How to manage super as a small business owner

Superannuation has been designed for employees, not for business owners. But with the right advice, small business owners can use their business assets to boost their superannuation.

- Small business owners need to understand the capital gains tax (CGT) lifetime cap and how the CGT concessions work.

- But they should talk to their tax accountant because these arrangements can be complex.

Building a business takes time and money. Did you know that when assets held by a small business are sold, the proceeds can be contributed into super to increase your retirement savings significantly?

It is hard work being self-employed, and probably the last thing you'll be thinking about is your own superannuation.

You've got overheads, mortgage repayments, salaries and insurance, and you need to keep the business running.

There are four capital gains tax (CGT) concessions for small business regarding the sale of a CGT asset. If sold, the proceeds of the sale of CGT assets used in a small business can be contributed into superannuation.

However, there are certain conditions that must be satisfied before these concessions can be applied.

Following is a general summary that describes how these CGT business concessions work. But it's a complex area that usually requires some consultation with an accountant or tax adviser.

Basic conditions

Certain basic conditions must be met by the small business for it to be eligible for the small business CGT tax concessions, such as:

- Net value of the assets owned must not exceed $6 million or the aggregated turnover of the entity and related entities must be less than $2 million.

- Active asset test - the asset sold was used or held by the small business for explicit use in a business

- Additional rules apply if the asset being sold is a share in a company or an interest in a trust, including there must be a 'significant individual', and the entity claiming the concession must be a 'CGT concessional stakeholder' of the company or trust.

| Entity refers to an individual, partnership, company or trust.

A CGT concession stakeholder is either a significant individual in the company or trust and also a spouse of the individual, who participates in the voting, receipt of dividends, income or capital distributions. |

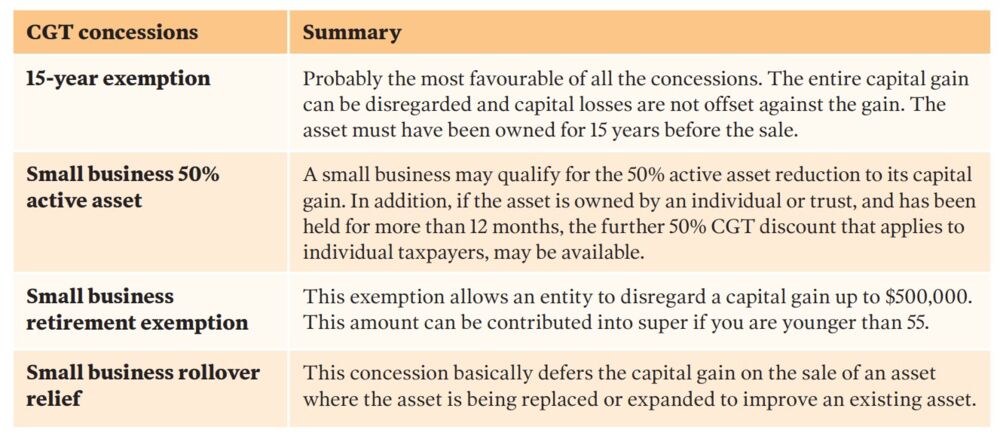

Small business CGT concessions

There are four small business CGT concessions available to a business owner for the sale of a CGT asset, as shown in the following table.

The amount you can contribute into superannuation using small business exemptions has a lifetime cap of $1.865 million for the 2025-26 financial year (the cap is indexed), which means the proceeds of the sale of an asset can count towards the lifetime cap and not affect your non-concessional cap.

The CGT lifetime cap contributions arise from the application of the following two concessions:

• The small business 15-year exemption.

• The small business retirement exemption.

Contributions relating to the 15-year exemption

If a business owner applies the small business 15-year exemption (the asset was owned for at least 15 years) towards their assessable capital gain, the proceeds can be contributed to superannuation as a CGT lifetime cap contribution.

