Major CBA change will allow homebuyers to borrow extra $50k

Homebuyers could now be eligible to borrow up to $50,000 more, thanks to a major lending rule change by Australia's largest bank.

The Commonwealth Bank of Australia (CBA) has quietly updated its credit policy to allow borrowers to count boarder income - money earned from renting out a spare room - towards their home loan application.

Mortgage broker George Samios, founder of Madd Loans, says the change could make all the difference for first home buyers trying to get a foothold in the market.

"This move will mean that many people can rent a room to a family member or friend and purchase a home, when before they may not have met eligibility criteria," Samios says.

And for others, "they will be able to borrow around $50,000 more due to the extra rental income, which can mean the difference between getting the home you want and missing out".

What's changed?

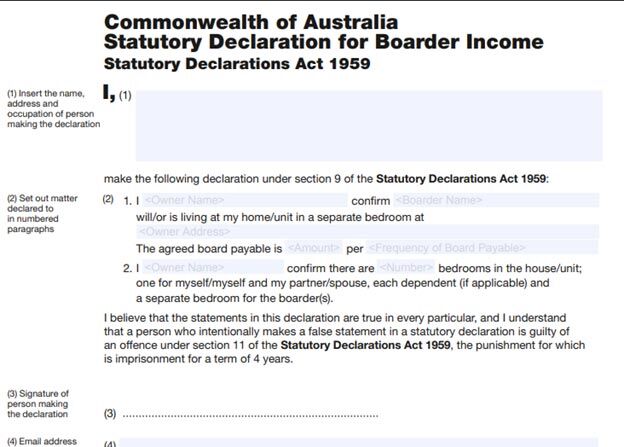

CBA confirmed to Money that under the revised policy, eligible borrowers can now include up to $150 per week in rental income, or $650 a month, when applying for a home loan.

The income must come from a boarder, defined by the bank as anyone who pays to live in the property, and the borrower must sign a statutory declaration, a legally binding document confirming the arrangement.

The policy applies to owner-occupied loans only, including first home purchases and refinances, and allows just one boarder per application. It excludes bridging and investor loans.

A CBA spokesperson says the update is expected to support a wide range of owner-occupiers.

"We are constantly reviewing and monitoring our home loan policies and processes to see how we can best meet our customers' home buying needs while maintaining our prudent lending standards," the spokesperson says.

How the new rule could work in real life

The update opens the door for borrowers who previously fell short on income requirements particularly those open to shared living arrangements.

For example, a single parent refinancing might declare that their adult child contributes $150 a week in board. With that income now counted, the parent could secure a better loan product than they otherwise would have qualified for.

A buyer working near a university could purchase a two-bedroom apartment and rent out the spare room to an international student, or to their mate or sibling.

But perhaps the group that benefits most from the change is first homebuyers.

The policy is open to customers with applications involving guarantor support, claiming first homeowners grants, or taking part in a Home Guarantee Scheme (HGS).

Samios says that in addition, many states will still provide stamp duty concessions. Queensland, for example, has allowed first homebuyers to rent out part of their property without jeopardising their eligibility for grants, provided they still live in the home.

"Think about this: in some cases, you now can pay zero stamp duty, access the first home buyer grant, and access up to $650 per month income towards your mortgage.

"And if you are building a new home there's no limit on purchase price."

What are other lenders doing?

While CBA is the first of the major banks to formally recognise boarder income, experts say it may not be the last.

"This is already generating a massive response," says Samios. "In a competitive market, this kind of move will force all banks to follow."

While CBA is the first major bank to formally recognise boarder income, many non-bank lenders already take a more flexible approach to income assessment-particularly for borrowers with non-traditional earnings.

Non-banks often have more relaxed lending criteria, which can benefit borrowers who rely on gig work, benefits, or irregular income. However, these lenders typically take on more risk, which can mean higher interest rates in return.

Get stories like this in our newsletters.