What's the outlook for gold amid the coronavirus crisis?

With investors having sold every sort of asset in March to raise cash, panic ruled over markets.

But gold and gold stocks could outperform the overall market this year if investors seek the precious metal as insurance against further financial market volatility, and as a hedge against inflation and the excessive debt held by central banks.

We remain optimistic about the outlook for gold and gold stocks in the near-term.

Gold companies continue to exhibit, we believe, truly compelling fundamentals and valuations.

Gold stocks generally remain in good shape and should be able to navigate a recovery, despite potential impacts to operations from the coronavirus pandemic in the near-term.

There are two main reasons why gold has been under pressure.

First, institutional investors have unwound hedged positions in risk parity and other volatility-strategy portfolios.

Second, other investors have sold gold to raise cash to meet margin calls to cover losses. This is commonplace during market sell-offs. Collateral and liquidity have been sought at all cost.

Lessons from history

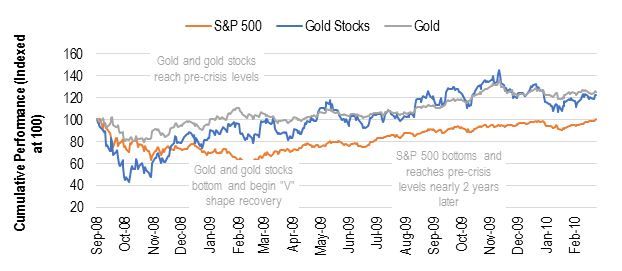

History has shown that stock markets eventually recover. And indeed, gold and gold stocks have tended to recover faster than the broader markets following crises, as seen in 2008 post-global financial crisis (GFC) and other previous market crises.

In 2007 our currency, buoyed by relatively high interest rates, bought as high as 0.9786 US dollars.

In the immediate aftermath of the GFC it finished 2009 at 0.8969. Prior to this current market-correction, at the start of the year the Australian dollar was buying 0.7003 US dollars and is now hovering near 0.6000.

During the GFC, gold and gold stocks bottomed and recovered much earlier than the US market benchmark, the S&P 500, recouping losses at around the time the S&P 500 reached its lows in February to March of 2009. You can see this below (prices are in US dollars).

The S&P 500 took nearly two years to reach its pre-crisis levels again. Gold stocks recovered a lot more quickly, as the chart below highlights.

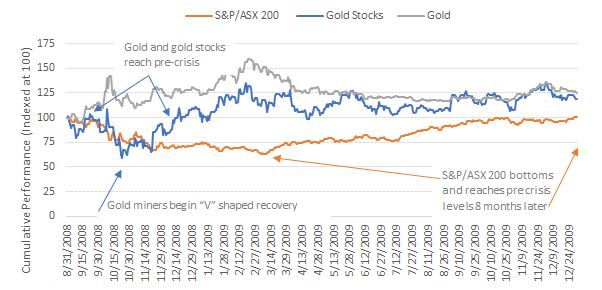

Looking at the Australian experience in 2008, our market recovered faster than the US. This is shown in Chart 2. Chart 2 is in Australian dollars and assumes all exposures to gold and gold stocks are unhedged.

You can see during the Australian share market recovery that gold bullion, in Australian dollar terms, held up particularly well and gold stocks tracked the experience of the US with a V-shaped recovery.

During this pandemic, gold miners are taking all precautions to continue running their businesses.

Although we anticipate that some operations will be impacted, discussions we have had with companies indicate that every effort is being made to ensure inventories, supply lines, employee health and back-up redundancies are in place to sustain production.

We expect limited to no credit problems in the gold mining sector.

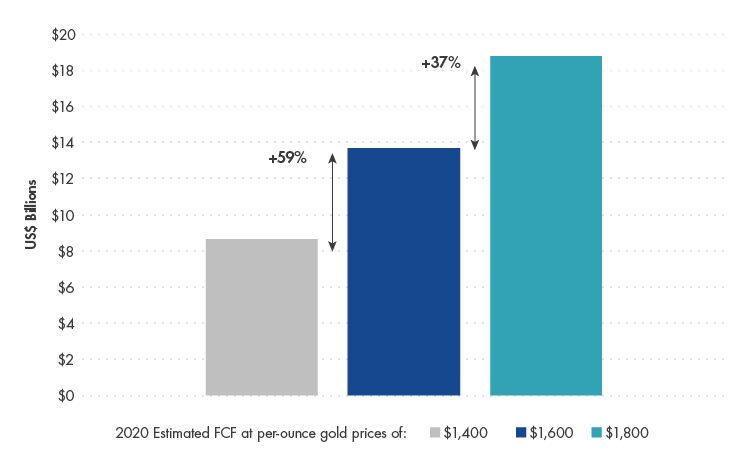

The lengths to which gold miners have gone to reduce costs and capital expenditures and to avoid mistakes of the past could translate to an additional near 40% increase in free cash flow, on average, if the gold price moves from US$1600 to US$1800 (for senior and mid-tier miners).

Exchange Traded Funds (ETFs) may provide access for investors looking to get exposure to gold bullion and gold miners in their portfolios as a source of defence and diversification.

The world's largest gold miners ETF, the VanEck Vectors Gold Miners ETF (GDX), is listed on the Australian Securities Exchange (ASX) and invests in a diversified blend of mid- and large-capitalisation companies involved in the gold mining industry worldwide.

GDX holds Australia's largest gold miner Newcrest and the world's largest miners Newmont and Barrick Gold.

GDX also holds Australian gold miners Northern Star, Saracen Mineral Holdings and AngloGold Ashanti, which have stood out amongst Australian gold miners on the ASX, with gains of 19.2%, 29.1% and 48.3% respectively over the year to March 31. GDX has gained 22.7%.

Across its whole portfolio, Canadian firms account for around half (53.7%) of GDX's holdings, while the United States (18.7%) and Australia (13.8%) round off the top three.

Get stories like this in our newsletters.