Should you buy, hold or sell Telix shares?

Pharmaceutical companies often find themselves in a cycle of high cash burn and constantly raising capital, only to fall by the wayside.

But from time to time a business in this space is able to deliver an approved, leading-edge offering that takes the world by storm and delivers explosive revenue growth.

One such company is Telix Pharmaceuticals.

What does Telix actually do?

Telix is a commercial-stage biopharmaceutical company focused on the development and commercialisation of diagnostic and therapeutic radiopharmaceuticals.

Telix is on the leading edge of theranostics, the field of targeted radiation for cancer diagnostics and ideally in future the actual treatment using that same technology.

Telix's commercially approved diagnostics offering is focused on the prostate cancer space, however, they are also deep into trials for the diagnostics of kidney, brain, and blood cancers.

Essentially, their nuclear medicine is attracted to the cancer proteins and can provide very clear visibility of the location of the cancer at very early stages.

The exciting prospect is that if they are able to successfully seek out various cancers, then logically there should be a possibility to package up treatments that can be delivered directly to the site of the problem.

The continued research and development to expand offerings is sustainably funded both through their fast-growing cashflows and via partnerships with larger cancer-focused pharma giants.

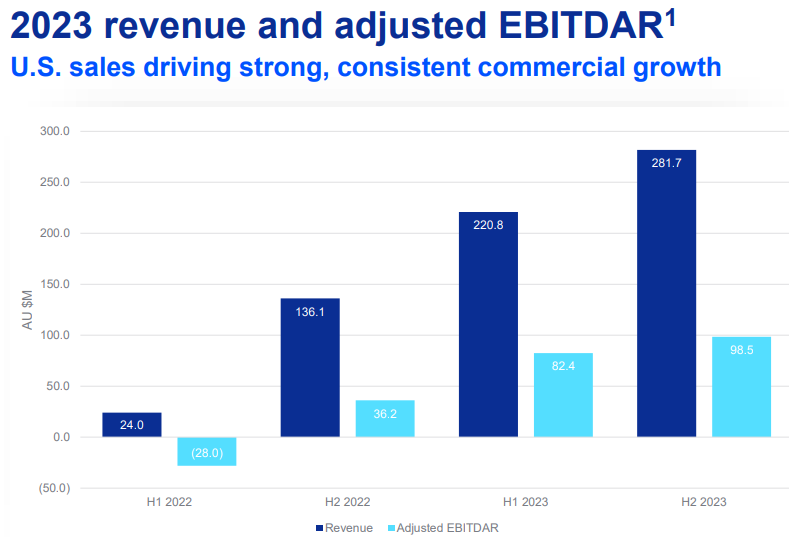

Revenues increase rapidly thanks to Illuccix

Illuccix is Telix's currently approved offering and generates the vast majority of revenues for the business.

It is an advanced imaging tracer that binds to prostate cancer cells in and around the prostate, or throughout the body. This imaging tracer is then detected with a PET scan to reveal prostate cancer.

Doctors can then use this to make more informed decisions around treatment. Illuccix targets a specific protein that is abundant in prostate cancer, called PSMA, and binds to it.

The product contains small amounts of radioactive material that light up with a PET scan, allowing detection of cancer cells and identifying if it has spread to other parts of the body.

Illuccix has experienced a rapid increase in demand and sales over the past two years particularly.

Telix has seen revenues increase from just $24 million in the first half of 2022, to $281.7 million in the second half of FY23, a more than 10-times increase over the short period. Adjusted earning (EBITDAR) also increased from a $28 million loss to up $98.5 million over the same period.

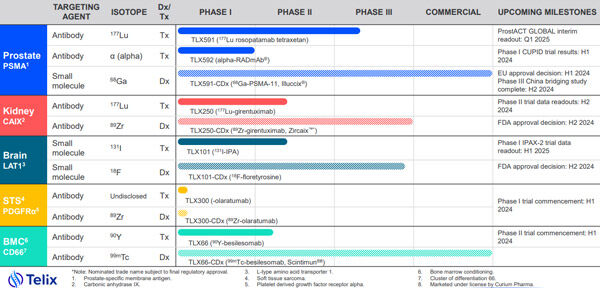

Product pipeline bringing significant upside potential

While their prostate cancer diagnostic offering, Illuccix, is currently approved by the Australian TGA, the US FDA and Health Canada, we are extremely encouraged by the upside potential of additional approvals into the other regions where clinical programs and trials are underway.

These include the UK and 19 European countries, as well as China and Japan.

Should Telix experience anywhere near the success they've seen in the US in these new markets, the revenue upside could be substantial. In addition to the Illuccix prostate cancer diagnostics offering, Telix has a very encouraging pipeline of diagnostic and treatment offerings for other cancers as shown below.

FY24 guidance and strong first quarter figures

In their FY23 annual report, Telix guided revenue to be in the range of $675 million to $705 million, with possible upside coming from Zircaix (kidney cancer imaging) and Pixclara (brain tumour imaging). Zircaix and Pixclara are awaiting FDA and NDA approval respectively.

The revenue guidance represents a 35-40% increase compared to the prior year - with further guidance to be provided to reflect possible product approvals. The company also expects an increase in R&D investment of about 40-50% compared to FY23.

R&D investment will go towards commercial manufacturing and market launch activities for Zircaix and Pixclara, as well as a fully operational Phase 3 therapy trial in prostate cancer. As of their Q1 2024 financial performance update, the company delivered revenue for the quarter of $175 million (+75% against Q1 of FY23).

Gross Profit increased 84% to $115 million and operating profit came in at $28.5 million against a loss of $5.6 million in last year's first quarter. On top of rapidly growing revenues, Telix also holds a healthy cash balance of $122 million which can put be put towards the likes of R&D, marketing and additional business acquisitions.

Is it too late to invest?

We are often asked, or hear the opinion that the horse has already bolted on companies that have seen strong share price gains like Telix.

In most cases, great businesses continue delivering impressive results and we believe that Telix, only generating first sales in recent years are still very early in their journey with significant upside potential from here.

The runway for growth is large, via both expansion of their current prostate diagnostics offering into new markets as well as new product offerings focusing on diagnostics for other cancers and also treatment.

Get stories like this in our newsletters.