What the arrival of Amazon will mean for Stockland

Rising bond yields have seen a sell-off in many 'income' plays in recent months, with the view that a strong income stream is not as enticing as it was.

One group which has certainly endured some weakness of late has been the Australian Real Estate Investment Trusts (A-REITs), with the retail segment seeing the most pain, given concerns over a cash-strapped consumer, along with the 'Amazon effect' as the US behemoth gets ready to be a major disruptor on these shores.

We have said for some time that interest rates have bottomed, and also that as a consequence the death of the multi-decade bull market in bonds is nigh. That said, we do not believe yields are going to escalate dramatically overnight, and as evidenced by Janet Yellen's testimony last week, the Fed (leading the way on tightening policies) is taking very much a softly, softly approach.

Demand for high-yielding income stocks, and particularly those with strong earnings growth potential is not going to suddenly evaporate, and as such we believe there are some select buying opportunities currently.

A standout case at the moment from our perspective is Stockland (ASX:SGP), which is one of the largest residential property groups in Australia.

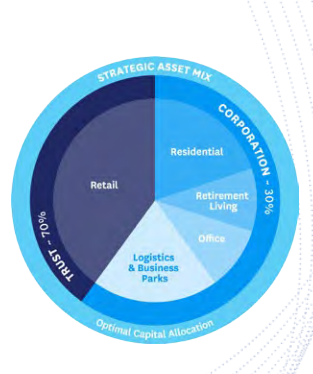

This may seem at odds with our view that the residential property market is near the top (at least in the hotspots such as Sydney and Melbourne), but there is more to Stockland than that. The company also has significant exposure to counter-cyclical assets in the retirement sector, as well as logistics centres, business parks, and office assets.

The company also has a hefty exposure to the retail sector, which again might be a reason that it is best avoided. However, Stockland's shopping centre properties are well positioned, with strong occupancy, and we believe that the fear and loathing over the disruptive impact of Amazon has actually gone too far, and created a value gap in the securities.

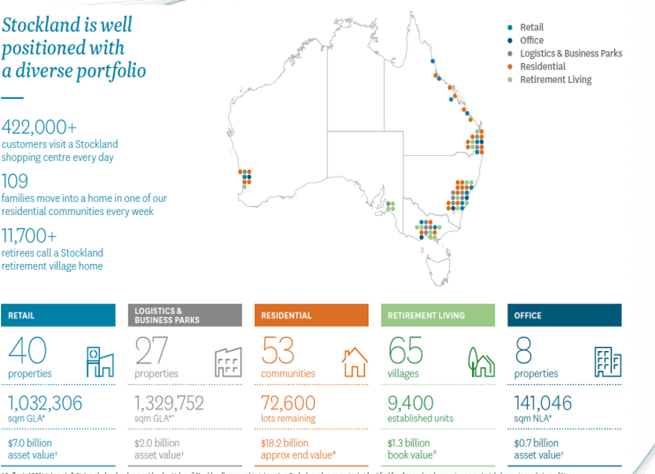

Stockland is one of the largest diversified property groups in Australia and has almost $16 billion of real estate assets. The company was founded back in 1952, and today owns, manages and develops shopping malls, logistics centres and business parks, office assets, residential communities, and retirement living villages.

A key attraction from our perspective is the diversity (as well as quality) of the asset base. The property footprint, while concentrated in residential and retail, is balanced to a degree by counter-cyclical/defensive exposures to other segments.

Looking at the two biggest sectors first, in retail, Stockland has more than one million square metres of gross lettable area, and also makes the claim that more than 422,000 customers visit a shopping centre each day.

The immediate thought is that the company is at the mercy of the 'decline' of retail, but the reality is that shopping centres are much more defensive than owning a set of individual leases. Safety in numbers as they say, or at least foot traffic. Moreover, tenants that are struggling can be replaced, and particularly by international brands that are widening their net to Australia.

On the residential side, the group has 53 communities, with an end value of around $18 billion. We have certainly expressed much caution about the Australian property market, and with lending rates heading up, we have been particularly wary of the apartment market, and the oversupply present.

Stockland however is focused more on affordable detached housing communities, targeting owner-occupiers (around 75%), and particularly first home buyers (around 55%). These groups should also continue to attract the 'social' support of government.

Residential property in any event in Australia is still strong, but a key point about Stockland is that it sells land rather than say apartments. The company can therefore quickly reprice upward and get margin expansion as land prices rise.

We also believe that Stockland has material earnings upgrade risk. The company saw EPS fall massively post the GFC and continues to rise off undemanding base comparables. This should mean that 7%-8%pa EPS growth should be very achievable over the medium-term, which would be excellent growth for a REIT.

Stockland trades on a forward earnings multiple of 13 times, and offers a yield of almost around 6%, with a history of steady dividends (which should also cap share price downside). Trading around $4.25 currently, the stock is also backed by net tangible assets of around $4.15 per share, with meaningful scope for earnings per share growth.

To receive a recent Fat Prophets Report, click here.

Get stories like this in our newsletters.