Why Aussies need to invest in more than property

Australians are stockpiling their wealth in residential property, with new data showing around two-thirds of household wealth is now held in bricks and mortar.

This proportion which has increased over time as property values surge, raising the need for Australians to diversify into other more defensive asset classes to reduce their financial risk.

While money cannot buy happiness, it is an important means to achieving higher living standards.

Recent data from the Australian Bureau of Statistics (ABS) shows that household net wealth rose to a record $16.2 trillion in the March 2024 quarter, boosted by a record level of property assets of $11.0 trillion.

The included a huge $200.5 billion rise in residential property values over the quarter, with the supply of housing unable to keep up with meet demand. As a proportion of net household wealth, residential property accounted for around 67.9%, up from 61.7% in December 2020.

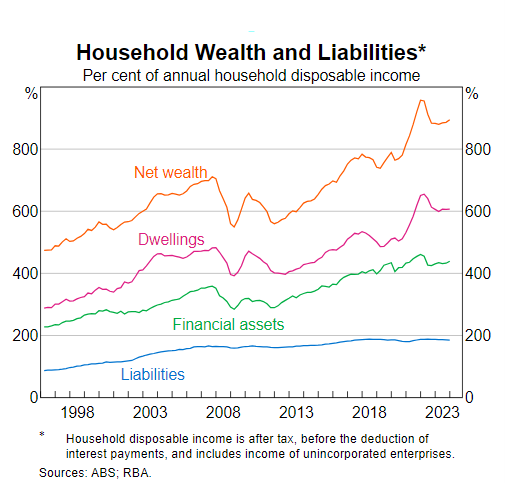

The ABS data shows that the key driver of household wealth gains in recent years has been rising property prices. That growth in the value of residential dwellings has outstripped growth in mortgage liabilities, as the chart below from the Reserve Bank show, indicating Australians are getting richer.

In terms of other assets, households also held $1.46 trillion directly in equities at the end of the March 2024 quarter, a record $1.73 trillion in cash and deposits, and $3.88 trillion in superannuation, which was also an all-time high.

Growth in superannuation was driven by strong investment performance in both domestic and overseas share markets, a strong labour market and rising contributions from employers.

Total contributions increased by 11.3% to $177.0 billion in the year ending in March 2024; employer contributions increased by 12.4% to $133.3 billion while member contributions rose 8.2% over the year to $43.7 billion, data from APRA reveals.

Need to diversify asset base

With such a large proportion of individual wealth tied up in property, it makes sense for investors to diversify into other asset classes, to lessen the risk of their wealth falling should residential property prices pull back on higher interest rates or with any slowing in the economy or a rise in unemployment.

While lower rates helped to boost asset values after the COVID pandemic, higher interest rates could work to erode wealth in coming quarters should interest rates move higher this year.

With inflation remaining sticky, the RBA Governor, Michele Bullock recently said the RBA board did discuss increasing interest rates at its June meeting.

While the central bank didn't do so, it could raise rates again at its August meeting; that indicates a positive outlook for the returns on private credit, as most corporate loans are floating rate and can increase with changes in the official cash rate.

That is an important point. More defensive assets such as fixed income, and private credit particularly, may deliver more attractive yields than residential property, cash or fully-franked shares.

That's a key detail because it is income-yielding assets that will support Australians in everyday living and in retirement. Private credit can deliver investors yields up to 10% per annum, which is almost double typical yields on cash and up to four times the yields on rental properties which fall well below 5%.

In contrast, private credit offers an attractive level of regular stable cash income and return for investors, particularly in comparison to the long-run average returns of more volatile asset classes such as residential property and share markets.

That is one of the main reasons that Australia's largest institutional investors are allocating more to private credit assets.

AustralianSuper is one of the largest investors and has allocated over US$4.5 billion (A$7 billion) in private credit globally, with the stated ambition to triple its exposure in the coming years.

Get stories like this in our newsletters.