Is now the time to buy, hold or sell ResMed shares?

ResMed (ASX:RMD) is the dominant global supplier of medical equipment to treat obstructive sleep apnoea, an increasingly common affliction.

Confidence in the outlook for the business dropped in mid-2023 with the arrival of the GLP-1 anti-obesity drugs as investors feared a drop in obesity rates would lower the prevalence of obstructive sleep apnoea.

So far, this fear has been misplaced, and I expect in the next couple of years obesity drugs will draw in many more patients who will discover they have sleep apnoea and be prescribed one of ResMed's devices.

In the longer term this could become more of a challenge, but this will require life-long adherence to the new drugs, despite their side effects, which seems improbable.

The valuation metrics have recovered some of the lost ground from the lows in 2023, but at about 21x next year's earnings, it is well below the 30x level seen prior to the emergence of the new obesity drugs.

I expect the company to deliver strong earnings growth over the next few years supported by a wave of patients seeking obesity drugs and from increased use of wearables (Apple and Samsung watches) which should also lift the number of patients diagnosed with sleep apnoea.

ResMed has a proven management team with the key leadership group having been with the firm for well over a decade.

The company also has strong track record in the competitive medical device space and its more recent investments in software as a service has shown good signs of developing into an attractive new source of revenue.

What it does

ResMed's core business is the treatment of sleep apnoea, a common condition in which the suffers' airways collapse while asleep, leading to many periods of suffocation which causes the patient to wake.

This leads to poor sleep quality in the short term, and if left untreated, sleep apnoea is associated with high blood pressure along with many other detrimental health conditions.

Data from a ResMed sponsored study reported there are more than one billion suffers globally. The high incidence of this chronic condition has proven to be a lucrative market.

ResMed sells both the CPAP and related devices along with the mask and tubing.

Patients typically purchase a new mask every three to six months with the regular replacement of masks linked with better adherence and superior patient outcomes.

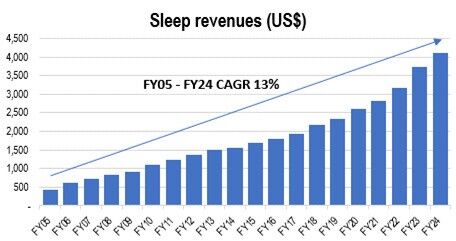

The masks account for over 40% of the company's sleep revenues and this is expected to continue to grow as the installed base expands. As shown in the chart below, ResMed has delivered nearly 13% annualised growth in sleep sales since FY05.

ResMed added a software division in 2016 with the purchase of Brightree, a provider to ResMed's US customers.

It has since expanded via acquisitions into software as a service for care providers in settings outside of hospitals in the US and more recently in Germany.

The software division now accounts for nearly 15% of group revenues and management have guided to high single digit top line growth.

Strategy

After the key competitor, Philips, was forced to recall it's sleep device range in 2021, ResMed focused on expanding its production to cater for demand allowing it to build its market share to approximately 90%.

ResMed's technology lead should hold for some years as Philips' ability to bring an updated CPAP device to market has been limited by the regulatory oversight associated with its settlement with the US Food and Drug Administration (FDA).

It remains unclear when Philips will return, but I am confident ResMed will be ready and should be able to maintain its dominant position.

Given the group's dominance, the strategy has switched to lifting market growth via demand stimulation programs.

In particular, the group is seeking to leverage the growth of obesity medications noting the close link between weight and sleep apnoea. ResMed now directly markets to doctors who are large prescribers of obesity medications. This is seen as fertile ground for new sleep apnoea patients.

The other strategic advantage ResMed has is that its devices are "connected", meaning they provide immediate feedback to the patient and prescribing doctor.

With over 20 million devices in the field, ResMed has built a database of over 20 billion nights of sleep and respiratory data which supports a constant improvement cycle. This large database should ensure ResMed maintains a near unassailable lead over its competitors, including Philips.

Looking further into the future, ResMed has reported a solid increase in long term patient adherence to the treatment. This positive trend supports the sale of more masks.

ResMed has long been the leading supplier of masks, and this high-margin revenue source should continue to grow as the installed base expands and patient's adherence improves.

Returns

ResMed has a long track record of delivering strong returns.

Return on equity was 25% in FY24 and this should be sustainable over the medium term, especially as mask sales growth is set to overtake device sales, supporting a lift in margins.

The investment into software services should also support further expansion in returns.

Management has also indicated it expects to deliver further improvement in operating leverage as sales growth exceeds expectations.

Recommendation

I recommend it as a buy.

Get stories like this in our newsletters.