What to do with your superannuation when you retire

Retirees who plan ahead will be better equipped to ride out any shock

To what extent should super funds prepare their members for a market correction and give them strategies to minimise the impact?

During the GFC many people panicked and fled to the safety of cash, only to lock in their losses.

This was especially the case for pre-retirees and those in retirement.

The prospect of taking another hit at the end of their working lives prompted many to become risk adverse and seek safe harbour in low- risk, low-return investments.

Financial consultant Rice Warner says funds need to be more proactive and help members manage market volatility better.

Its report "Preparing Members for a Market Downturn" shows how a "bucket strategy" of sticking to growth will outperform investing higher proportions in cash and switching to cash at the bottom of the market.

"When people are upbeat about the economy, prices often rise exuberantly. When the market turns down significantly, it is usually fast and without notice," according to the report.

"So while we can say that investment markets follow a cyclical pattern, no one can predict when the market will rise or fall. We also know that markets usually recover their losses over time, sometimes quite quickly."

While default super funds have been positive for each of the past nine years, with many close to, or above, double-digit returns, Rice Warner warns that a sharemarket reversal is becoming more and more likely.

"Could we have a negative 25% return on equities leading to a 10% or more fall in fund returns this year or next year? If the markets do take a step back, this will have a big impact on super funds and their members, particularly the growing numbers of retirees."

The effects could be magnified for members who find that they are bearing more investment risk than they realised and lock in losses by moving to more defensive strategies at an inopportune time. "Rather than waiting until the event, funds should prepare now through active communication to those at risk."

Rice Warner questions the investment return targets of many funds - typically CPI plus 3%-4% over a rolling 10-year period - and says they need to ask themselves whether these targets are realistic and communicate the risks to members.

Since experience from the previous financial crises shows that many members will switch out of growth assets into cash at the bottom of the market and select investments that lead to lower returns, Rice Warner calls for more tailored advice.

For those close to or in retirement who will have liquidity needs, funds should encourage members to calculate their forecast pension payments and put away up to 18 to 36 months of their expenditure needs into a "cash bucket".

Excess investment returns or income from dividends could go into this bucket to reduce downside risk.

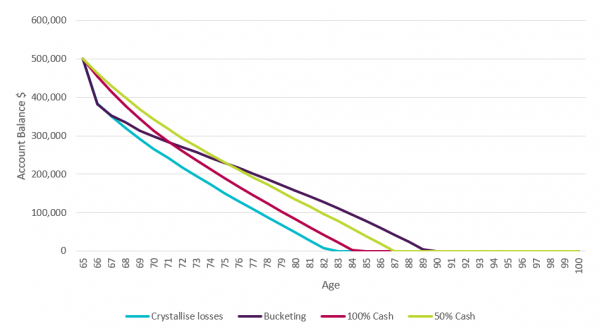

Benefits of a bucket strategy

Rice Warner gives the example of a member who retires at 65 with $500,000 and allocates a year's drawdowns to cash, then 50% in a balanced portfolio to cover the next 10 years and 50% in high growth for the period thereafter. Then there is a market crash.

- The correction results in a -15% return on the high-growth assets and -10% on the balanced portfolio.

- The funds recover back to the base after three years.

- After the recovery the cash portfolio earns 2.5%pa, the balanced portfolio earns 6%pa and high growth earns 8%pa.

As the graph shows, the simple bucket strategy of sticking to growth outperforms investing higher proportions of the portfolio in cash, as well as crystallising losses at the bottom of the market. This strategy sees the retiree through to 90.

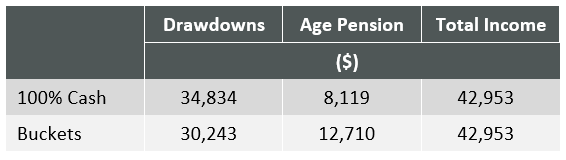

Age pension provides a safety net

Critically, as the member's overall assets fell in this scenario, the part age pension grew. The bucketing solution versus 100% cash meant the member's age pension increased by more than 50% in the first year.

While the drawdowns from super were $4500 lower, the members made up the shortfall, thanks to means testing of the age pension.

"Effectively, the age pension becomes a put option on any downturn in market prices. It also means the member's cash bucket lasts longer, allowing a higher chance of recovery without eating into capital," says Rice Warner.

"Given asset allocation is the No. 1 driver of net returns to members, taking small and simple steps such as the example above has the potential to protect retirees and deliver a great outcome."

Get stories like this in our newsletters.