaging.

Visage is also an open solution which means it can work with all brands of imaging hardware, whereas most legacy solutions can only work with a single hardware brand.

Its streaming technology also works in the cloud and is considered 'cloud native'. This is not the case with the offerings of its competitors.

The majority of Visage deployments are now in the cloud and work with all three large cloud providers - AWS, Google and Microsoft Azure. This allows Visage to serve customers of all sizes as there is no hardware investment required.

Visage has a 'per click' model, which means it charges providers for each image/case viewed. This ensures its revenue grows as the market grows, and Visages' customers are growing faster than the market in part through mergers and acquisitions.

Expansion into other offerings

Pro Medicus has expanded its US offering to include a vendor-neutral archive (Visage 7 Open Archive) and workflow software (Visage 7 Workflow) in addition to its core viewer. This has materially increased the group's revenues/price per click.

The price per charge by Visage for each click (case viewed) has been rising well above inflation in recent years as the company lifts its rates especially when contracts are renewed.

Visage has been selected by more than half of the leading US academic hospitals such as the Mayo Clinic and Memorial Sloan Kettering. Anecdotes even suggest that many radiologists will only work at institutions which have deployed Visage.

Visage is provided on a software as a service (SAAS) basis. The cost to Pro Medicus for an additional customer (excluding sales/marketing and set-up costs) is virtually zero. Gross margins are above 99%.

Expansion into additional radiology market segments

Visage began by winning large academic hospital customers and has since expanded into the larger Integrated Delivery Network (IDN) segments (health systems with multiple hospitals and outpatient clinics).

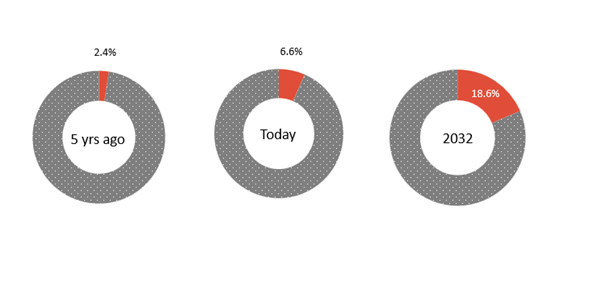

Most recently Pro Medicus announced contracts with two out-patient private radiology groups demonstrating it can service all segments of the market. A market share of well over 20% appears achievable.

Outlook and recommendation

To date Pro Medicus has focused on the US market with only modest customer numbers in Europe and Australia. We expect this to change in the coming years, potentially doubling the size of the addressable market.

Pro Medicus has also expanded Visage to include cardiology imaging, an area of opportunity we expect to see grow over the next few years. While this market is only one fifth the size of imaging, by volume pricing it will be two to three times higher suggesting it could be a large opportunity.

We expect Pro Medicus to announce its first cardiology customers later this year - it is even likely cardiology customers are already using Visage.

Visage also has limited competition. The other large hardware-independent software provider is Sectra. Compared to Sectra, Pro Medicus has shown superior growth in recent years and generates much higher margins. Sectra does not appear to have a product that functions as effectively in the cloud.

Artificial intelligence is also an untapped opportunity for Pro Medicus, and it is uniquely placed to become a platform for the use of AI in imaging.

Our recommendation is a buy.

Get stories like this in our newsletters.