Where to invest: SCT Logistics bonds

This week Money asks FIIG where to invest and its pick is SCT Logistics bonds.

SCT has issued two bonds, one fixed and the other a floating rate.

The floating-rate bond matures in just over three years with a yield to maturity of 6.43% a year while the fixed-rate bond has a longer term to maturity in June 2021 and has a yield to maturity of 7.13%pa.

Company description

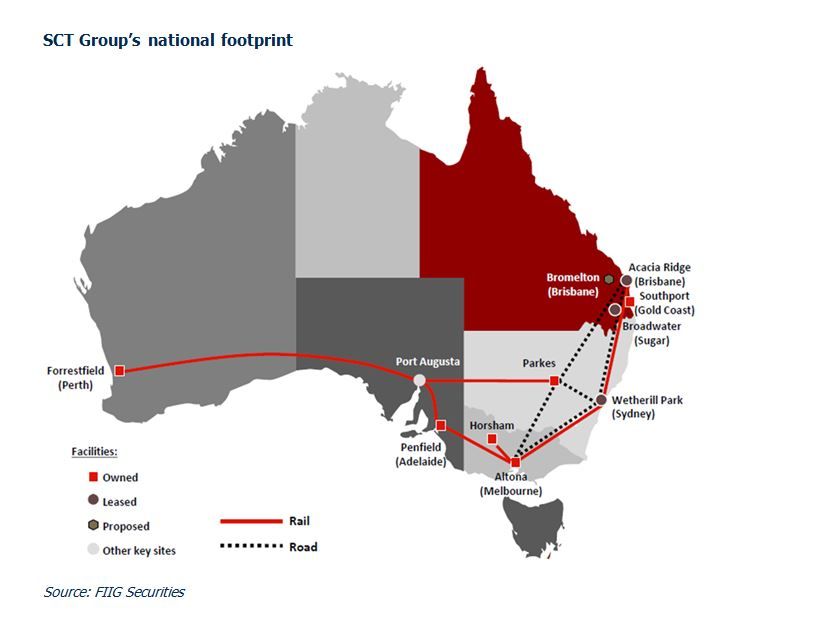

SCT Logistics is Australia's largest private rail freight operator with a 40-year operating history.

It provides a full suite of vertically integrated, national logistics services, at the core of which is Australia's most modern rail freight operation and national terminal footprint.

The business was established in 1974 as a rail line-haul service by Peter Smith, and ownership of the business has remained with the Smith family.

The company transports fast-moving consumer goods, beer, wine and materials, with limited exposure to goods used in mining and no direct exposure to commodities.

Its customer base includes major recognised brands and retailers such as Nestle, Fosters, Super Retail Group and Woolworths. The average tenure of its major customers is around 15 years.

SCT runs 11 weekly services over three rail routes, with most earnings generated from the Australian east coast/west coast corridor (40% market share) and the emerging north-south corridor.

Industry dynamics are favourable on long-haul routes, with rail about four times more fuel efficient than road on the east-west corridor. SCT operates Australia's longest general freight train at 1.8km, which is able to move 6000 tonnes.

Barriers to entry are high with large upfront capital expenditure requirements ($90 million-plus over the past five years) and stringent route accreditation being required before track owners allow route access.

Key financials - half year ended December 27, 2015

- - Half-year normalised EBITDA* of $21.2 million is tracking in line with the 2016 financial year research forecast of $42.4m on a pro rata basis and consistent with the turnaround that was expected for the business after the 2015 financial year. (*Normalised EBITDA calculated as profit before tax, $4.04m, adding back line items finance costs, depreciation and amortisation expenses plus normalisation adjustment of $600,000.)

- - SCT envisages that the second half of the year will be relatively consistent with the first half. If this eventuates then full-year EBITDA would be broadly consistent with the $42.4m forecast.

- - The net debt position has reduced by 15% from June 30, 2015 - from $149m to $127m. This is a function of the amortisation of equipment finance (flagged in research) as well as the increase in cash (see below)

- - Assuming EBITDA of $42.4m for the full year, we are seeing leverage (net debt/EBITDA) of 3.0x at the half year (a solid improvement from the 4.0x leverage at bond issue). With further debt reduction through amortisation, leverage could fall below 3.0x by the end of the year.

- - As flagged in the previous update on SCT, cash is up to $9.4m following the receipt of proceeds of a related-party business Logicoil.

- - Fixed assets with a written-down value of $164m as at March 2015.

Investor information

- Minimum investment per bond $10,000, with an upfront minimum of $50,000.

- No management or performance fees.

- FIIG is a dealer and we take a small brokerage fee when we transact (this is already included in the yield-to-maturity returns).

- A custody service fee is also charged.

- Wholesale investors only.

Get stories like this in our newsletters.