There are other conditions that must be met, but this gives you a basic understanding of the exemption.

| EXAMPLE

Sharon, age 64, has owned her cattle farm since 2021 and sells it in 2024. By disposing of the farm and assuming that a capital gain was triggered, Sharon could apply the 15-year exemption to disregard the capital gain. Sharon received $950,000 from the proceeds of the sale of the farm and she's eligible to contribute to superannuation. Sharon can make a CGT lifetime cap contribution of up to $950,000 (the entire proceeds of the sale as it is less than the lifetime cap). |

Contributions relating to the retirement exemption

If you apply the small business retirement exemption, a capital gain can be exempted to an amount of $500,000 (this amount is not indexed), and the exempt amount can be contributed to superannuation as a CGT lifetime cap contribution.

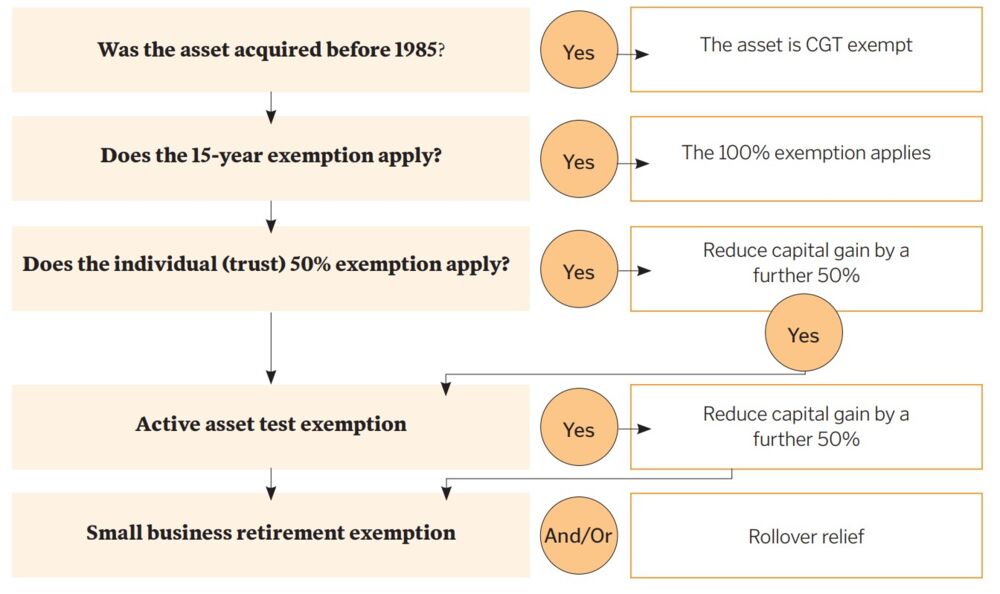

Tip: If you are age 55 or younger, the retirement exemption amount must be contributed to superannuation; if you are older than 55, there is no requirement to direct the amount into superannuation. The small business CGT concessions are a strategy that can save you a lot of tax, and can also boost your superannuation savings. The small business CGT concessions are generally considered in the following order:

| CASE STUDY

David, 53, is a small business owner and has sold an active asset that he has held for five years. He would like to contribute the proceeds of $500,000 to his superannuation. Being a small business owner, David may be able to use the small business CGT concessions to reduce all or part of any CGT liability on the sale of the asset, and at the same time build his retirement savings. David has some options available to him. Small business retirement exemption: David could contribute the entire proceeds of the sale to superannuation under the CGT retirement exemption, and any capital gain would be disregarded up to the maximum lifetime amount of $500,000. Concessional contributions: David could choose to make a tax-deductible concessional contribution of up to $30,000, and contribute the balance as a combination of non-concessional and/or contributions using the small business retirement exemption. Non-concessional contributions: David could choose to contribute some of the proceeds as non-concessional contributions (up to $120,000pa or $360,000 if invoking the bring forward rule) and the balance using the small business retirement exemption. 15-year exemption: In this example David did not own the asset for long enough to apply the 15-year exemption. However, hypothetically David could use the 15-year exemption in the future if he sold an asset that met all the requirements. Remember that the CGT lifetime cap of $1.865 million (indexed) applies to super contributions that arise from both the small business retirement exemption and the 15-year exemption. If David has already 'used up' $500,000 as a small business retirement exemption contribution, he could still make an additional contribution of up to $1,280 million under the 15-year exemption within the current CGT lifetime cap of $1.865 million. |

| How to find the best MySuper product for you |

| How to choose the right super fund |