Will gold continue to shine in your portfolio?

One year ago, we discussed the forces driving the gold price to all-time highs.

Since then, the yellow metal has returned 33%, making it one of the best performing asset classes over the period.

And despite this impressive run, the structural case for gold remains well in truly intact.

A golden year not without its bumps

Gold reached US$3000 for the first time in history in March 2025 and has done well to largely hold above that level since. However, it was not all smooth sailing for the asset over the past year.

In November 2024, on the back of Donald Trump winning the US election, the gold price dropped 7% in response to the US dollar strengthening and bond yields increasing following the victory.

The stronger US dollar was an initial reaction to investors believing Trump's 'America First' pro-business agenda would benefit the US economy over other regions. This attracted investment in the US from abroad strengthening the dollar.

Bond yields increased as the market feared that higher budget deficits under Trump's proposed policies would put more pressure on an already very high debt level in the US.

As discussed in our previous insight, the US dollar and bond yields have historically been two of the key drivers of the gold price.

As the US dollar strengthens and/or bond yields increase, the gold price has historically tended to weaken as these assets are seen as alternatives to gold for investors.

More recently, following Trump's 'Liberation Day' tariff announcements, gold fell 5% in a single day.

The market reaction to Trump's 10% universal tariff and even higher reciprocal tariffs saw a sharp selloff in almost all securities as investors priced in this new regime.

Where does gold stand in the new US administration?

While both of these events could seemingly pose a risk to gold's run under the new US administration the reality may be very different.

Members of Trump's administration, including the president himself, have stated their desire for both a lower US dollar, to improve US export competitiveness, and lower bond yields, to better service the massive government debt and lower mortgage rates for individuals. If gold's historical relationships hold, these are both positive factors for the metal's desirability.

In fact, while the US dollar strengthened on the back on Trump's victory it has been weakening against its major trading partners through 2025 as investors come to the reality of the administration's policy priorities.

Similarly, bond yields peaked in January with investors turning their attention to the potential for a US growth slowdown as inflation continued to come under control.

Both of these moves lower also coincided with growing fears around the impact of Trump's tariff policies.

Tariffs, and how they are rolled out, could play a significant role in the returns for gold over the next few years.

Tariffs themselves, in the first instance, are likely to increase inflation and dampen economic growth. Both of these factors would be expected to increase gold attractiveness as a defensive, inflation hedging asset.

Further, the haphazard approach to the application of tariffs is also making gold more attractive as a portfolio diversifier.

There has been a lot of uncertainty around what tariffs will be in place, when they will take effect, how long they will stand for and ultimately what the Trump administration is using them for, be it a negotiating tactic, a revenue raiser, or a combination of both. This uncertainty lends itself to holding defensive assets like gold in portfolios.

Gold's structural drivers are still in place

As geopolitical tensions have escalated over the last few years central banks, in particular, have gone on a gold buying spree which has been the key driver of gold prices to all time highs - even before the latest episode around tariffs.

As a reliable store of value, gold is highly attractive for central banks seeking to diversify their reserves beyond foreign currencies like the US Dollar and US Treasuries.

In the wake of the Ukraine invasion, the US showed they were not afraid to 'weaponise' the dollar-centric global financial system by imposing crippling sanctions on other nation states. As the world's reserve currency, the US dollar gives the United States enormous leverage on the world stage.

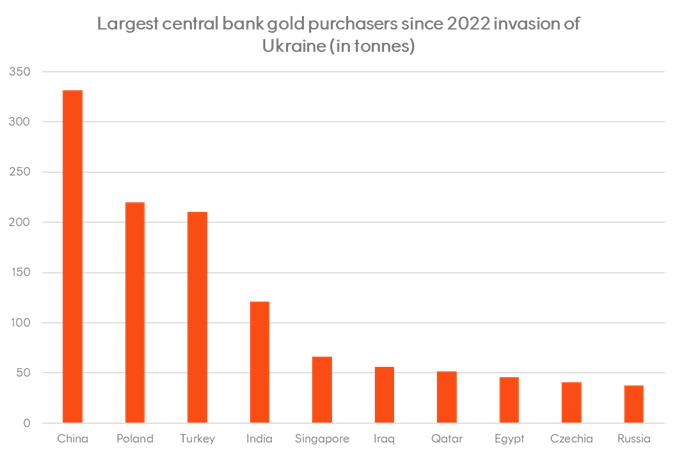

In response to this threat, the central banks of countries that wish to remain non-aligned or independent of the US have become huge buyers of gold in recent years. Since February 2022, total reported central bank buying has ramped up significantly thanks to emerging market and Eastern European countries like China, India, Poland, Turkey and Egypt.

Any dislocation caused by a trade war could further drive governments to increase their holdings in gold versus US-denominated assets. Goldman Sachs reported that central bank buying at the end of 2024 came in significantly higher than their expectations, particularly from China.

Investment implementation

In a period of escalating geopolitical tension and policy uncertainty, gold provides unique characteristics to diversify risk embedded in other asset classes.

As such, adding some exposure to the USD gold price in our Gold Bullion ETF (QAU) can improve diversification for traditional multi asset portfolios.

Get stories like this in our newsletters.