Trump's tariffs are here - what to do with your money

Donald Trump said he'd bring back tariffs and now they've landed, taking effect today.

Far from being just another negotiating tactic, the US president has gone further, adding new tariffs on Chinese imports and refusing to grant exemptions. Markets are reacting accordingly, with the recent chill turning into a full-blown fever as world teeters on the edge of a trade war.

Investors are jittery, the global outlook uncertain, and the question many Australians are now asking is: what do I do with my money?

Trump slump: How bad is it?

If you're exposed to international shares, especially in the US, the numbers aren't pretty.

The S&P 500 has tumbled 19% since February, its worst stretch since the COVID crash in 2020. The Nasdaq is down more than 20%, dragged lower by big names like Nvidia, Apple and Tesla.

The Russell 2000, which tracks smaller US companies, has lost 19.7% since Trump returned to office. All up, around US$6 trillion in market value has been wiped from US equities in just two days.

It's not just America. The MSCI World Index, which tracks developed market shares across 23 countries, is down 17%. In Australia, the ASX 200 has held up better but still lost 10% in three days before clawing back 2% on Tuesday.

But that rebound may not last.

"It has all of the hallmarks of a dead cat bounce," says Capital.com analyst Kyle Rodda, referring to a short-lived recovery before markets fall further.

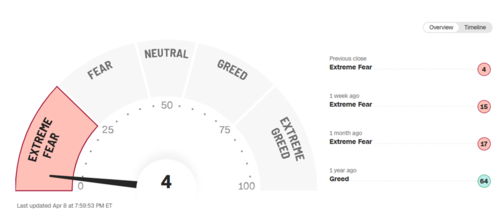

Fear is spreading

Investor mood has flipped. CNN's Fear and Greed Index shows sentiment has swung deep into "extreme fear" territory. Share price momentum has dried up, trading activity is down, and what little activity there is tends to be selling.

The American Association of Individual Investors (AAII) just posted one of its most bearish sentiment readings ever. Some 62% of respondents said they expect stocks to fall, ranking behind only the 2009 financial crisis and the 1990 bear market.

Add in fears of a US recession and the threat of stagflation, the toxic mix of weak growth and rising prices, and it's easy to see why people are nervous.

"Stagflation can be particularly painful because the uncertainty that comes with a downturn in the economy is compounded by the erosion of wealth through higher prices," says Ed Monk from Fidelity International. "It's a combination that markets hate."

Australians aren't immune. The Westpac-Melbourne Institute Consumer Sentiment Index plunged to 86.6 following the tariff news, down sharply from 93.9 and well below the neutral 100 line.

Matthew Hassan, head of Westpac's Australian macro-forecasting division, notes the "clear risk of more significant sentiment declines" as the global situation deteriorates.

What should Australian investors do?

With short-term forecasts uncertain, it's easy to buy into the doom and gloom. However, it may pay to step back and zoom out.

AMP economist Shane Oliver says investors should keep in mind that periodic share market corrections and occasional bear markets are a normal part of investing in shares.

"Shares climb a wall of worry over many years with numerous events dragging them down periodically, but with the long-term trend ultimately up and providing higher returns than other more stable assets," Oliver says.

Should you move your super?

Turbulence like this often prompts people, especially those nearing retirement, to consider switching their super to more conservative options.

It's a natural impulse. No one wants to see their nest egg shrink right before they need to access it.

But Oliver warns that making moves in the heat of the moment can do lasting damage.

"This strategy could turn a paper loss into a real loss with no hope of recovery," says Oliver. "Even if you get out and miss a further fall, the risk is that you won't feel confident to get back in until long after the market has fully recovered."

This played out during the 2020 pandemic crash. Many nervous investors locked in losses of up to 30% when they switched out of growth options, only to miss the rebound that followed.

"The best way to guard against deciding to sell on the basis of emotion after falls in markets is to adopt an appropriate long-term strategy and stick to it."

Is it time to buy the dip?

Once the panic subsides, another instinct kicks in: the urge to buy cheap.

Volatility can create opportunity. If you'd bought the ASX 200 at its pandemic low, you'd have seen a 30% return within 14 months.

As Warren Buffett famously said, "Be fearful when others are greedy, and greedy when others are fearful."

But timing the bottom is notoriously difficult. Instead, Oliver suggests using dollar cost averaging, which is a more measured approach.

According to research by Charles Schwab covering market data from 2001-2020, even if you consistently made badly timed investments, you'd still be US$76,000 better off than if you had not invested at all - stayed in cash.

Those who took a dollar cost averaging approach to investing were US$90,000 better off than those who stayed in cash, and for those rare folk who timed the market perfectly you'd be US$107,000 better off.

"Fortunately, the Australian superannuation system does just that by regularly putting money into shares for employees (via their super) taking advantage of the fact they are cheaper," says Oliver.

What about dividends?

While share prices have fallen, dividends remain a bright spot.

Oliver says that while the rebound in interest rates since 2022 reduced the yield advantage shares had over cash, it's likely now starting to wide again with the RBA looking to cut rates.

This resulted in more than half of Australian companies lifted their dividends during the recent earnings season. For income-focused investors and retirees, this could be a reason to stay the course.

"The income flow from a well-diversified portfolio is likely to remain attractive," says Oliver.

How can you protect your mental health?

Market sell-offs always come with a flood of headlines, opinions and forecasts. Right now, the noise is deafening.

That can make it harder to think clearly, especially when it comes to something long-term investing.

All of this makes it harder to stick to an appropriate long-term strategy, according to Oliver which is particularly important when it comes to super as it's seen as a long-term investment, except for many of those near to retirement.

"So best to turn down the noise and watch the third series of White Lotus or Brady Bunch re-runs."

Get stories like this in our newsletters.