No Christmas miracle: RBA holds cash rate at December meeting

There's no early Christmas present for mortgage holders, with the Reserve Bank of Australia (RBA) opting to hold the official cash rate steady at 4.35% in its final monetary policy meeting of 2024. This decision keeps rates at their highest level since 2011, dampening hopes for a reprieve amid the festive season.

The RBA's stance comes despite seemingly encouraging signs on the inflation front. Headline inflation rose by just 2.1% in the 12 months to October - a three-year low and comfortably within the central bank's 2-3% target range.

However, the RBA's focus has shifted to trimmed mean inflation, a measure that excludes volatile price changes.

Eleanor Creagh, REA Group senior economist, says these underlying price pressures and "stickier" components of inflation combined with a resilient labour market has prevented an interest rate cut this year.

According to Creagh, this outweighs the recent National Accounts data, which showed Australia's gross domestic product (GDP) slow to 0.3%.

When looking at the value of goods and services produced per person in Australia (GDP per capita), this data shows that the economy has been shrinking for seven straight quarters. This indicates that, on average, each person in Australia is producing less than they were before - a sign of a recession.

Despite this, Creagh says the RBA is likely to keep rates on hold through the first quarter of 2025.

"... Unless there is an external shock or significant shifts in unemployment or underlying inflation, as it aims to sustainably return inflation to target."

Why trimmed mean inflation is the new goal post

The RBA's shift to trimmed mean inflation reflects its cautious approach. This measure, which excludes volatile items like electricity and fuel, remains above 3%, signaling persistent cost pressures in services and housing.

To some, this may seem like a shifting of the goal posts.

In its first monetary meeting of the year in February the RBA prioritised returning headline inflation to its 2-3% target range, forecasting it would reach the midpoint by 2026. Trimmed mean inflation wasn't mentioned in that statement.

However, surging electricity and fuel prices in mid-2024 forced a recalibration. State and federal energy rebates, combined with lower global oil demand, caused electricity prices to drop 35.6% - the largest annual fall on record - and fuel prices to decline 11.5% in the year to October, according to ABS data.

This volatility pulled down headline inflation but had little impact on underlying pressures. Trimmed mean inflation has stayed above target for 11 consecutive quarters. By September, the RBA adjusted its outlook: underlying inflation is now expected to return to target by late 2025 and approach the midpoint in 2026.

As the RBA explained in September: "While headline inflation will decline for a time, underlying inflation is more indicative of inflation momentum, and it remains too high."

No rate relief for mortgage holders this Christmas

While the RBA's reasoning is open for analysis, the cash rate decision means Australian households with variable-rate mortgages will continue to face higher repayments through the holiday season.

Even so, Canstar research reveals that out of those with an owner-occupier mortgage, 60% feel financially prepared for interest rates to remain elevated into 2025, while 28% say they are not prepared and 12% are unsure.

Impressively, one-third (33%) of borrowers who are prepared for rates to remain higher for longer say they'll still be able to meet the repayments if rates climb even higher.

This can largely be attributed to the July stage 3 tax cuts, which offered cost-of-living relief and supported stretched households.

Data from credit bureau illion found this money went to areas consumers needed most, paying down consumer debts rather than increasing discretionary spending - which could have been inflationary.

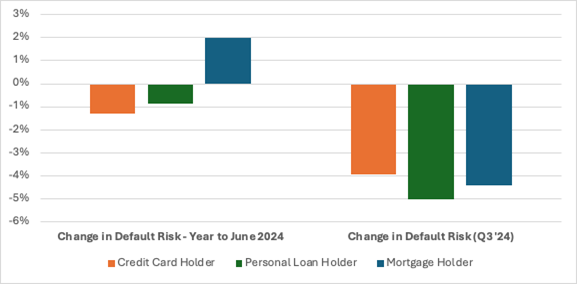

Illion's Consumer Credit Stress Barometer shows that in the September quarter, mortgage holder risk fell by 4% - a substantial reverse to the 3% risk deterioration seen in the prior quarter. This has led to an overall improvement of 2% in mortgage holder risk nationally, over the past 15 months.

However, illion's data showed that the economy is still weak in places. The credit bureau's head of modelling, Barrett Hasseldine explains, "Economic stresses are still evident, especially amongst 30-something mortgage holders."

"The outlook for lower income, mortgage-belt Australia and for the small business sector is still uncertain, and this is a large number of people."

Graham Cooke, head of consumer research at Finder, agrees, emphasising that many can't wait for a rate cut.

"Thousands of stressed homeowners can't manage much longer with soaring mortgage costs smashing household budgets. While we expect the RBA to start cutting the cash rate next year, many will struggle through the festive season with less money to spend than in previous years."

Aussies with the average home loan size of $641,416 are now forking out $3958 per month on repayments on average. That's $1453 more per month - $17,436 more per year - than they were paying before the RBA started lifting the cash rate in May 2022.

The next monetary policy decision will be announced on February 18, 2025.

Five tips to save for the holiday season

Although the cash rate pause may have dashed the hopes of any Christmas cheer for many mortgage holders, there are still ways to save money this holiday period.

Mortgage broker and financial literacy advocate Adele Andrews says it is more crucial than ever that Australians keep the purse strings tight throughout the holiday period - and well into the first quarter of 2025.

Here are Andrews' top five tips for making your holiday season budget go further:

- Leverage from shopback or cashback apps, when booking any holiday activities or trips.

- Look at experiences rather than gifts at Christmas - can you give something holistic that the whole family benefits from in one experiential gift, as opposed to material things?

- Price watch - sites such as CamelCamelCamel and Honey are great for watching prices of items you have your eye on - and alerting you to when prices drop.

- Review your home debt - sit with a mortgage broker who is prepared to analyse your mortgage, car, or personal loans and review better ways of structuring it and saving you money on your repayments.

- Make a weekly budget and stick to it. Have it on the fridge or somewhere visible and plan, plan, plan. You would be surprised at the impact that a visible, financial plan can have.

Get stories like this in our newsletters.