Thirty years since the world crashed: lessons from Black Monday

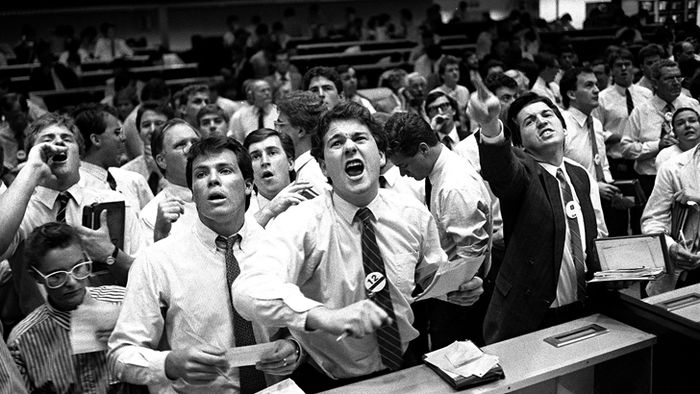

Black Monday for the US market became Black Tuesday in Australia.

The US market had fallen by 22% on Monday night, October 19, 1987, and the Australian market crashed by 25%.

My recollections are that the warning signs were observable earlier in 1987.

The US equity market had peaked in August and staged a weak recovery before weakening in the week before October 20.

More than most markets, the Australian equity market had been driven by debt, with much of it feeding the corporate plays of many long-forgotten entrepreneurs.

However, the biggest and most memorable debt player was Robert Holmes a Court, who had been stalking BHP through his debt-laden Bell Group.

He may not have invented leverage but Holmes a Court convinced our major banks to lend against the listed security of his massive BHP holding, the price of which had been constantly massaged higher through takeover bids, option trades and hedging.

That leads me to my lessons from the '87 crash.

First, the benefits of "leverage" built in a bull market and based on market prices (for security) are totally usurped in a correction.

Twenty years later, in 2007, the lessons of leverage had been forgotten and many a leveraged portfolio was wiped out in 2008.

Second, observe and therefore benefit from the effects of forced selling.

Leverage transfers control of the equity asset from the investor (with leverage) to the provider of the leverage. The bank or financier will always cut a margin loan to recover their exposure.

Buying from banks or forced sellers is a lucrative practice.

Third, every economic and therefore stockmarket cycle matures into a "nonsense" stage.

The maturity of a market is not measured by the maturity of the participants but the rehashing of hope that is sold to investors who come late to a bull market. The catch-up investors who are chasing a bull market always push it beyond reality.

While high pricing is a feature (well above value), it is more starkly seen in the craziness of the "new" business concepts that emerge in a tired bull market.

I recall Perth entrepreneurs in 1987 claimed they had discovered that water could be converted into a type of oil for engines.

Another classic was the entrepreneur who invented (and floated on the ASX) a non-flammable substance that could be used to build aircraft.

A passenger would not be burnt in an air crash - if they survived the impact from falling 40,000 feet!

Finally, history repeats and the basic traits of human fragility are constant.

With regards to equity investment, we all want to believe that this time it's different (but it never is); that equities will never fall or fail (they will); that entrepreneurs will not be driven by greed and feed off the greed of investors (they mostly do); and that value-based investing is a fallacy whose time is over.

Sorry, it always will endure and for much longer than a normal human life.

Get stories like this in our newsletters.