Is the tech bubble about to burst?

The US share market has leaped ahead of other markets this year, but the technology-driven rally is vulnerable to the same fate it suffered in 2022, and there are even echoes of the dotcom bust of 2000.

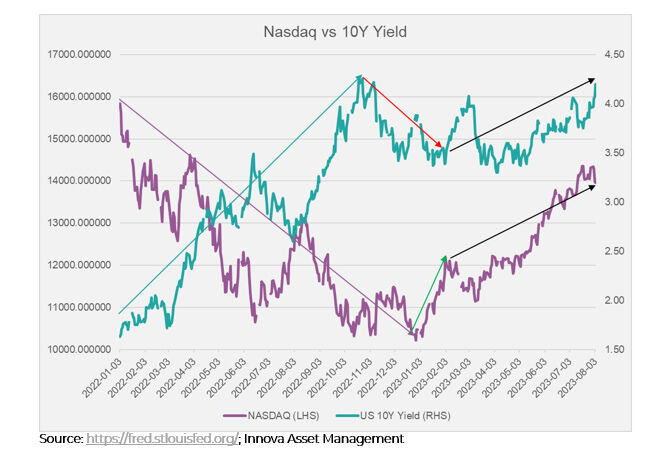

The current rally has been triggered by investors' enthusiasm for companies enabling artificial intelligence (AI). Yet it defies logic, with interest-rate sensitive technology stocks rising the most in the face of dramatically higher US Treasury bond yields, which have risen to their highest since 2008.

No matter what the bulls argue, this rally makes no fundamental sense and we could see the start of a broader technology sell-off this year, with the Nasdaq Composite Index posting its first monthly drop this year in August 2023 and September too is looking like it could be a weaker month. Prices are starting to wobble.

What does 'tech bubble' mean?

Investors considering a technology investment now must not forget that the price paid for companies drives long-term returns and they might have to wait for a long time for decent returns if they buy into US shares at current levels.

In the late 1990s, it was the internet. Online retail giant Amazon was one of the winners in the dotcom rally, but its stock went from over US$5 in December 1999 and fell to just over thirty cents in 2001.

Microsoft dropped from US$58 in 1999 to US$22 in 2000 - investors had to wait 16 years for Microsoft and 11 years for Amazon to get their money back.

Is AI the next tech bubble?

A similar scenario could play out in coming months. The AI rally, triggered by ChatGPT's launch in November 2022, has seen many investors rush into expensive AI stocks.

While they may ultimately be proven right, there are plenty of safer places to invest given the risk of persistent inflation and higher interest rates, and a potential economic slowdown in the US.

This includes emerging markets such as Korea and the UK, which are both much cheaper than the US equity market (so they are unlikely to suffer as much if there is a downturn).

In contrast, the US stock market leaders this year already have a lot of future good news in their prices, so we think they are more likely to disappoint than impress.

Where is the US economy headed?

There are big questions about the health of the US.

On the surface, the economy seems strong. However, US employment, economic growth and inflation are lagging indicators, so it would pay investors to look to the future, not to the past or present, before they make investment decisions.

We've all heard of analogies of the dangers of driving while looking in the rear-view mirror; there exists a high risk of a crash.

If we dig into some of the more nuanced components of the US economy, there is a plethora of indicators outside of growth and inflation data which are pointing to more difficult times ahead.

US retail sales are missing expectations, new home sales and housing starts are worse than expected and US economic productivity is falling.

What did we learn from reporting season?

Following reporting season, we've started to see companies downgrade earnings. We are also seeing huge job layoffs in the US technology sector, as companies try to curb their expenses.

Despite these warning signs and the collapse of Silicon Valley and Signature banks, the interest rate-sensitive tech sector has continued to rally for much of the year, as the chart below shows. This rally breaks with logical, fundamental reasoning.

However, if we're wrong, and the US leads the world into a global cyclical rebound, the areas currently offering more protection are the same sectors that are more likely to lead future gains - cyclical sectors and regions that are more appropriately priced and generally do well in a cyclical upturn.

If all the good news is already in the price of the 'Magnificent 7' technology shares - Tesla, Apple, Amazon.com, Nvidia, Microsoft and Google's owner Alphabet - then logically you'd expect the areas that don't have this good news in the price to benefit to a greater extent. The August pullback has already shown that there is real fragility in the current price of the 'Magnificent 7'.

When will the US Federal Reserve cut the cash rate?

Looking at current prices, markets have been pricing in interest rate cuts from the US Federal Reserve, and this could be wishful thinking.

If the US Fed were to cut rates soon, with inflation still high, this could likely cause a stock-price bubble that could have devastating after-effects when it pops - and the US central bank knows this, not to mention they could fan the flames of a second wave of inflation.

So, the question becomes, why would the US central bank cut interest rates any time soon? We don't think it will.

In reality, there would need to be some form of weakness in the US economy that the US Fed would try to stimulate by cutting rates - this would likely be economic weakness, poor employment numbers or a stock market crash. But we have not seen that yet.

High interest rates could be here to stay for some time. With stock prices still high, guessing who will be the next big winner in the AI race is a risky game; we've seen this playbook before throughout history and the costs of any AI gamble now could be potentially very high.

Get stories like this in our newsletters.