This is how Lifecycle super products actually work

What are lifecycle super products, how do they work, and should you choose one for your default MySuper investment strategy?

- In lifecycle investments you are assigned an asset allocation based on your age.

- They are designed to insulate older fund members against the impacts of a sudden fall in capital markets when they are approaching retirement.

- The way the asset allocation changes as you get older is known as the lifecycle investment's glidepath trajectory.

Lifecycle superannuation products are investment choices where the asset allocation is determined by how old the member is or how long they have until they expect to retire.

They are becoming very popular as they now make up almost half of all MySuper products. They are favoured by not-for-profit and retail super funds alike.

The idea behind lifecycle investments is that when you are young you have a long time until you retire, so you should be comfortable taking more investment risk with the expectation that you will achieve higher investment returns.

But as you get older, particularly in the decade leading up to retirement, you become more focused on preserving your capital so you lower your investment risk by reducing your exposure to growth assets like shares and property.

This is done by having more of your superannuation savings switched across into defensive assets like bonds and cash.

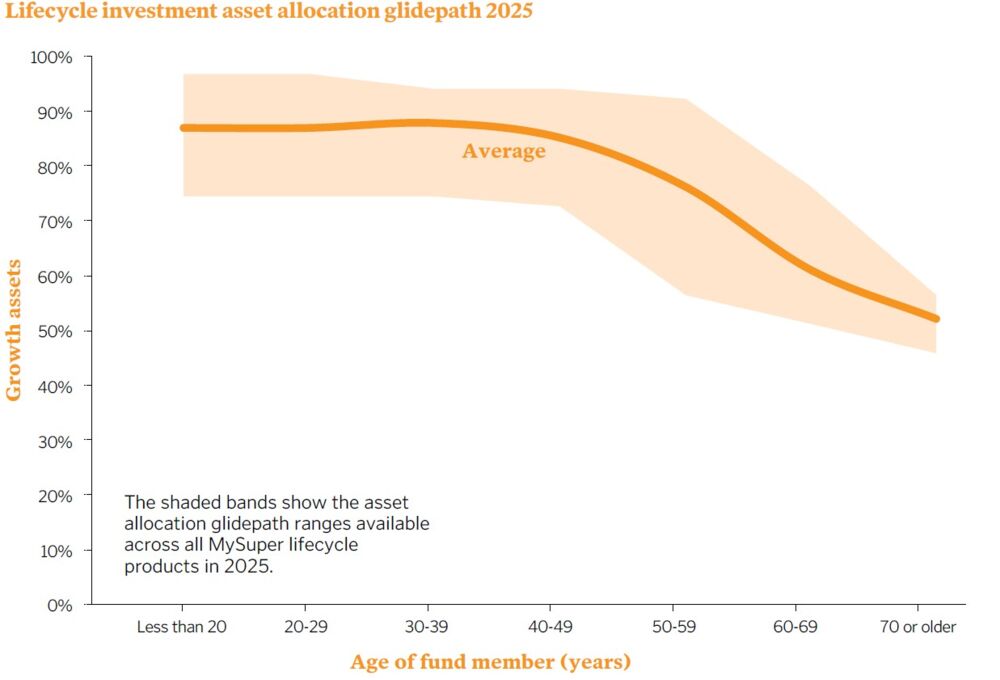

In practical terms, this means when you are under age 40 your exposure to growth assets will average almost 90%, before progressively reducing to an average of 70% by the time you are in your 50s.

By age 65 when most people retire, the average lifecycle MySuper product has about 55% of its portfolio invested into growth assets. This is illustrated in the chart below.

Are lifecycle investments safer?

Lower investment risk doesn't come without potential cost.

This is because when you choose a lifecycle investment - whereby as you get older more of your account balance is allocated into defensive assets - it means that over your superannuation life your portfolio is more conservatively invested than if you had chosen a traditional single-strategy diversified growth portfolio.

The way this could impact your account balance is that when you are older and have a larger account balance, the lower expected investment returns delivered from a typical lifecycle superannuation product designed for older people means you will not get the same compound interest boost as fund members invested into a traditional diversified growth portfolio.

As a result, for a lifecycle strategy to pay off, you are in effect betting the investment markets will fall sharply in the years approaching your retirement.

How you feel about these investment risks determines whether you should choose to be in a lifecycle investment strategy.

| A quick guide to the different types of super funds |

| Introducing the experts who run your super fund |