How to pay less for health insurance (and why it's worth having)

Sydney man Martin, 31, is constantly on the move, with cricket every summer, football in winter, spin class, running festivals and yoga. He is healthy - and committed to staying that way - but he's always had health insurance.

"I've always found it an investment worth paying for," he says.

"There's a lot of debate, and I think what potentially confuses the issue is when the focus is on taxes and rebates and not on health coverage and treatment outcomes.

"We are fortunate to have a world-class public hospital system, but I believe it's good to have additional cover for elective treatments that you know you will need."

Martin had four impacted wisdom surgically teeth removed in his early 20s, and hospital cover provided peace of mind, he says.

"The cover was worth it for being able to schedule it at a time of my choosing, and having a private room for recovery."

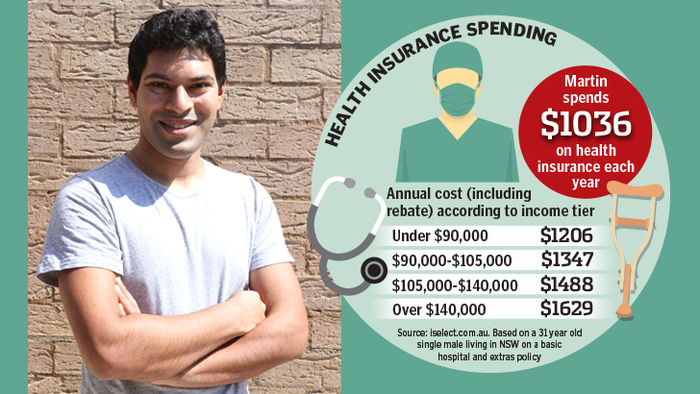

What is he paying?

Currently single, Martin pays $1036 a year ($518 every six months) for Medibank basic hospital and basic extras.

"This includes a reduced rebate because I'm a higher income earner," he says, "so I've opted to pay the extra now instead of the tax adjustment in my tax return."

How does he do it?

"Medibank had the best option when I turned 25 and was kicked off my parents' cover," says Martin.

The policy had zero excess for hospital cover for young singles.

"They are no longer the cheapest, but they've been good enough for me to stay." Once you've found a good price, the next step is to get value for money out of your premiums, he says.

"I buy a new pair of prescription glasses each year, and get about half back on my annual dental check-up, so my extras cover is worth it. Medibank also provides a 15% discount to existing customers on travel insurance, which I take advantage of when I travel overseas."

How can you do it?

Martin's tips

- Pay annually before the premium increase on April 1 each year, or schedule six-monthly premiums to be paid in March and September

- Take a good long look at extras cover. Don't cover yourself for alternative therapies if you don't need them.

- Read your policy to find what other benefits your health insurance offers, such as discounted travel insurance, subsidised gym membership or discounted movie tickets.

Money's tips

- Don't assume couples membership is cheaper. Research costs for both individuals and shape extras cover to their needs.

- Make sure your policy includes ambulance cover. Not all private health insurance policies include coverage for ambulance trips, and it can also vary by state.

- Only hospital cover delivers tax benefits. Taking out an extras-only policy will not exclude you from the Medicare levy surcharge. If you earn over $90,000 (single) or $180,000 (couple) and are looking to save on tax, make sure your private health insurance includes hospital cover.

- Consider paying a higher excess or co-payment. (Remember, to avoid the Medicare levy surcharge you can't have an excess of less than $500 if you're single or less than $1000 for couples/families.

- Ask your health fund if it offers a discount for paying via direct debit each month.

- Find out if your employer has a corporate fund; it could mean a significant discount.

Have you slashed your health insurance costs? Let us know in the comments!

RELATED: Meet the millenial paying just $17.50 a month for her smartphone

Get stories like this in our newsletters.