Slow turnaround starts to pay off for QBE Insurance

Greater focus and discipline are bringing improved results for this global insurer

QBE Insurance Group's turnaround is showing results after promising to do so for years. A simpler, more focused insurer is replacing a company that once seemed to want to insure everything, everywhere.

QBE is pulling back to where it has better prospects - Australia and parts of Asia, North America and Europe. Peripheral products and operations in South America and (other) parts of Asia have either been sold or wound down.

The reorganisation coincides with a detailed review of critical functions such as underwriting standards and pricing. These are basics for insurers but were flawed within QBE. The combined impact is that QBE is reducing risks where they previously festered.

Results for 2018 provide evidence of the improvement. Premiums declined as expected, as QBE pulled back in certain areas, with gross written premiums (GWP) falling 4% to $US14.2 billion ($20 billion). However, for those operations to which QBE is committed, GWP rose 2.5% to $US13.7 billion due largely to price rises.

Profitability showed a big improvement across all divisions, with the company moving from an underwriting loss to an underwriting profit. The combined operating ratio (COR) - which measures expenses and claims losses as a percentage of premiums - fell from 103.9% (a figure over 100% indicates an underwriting loss) to 95.7%.

QBE could achieve good earnings growth in the next few years if premium prices rise and the COR falls to the target of 94.5%-96.5%. The consensus is for the company to make earnings per share of $1 in 2020, compared with nearly 60c now.

Compared with its domestic peers IAG and Suncorp, QBE has better growth prospects yet it's a lower-quality business without clear competitive advantages.

QBE is largely a commercial insurer playing in markets with heavy competition. Around 8% of its equity is also tied up in mortgage insurance in Australia, of which it is the second-largest provider, and that could lead to some headaches if the housing market continues to fall.

In contrast, IAG and Suncorp are simpler and stronger businesses. They have large shares of retail insurance in Australia and New Zealand. Scale and brand matter here and the pair have combined those with solid margins and reasonable growth.

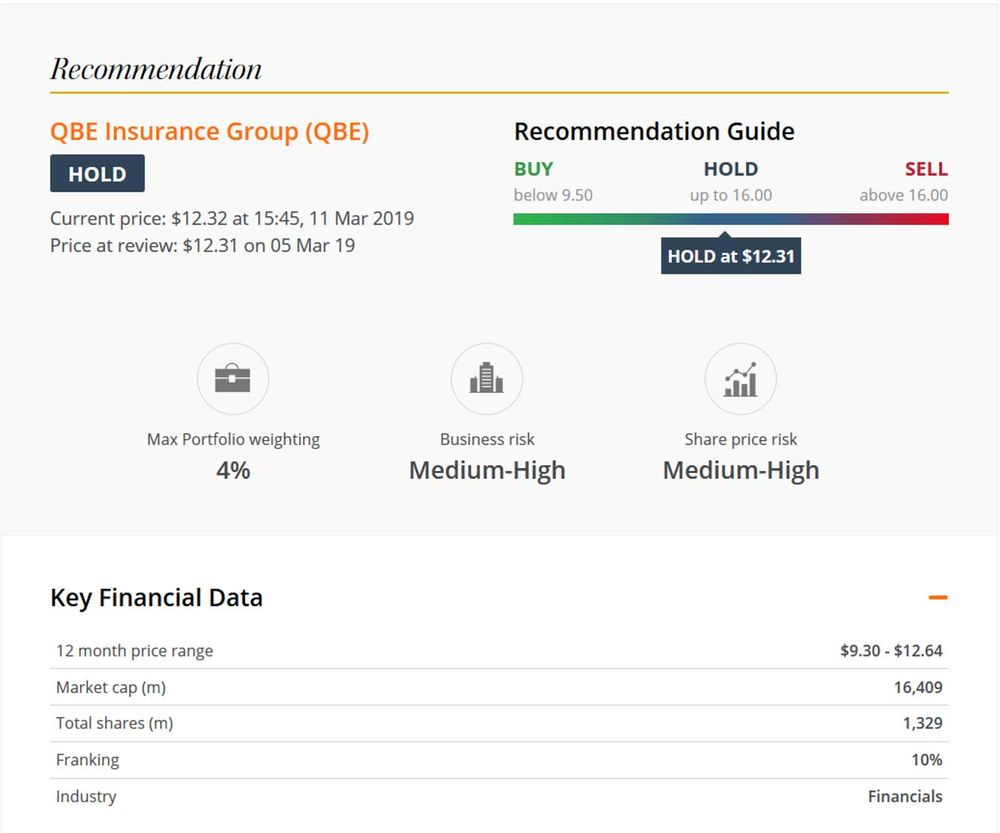

QBE is heading in the right direction, though we're some way off an upgrade. The stock trades at 1.4 times its book value, which is not that attractive for the risks involved.

That said, QBE's progress warrants an increase in our buy price to $9.50 from $8.50 but we'll leave the sell price unchanged at $16. HOLD.

Get stories like this in our newsletters.