Introducing the experts who run your super fund

MySuper products and super funds use many different expert advisers. Understanding the different roles they all play will help you make better sense of how a fund operates.

- The people who run your fund are called trustees.

- Investment managers look after your fund's investments.

- Trustees often use asset consultants to help them choose which investment managers to use, and to help them decide their investment strategy.

- Specialist fund administration companies help your trustees run the back-end administration of your fund, including its call centre and making sure it complies with all government rules.

A MySuper product or super fund is nothing more than a savings fund that you invest in during your working life so that by the time you retire you have accumulated enough money to help pay a reasonable lump sum or pension.

To understand how good your MySuper product or super fund is likely to be in delivering this, it will help if you understand the main roles people play at a super fund so you can properly judge each person against his or her role. To do this, you need to understand what these roles are and what they mean.

RSEs and trustees

Super funds are operated by companies that are overseen a board of directors, where each director may also be called a trustee. To run a super fund these special companies have to apply to the superannuation regulator, the APRA, for permission to become a Registrable Superannuation Entity (RSE).

The boards of these RSE companies usually have between four and 16 trustee directors. Some operate as 'equal representation trustee boards' - for example, in-house corporate super funds, government funds or industry funds - have half the trustees appointed by the fund sponsor (say, the employer) and half appointed by members or people representing the members (say, a union).

More funds are now appointing independent trustees.

In many commercial products or funds, such as master trusts, the trustee role is played by an approved trustee company that is specially set up to provide these services. Approved trustees are registered with APRA, and have to satisfy a range of licensing requirements before they can offer their services.

Trustees are not expected to be experts in all aspects of how to run a product or fund, but they are expected to know how to manage people who are. Your fund's trustees are there to represent you and make sure the fund is working properly for you and its other members. If anything goes wrong with the fund, the buck always stops with the trustees, and this motivates them to make sure things are working properly for you and its members.

If anything goes wrong with the fund, the buck always stops with the trustees, and this motivates them to make sure things are working properly. A good trustee board will always listen to the members and will work to keep them informed about how the fund is performing.

Investment managers

Investment managers are expert companies that specialise in managing investments. They may also be called fund managers, money managers or asset managers.

Their job is to decide what assets to buy and when to sell or hold these investments to make the best return for the super fund members. Of course, while some investment managers are better than others, for the most part the crucial decision they have to make is the type of investments they buy into, such as shares, property or government bonds.

While the investment managers look after the investments, they do not operate the super fund itself. This means, for example, if you have problems with how your MySuper product or fund operates, what investments have been chosen or what other investment managers are being used, this is something you should complain about to the trustees.

MySuper products or super funds generally use up to 50 different investment managers, and of all the fees you pay, two-thirds goes to these managers. Remember, it is the investment managers who run the investments, while the trustees run the actual super fund.

Asset consultants

When it comes to using investment managers, MySuper products and super funds have to choose from around 900 or more investment managers in Australia, and the thousands available overseas.

Not surprisingly, they often need help from special advisers who are experts in understanding investment managers and how to choose between them. These experts are called asset consultants or sometimes investment consultants.

Asset consultants help super fund trustees decide how much money they should invest into particular types of investments or asset classes, for example, how much money a fund should invest into overseas shares compared to Australian government bonds.

| CONSUMER WARNING: PRODUCTS NOT FUNDS

s your super with a product or an actual fund? Funds are run by RSE trustees that are regulated by the government. A product is run by a finance company. Even though the product sits within a fund and the finance company itself is licensed, the product's investments are directed by the finance company, not the fund trustees. As a result, the lines of control are a bit different. If you choose to use a superannuation product that is run this way, you should check that you trust the finance company offering the product. This is because if something goes wrong it could be harder to sort out who is responsible. To address these concerns, some of these products now have advisory boards to act as informal trustees. |

Some personal master trusts that operate dozens, or even hundreds of different investment options, may also use investment research companies to help them choose and assess investment options before they are added to a super fund's investment menu.

In recent years, some super funds have started outsourcing their entire investment operations to asset consultants, who are then assigned the complete task of designing the investment strategy and choosing the investment managers for the super fund.

This is called 'implemented consulting'. This arrangement is generally used by only the biggest employers running in-house corporate super funds, as most usually outsource their whole fund - rather than just parts of the fund - to an industry fund or a master trust. Some smaller industry funds have, however, started using implemented consultants so they can get access to the same economies of scale as bigger funds.

Because some asset consultants have been so successful with their advising services, they have now adapted these into their own master trusts that they offer to employers and consumers. When this happens, consultants cross the line from being just consultants to being fully fledged product operators, and this is how you must judge them.

Administrators and platform providers

Superannuation trustees sometimes use specialist companies to help them administer their product or fund. These specialist administrators are experts in the government rules of operating a fund and making sure the fund meets all the compliance and regulatory requirements.

Administrators also make sure that every time an employer pays a contribution into an employee's super fund account this money is recorded properly.

Annual reports, member statements and government compliance reports are all produced and managed by your super fund's administrators, and it is usually the fund's administrator that operates the call centre that answers when you email or ring up with an enquiry.

Administrators of master trusts are sometimes called 'platform providers', as they provide the back-end investment platform that makes up the master trust, in addition to just providing regular administration services. In doing this, platform providers offer a mix of asset consultancy expertise to the funds, and in this way they are usually more sophisticated in their operations than regular super fund administration companies.

Insurers

Insurers are the insurance companies used by your super fund to provide the life insurance policy that they offer you.

Custodians

Many MySuper products or super funds also use special companies called 'custodians' to hold their assets and to coordinate and keep track of the investment managers used by the super fund.

Custodians act as an important check for super funds because they help insulate the super fund from fraud and dubious investment transactions. If your fund has a custodian in place it means that if an investment fraud was perpetrated on the fund, the custodian would foot the bill, because a big part of their job is protecting the fund from fraud.

Most good MySuper products or super funds use only very large and highly expert custodians. If your fund, however, does not use a custodian that is separate to the super fund - that is, they try to handle this role themselves - make sure you understand how the super fund does this, because if it is not handled properly your super savings could be at risk.

| This is how Lifecycle super products actually work |

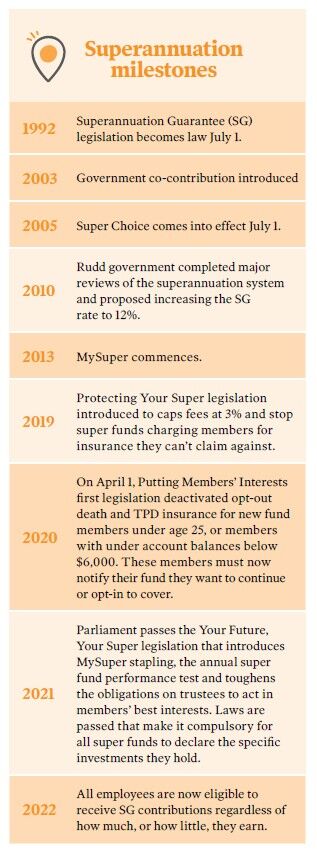

| A quick history of superannuation in Australia |