Why asset quality matters in uncertain times

When it comes to investing for income, one thing matters most: quality.

Strong investment portfolios don't happen by chance.

They're built with care, discipline and a clear focus on quality.

What makes a portfolio resilient?

The past 20 years have brought major challenges for investors. From financial crises to global pandemics and trade disruptions, markets have faced serious uncertainty. Yet, investment strategies that prioritise quality have continued to deliver steady income, protect capital and maintain access to funds. Some have even done so without a single investor loss.

The key is how the portfolio is built.

Diversification plays a big role. For example, a mortgage investment strategy can include thousands of individual loans, each carefully selected and spread across different borrowers, industries and locations. This helps reduce the impact of any single event or downturn.

In the private credit space, a key measure of quality is the loan-to-value ratio (LVR). While loans may go up to 80% LVR, keeping it closer to 65% provides a strong buffer. This means that even if property values fall, the loan is still well covered by the value of the property.

A lower LVR also reflects careful lending and a focus on protecting investor capital. It supports steady income and keeps arrears and losses low. In short, LVR is more than a number - it's a key part of a quality-first approach that delivers reliable returns without taking on unnecessary risk.

Who are private credit's borrowers?

Private credit mortgage investments often involve lending to 'complex prime' borrowers. These are financially strong individuals, such as doctors, pilots, business owners and self-managed super funds, who may not meet the strict rules of traditional banks. Their finances may be more complex, but they are still creditworthy.

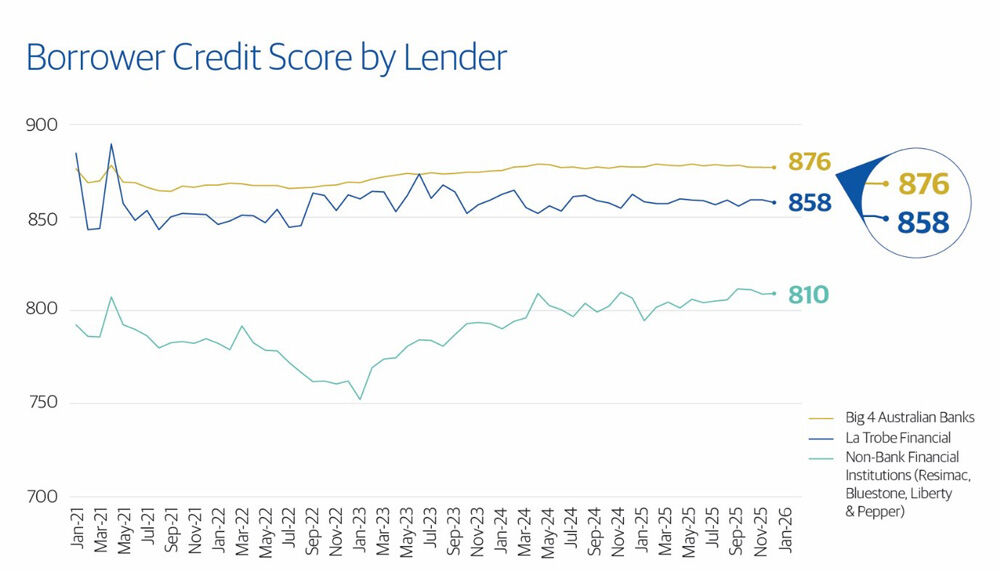

At La Trobe Financial, 96% of borrowers have no history of credit issues. Their credit scores are similar to those of customers at Australia's major banks.

A personal approach to lending

Banks, particularly post-global financial crisis, tend to rely heavily on regimented and automated lending systems.

This has seen them withdraw from lending into the economy where a more specialised or personalised approach is required to achieve an acceptable outcome for both the borrower and lender. Just because a bank is unable to make the loan, does not mean that one should not be provided.

Private credit lenders, like La Trobe Financial, take a more personal approach. Every loan application is reviewed by at least two experienced credit assessors. This hands-on process ensures that only high-quality borrowers are approved.

Mortgage brokers also play a key role. They help connect lenders with borrowers who need tailored solutions, helping to build a strong and stable portfolio for investors.

Different to a bank

Private credit funds are not bank accounts. They are investment funds, and their managers aren't banks they are asset managers.

By focusing on high-quality assets, strong credit checks and a well-diversified portfolio, private credit has and can continued to deliver for investors through all kinds of market conditions.

The numbers speak for themselves. La Trobe Financial's Australian Credit Fund portfolios have delivered steady income and full capital returns - even during market stress.

The 12 Month Term Account, for example, has a seven-year average annual loss rate of just 0.03%. And, this has been fully covered by the investor reserve, a built-in safeguard that protects against loan defaults.

At La Trobe Financial we believe that income-focused investing means not taking unnecessary risks with investors' capital. With the right approach, it's possible to earn strong, steady returns while safeguarding your capital.

*The variable rate of return is current as at November 1, 2025. The rate of return is reviewed and determined monthly, are not guaranteed, and may be lower than expected. The rate of return is determined by the future revenue of the credit fund, and distributions for any given month are paid within 14 days after month-end. An investment in the credit fund is not a bank deposit, and investors risk losing some or all of their principal investment. Past performance is not a reliable indicator of future performance. Withdrawal rights are subject to liquidity and may be delayed or suspended."

La Trobe Financial Asset Management Limited ACN 007 332 363 Australian Financial Services Licence No. 222213 Australian Financial Services Licence No. 222213 is the responsible entity of the La Trobe Australian Credit Fund ARSN 088 178 321. It is important that you consider the Product Disclosure Statement (PDS) before deciding whether to invest or continue to invest in any of the funds. The PDSs and Target Market Determinations are available on La Trobe Financial's website. Any Financial product advice is general only and has been prepared without considering your objectives, financial situation or needs. You should, before investing or continuing to invest in the La Trobe Australian Credit Fund, consider the appropriateness of the advice having regard to your objectives, financial situation or needs and consider the PDS for the fund.

When considering whether to invest or continue investing in the La Trobe Australian Credit Fund, you should be aware that (1) an investment in the fund is not a term deposit, and your investment is not covered by the Australian Government's deposit guarantee scheme. Investing in the fund has a higher level of risk compared to investing in a term deposit issued by a bank and (2) there are other risks associated with an investment in the fund. The key risks of investing in the fund are explained in section 9 of the PDS, available on our website.

Get stories like this in our newsletters.