Aussies may need to take on more risk ahead of retirement

Many Australians close to retirement age won't have enough superannuation to live on during retirement and may need to invest more in higher risk assets such as shares to achieve their savings needs.

The sad reality is that many seniors simply don't have nearly enough in their nest egg.

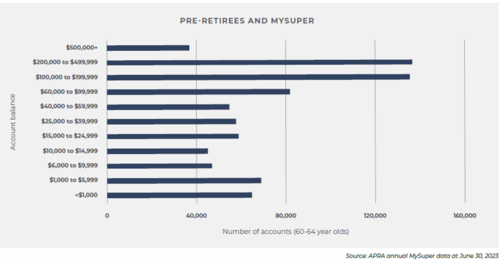

An analysis of APRA data by Innova Asset Management reveals that about 60% of MySuper accounts held by pre-retirees, or those aged between 60 to 64 years, had low savings balances below $100,000 - or around 800,000 accounts, as the chart below shows.

That is not sufficient to fund a comfortable 20 or 30 years in retirement, even with the Age Pension.

Gap between retirement savings and life expectancy

A 65-year-old Australian woman today can expect to live another 23.0 years and 65-year-old man another 20.3 years longer.

Taking the ASFA retirement standard, or savings required for retirement at age 67, a couple would need $690,000 while a single person would need $595,000 to live reasonably comfortably.

With around 800,000 accounts having a balance of less than $100,000, many older Australians risk being able to afford only a basic lifestyle and having to go without luxuries in what should be their most comfortable years.

This analysis suggests that a significant cohort of older Australians may need to seek financial advice during the critical years before retiring.

While the typical advice for a person aged 60 to 64 is to lower investment risk as their retirement approaches, which is something that lifecycle funds do automatically, lowering exposure to growth assets may not be a good strategy for many pre-retirees with low savings balances.

Those with lower balances may be better served by maintaining or allocating more aggressively to growth assets such as shares and investing less in cash and bonds, given their need for more wealth creation and better long-term returns.

Understanding of risk

Retirement planning involves complex calculations that require expert financial advice and an understanding of investment markets and risk.

The advice doesn't need to be all-encompassing financial advice. It can be limited to areas such as retirement and the better investment outcomes can potentially more than pay for the cost of financial advice.

Ironically, pre-retirees with substantial savings above $500,000 are more likely to seek advice and protect their retirement assets from the risk of a market downturn. It's those on lower balances who may be more in need of advice to build and protect their nest egg.

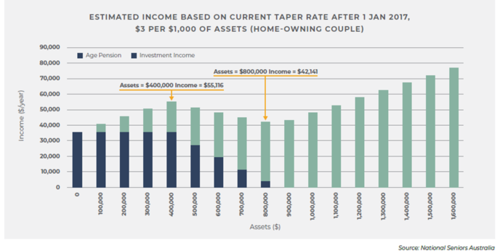

It's also important to note that the Age Pension isn't much help, given the 'taper trap,' or the outcome that as superannuation savings grow, the value of the Age Pension is cut by an even greater amount thanks to rules in Australia's retirement system, as the chart below shows.

In effect, the taper rate means that some individuals are getting less income even though they have more retirement savings. A financial adviser can help to manage this risk and to produce a higher level of superannuation savings overall, an essential goal for those with low balances.

Innova's analysis of the APRA data reveals that 46.4% of the near 1.7-million-member accounts held by 60- to 64-year-old Australians were invested in MySuper funds at June 30, 2023.

MySuper funds are intended as low-cost, simple products suitable for most investors.

Most are balanced funds, with a static 70:30 growth-defensive asset portfolio allocation. Yet as this analysis reveals, MySuper products are not the answer for many investors.

They were designed to cater for a largely disengaged customer base given superannuation's distant payoff.

Those least likely to be engaged - and invest in default MySuper products - include older people with lower education, on lower incomes and/or with lower financial literacy.

Building super earlier

Our research highlights the need for advice to build super savings much earlier in life and potentially in more aggressive investment products.

Nationwide, superannuation levels are growing.

Recently released ABS Household Wealth Data reveals that household net wealth sat at a record $15.66 trillion in the December 2023 quarter, with wealth boosted by a record level of superannuation assets, which totalled $3.74 trillion.

Total superannuation assets increased by 3.9% in the December quarter on rising Australian and international share markets and rising super contributions, driven by the strong labour market and legislative changes to raise compulsory superannuation levels.

So, as a nation, we have a very high level of superannuation savings but on an individual level, the level of savings is very unevenly split.

Get stories like this in our newsletters.