Nasdaq poised for long-term growth

Of the US broad market indices, one has stood head and shoulders above the rest over the past two decades - the Nasdaq 100 - which comprises the 100 largest non-financial companies on the Nasdaq exchange.

Most recently Nasdaq-listed companies have led US markets to all-time highs, which sparks questions about where to next for this exposure.

Home to Apple, Amazon, Nvidia and other global technology giants six Nasdaq stocks now boast market caps well over US$1 trillion.

This has raised questions whether US economic activity can support the ongoing growth of such giants.

However, despite the Nasdaq exchange sitting in New York, and the HQs of these companies mostly located in the US, these companies should not be seen as US-centric businesses.

Perhaps an underappreciated fact is that with scalable platforms that transcend national borders, many Nasdaq companies generate revenue from a globally diverse customer base.

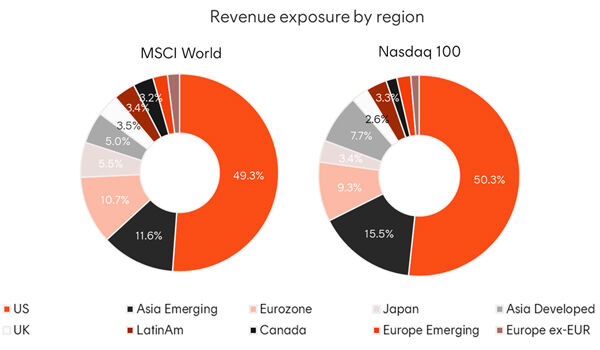

A quick look under the hood of the companies that comprise the Nasdaq-100 and breaking down their revenue source by country (on the left), it shows that these companies have a very similar split to global equities (as shown for the MSCI World benchmark on the right).

This proportion of non-US revenue share has increased over time for the Nasdaq 100 and is now far greater than the S&P500 non-US revenue share of only 40%.

Not only are Nasdaq companies earning more from outside the US, the number of non-US companies choosing to list on the Nasdaq is also increasing.

The top 100 stocks include names like Lululemon (Canada), AstraZeneca (UK), ASML (Netherlands) and Mercado Libre (Argentina).

The biggest IPO globally last year was British chip design company Arm, which debuted shares on the Nasdaq with a valuation of US$54.5 billion. Another Australian home-grown tech hero, Canva, is considering an IPO on the Nasdaq in a year or two.

On this measure, the Nasdaq is effectively a global index, attracting some of the best companies in the world, whether they were founded Silicon Valley, Cambridge UK, or Perth, Western Australia.

Earnings growth is what matters in the long run

Over the short term, the market is driven by vagaries of investor sentiment, but over the long term the compounding of earnings growth is the true measure of value.

Given the outperformance of US equities over the last year, it's important to consider whether the primary driver of these returns has been multiple expansion (sentiment) or earnings growth.

Over the past months consensus earnings forecasts have been upgraded in the US and downgraded elsewhere.

A deeper dive into US equities shows that earnings upgrades are being driven by companies in the Nasdaq 100. In fact, ex-Nasdaq earnings growth is nothing to get excited about.

The stellar performance of the Nasdaq 100 in the 2023 calendar year can, in large part, be explained by the strong earnings upgrade cycle many of these stocks have enjoyed.

For example, Nvidia's EPS growth outstripped its incredible 239% share price return, meaning its PE ratio actually compressed in 2023. Amazon's PE also compressed on stronger earnings.

At an index level, the trailing PE for the Nasdaq 100 might sit toward the top end of its long-term range at 30x, but the 3-year forward PE is closer to 20x. The Nasdaq 100 arguably looks cheap by this measure.

If the companies in the index can deliver on the strong earnings growth reflected in the forward PE ratios, the index will be well-positioned to continue producing good returns.

Nasdaq companies have a history of beating consensus forecasts, and their long-run growth story is backed up by their commitment to innovation.

On average Nasdaq companies spend nearly seven times as much on R&D as non-Nasdaq S&P500 companies.

Over time this has created a virtuous circle, with the introduction of a new highly profitable product driving earnings growth and funding the development of the next generation of highly profitable products.

A complement for Australian equities

It's well known that the large-cap end of the Australian equity market is dominated by the Financials and Materials sectors, with Information Technology and Communication Services representing less than 10% combined.

By contrast, the Nasdaq 100, which has next to zero exposure to Financials and Materials, and a majority of its exposure in Information technology and Communication Services, may therefore be a well-suited complement to provide diversification benefits.

This sector makeup means that the Nasdaq 100 has a comparatively low level of correlation with Australian equities.

As a result, exposure to the Nasdaq 100, through an ETF like NDQ, can be used for part of a global equity allocation for diversification benefits, as well as for the potential for outperformance.

Get stories like this in our newsletters.