Our changing breakfast habits are feeding this company's boom

Key statistics: ASX: NUF

Closing share price 03.10.17: $8.110

52-week high: $10.470

52-week low: $8.010

Most recent dividend: 8c

Annual dividend yield: 1.58%

Franking: 0%

Crop protection specialist Nufarm (ASX: NUF) delivered a more than 300% increase in statutory net profit for the 2017 fiscal year.

Excluding one-off items, underlying profit was also up healthily, rising 25% to $135.8 million.

The company expects to continue growing earnings through a combination of new product introduction, a focus on higher-value market segments and further efficiency improvement program benefits.

Ultimately we see the agricultural sector (and Nufarm's customers) getting a boost from a growing global population, and the fact that consumption habits are changing (and becoming more Westernised).

Asia in particular is set to put a rocket under demand in the coming decades. The fact that land is in limited supply also means that agricultural yields need to rise.

We believe an improving long-term outlook (and subdued prices) is also why we have seen more action on the merger and acquisition front in recent times.

Swiss competitor Syngenta has been swallowed up by ChemChina, while Monsanto has fallen to German group Bayer.

One possible impediment to Nufarm also coming onto the radar of an acquirer has been a 23% blocking stake held by Sumitomo Chemicals.

The Japanese company, though, is thought to be in the midst of selling out. Nufarm has been acquisitive itself in recent years but the shoe could soon be on the other foot.

2017 results

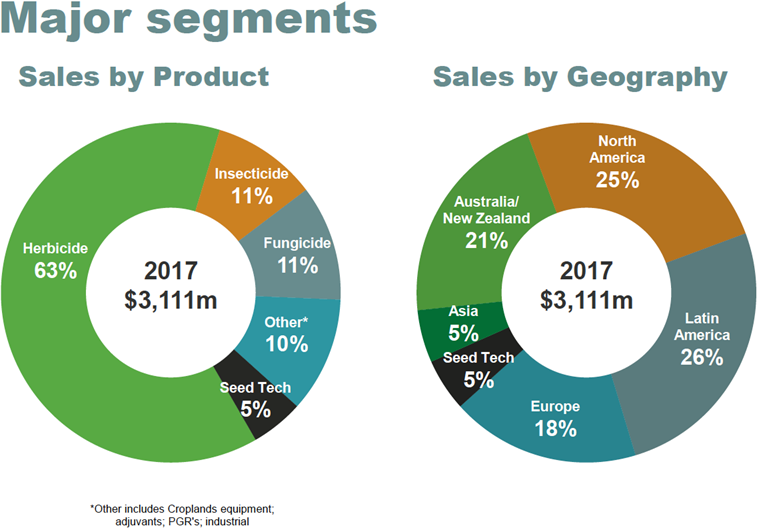

Despite what Nufarm referred to as "tough industry conditions", it delivered a double-digit revenue increase. Sales of $3.111 billion for the year were up 11.5% over 2016, only slightly above consensus analyst forecasts of $3 billion.

Nufarm benefited from higher sales in the core crop protection segment, which rose 11% to $2.94 billion.

Herbicide turnover increased roughly 10% to $1.95 billion, insecticide sales surged 18% to $34 million and fungicide sales were up 8% to $335 million.

Sales across the group increased in all regions measured on a constant currency basis. It was a solid enough top-line result during a period when the overall industry recorded marginal to no growth.

Group underlying gross margins in 2017 came in at 29.4%, in line with last year.

Underlying EBITDA (earnings before interest, tax, depreciation and amortisation) was up 4.9% year on year to $390 million, and at $302.3 million underlying EBIT (earnings before interest and tax) increased 5.4%.

Margins were curbed by foreign exchange movements but rose on a constant currency basis.

The company's performance improvement program delivered an incremental net EBIT benefit of $26 million and remains on track to "deliver at least $116 million by FY18".

The benefits of this cost-out program are a core plank of our investment case for Nufarm, and we have been generally content with its progress to date.

Regional trends were also generally favourable, although a soft performance in Argentina dragged Latin American earnings down 11% to $89.4 million.

The Argentina peso also weakened 30% against the Australian dollar over the year, exacerbating the headwinds.

All other regions in the crop protection segment posted higher earnings, with North America leading the way, with an 18.5% jump to $70.3 million on a 16.4% improvement in sales to $761.1 million.

The company also did well in Europe where profits increased 17.5% to $85.8 million, even as sales fell slightly (down 1.9%), due to a fall in the euro. The previously announced restructuring of the European manufacturing base has been completed and this will flow through to earnings growth in our view.

The Australia and New Zealand region reported sales of $654.2 million, marking an 18% increase on the previous year as management capably executed a strategy to regain volume and market share.

Despite challenging climatic conditions in Australia, earnings for the region increased some 9.9% year on year to $51.6 million with an improving trend in the second half.

The company has also rationalised operations down under, closing three manufacturing facilities.

This initiative has lowered fixed costs and will enables better plant utilisation and efficiencies.

Nufarm shares trade on about 16 times 2018 financial year earnings, falling to 14 times the following year.

Despite some challenging industry conditions, the company continues to benefit from various restructuring and business optimisation initiatives that have featured over the past several years.

Nufarm is now much leaner and meaner, and the company's strong capital position provides further strategic optionality within a consolidating industry.

Will Nufarm become a target? Time could soon tell.

Disclosure: Interests associated with Fat Prophets declare a holding in Nufarm.

Get stories like this in our newsletters.