How to measure price and value when it comes to investing

Famed investor Warren Buffet once said "price is what you pay, value is what you get". But while understanding price is pretty straightforward, measuring value is more difficult.

Everyone has a different view on what represents value. Some people are more thrifty and therefore focused on achieving a lower price point. Others are happy to pay more if they believe they will get better quality - or, in the case of investors, better returns.

In some instances, value can be hard to quantify. For instance, an expensive bottle of wine may be seen as a waste of money by one person but good value by another - even if they have the same amount of money to spend.

But when it comes to investing, and particularly managed funds and their fees, it's different.

It can seem fairly straightforward to work out if an investor in one fund has obtained a greater return than an investor in a similar product with a different fee. You can also compare the price paid - provided the calculation is done after the funds' suggested investment timeframe.

However, to decide whether a fund presents good value or not, it's essential that the fees and what they apply to are properly understood - which is not always the case.

The main fee types

- Annual management fee - this is usually quite clear-cut and is easy to compare between two funds.

- Management expense ratio (MER) - this represents the management fee along with other fund expenses (e.g. audit costs). Again, it's usually straightforward to compare the MER of different funds.

- Performance fee - this can be more complex. It's often difficult to compare performance fees between funds as they rarely encompass the same information and can be structured differently.

To help with this, the indirect cost ratio (ICR) can be useful. It represents the overall cost of a fund, including the MER and any related performance fee, that has been paid during the financial year and then reported to ASIC.

However, the ICR is backwards looking. It is usually calculated after the end of the financial year, and looks solely at that past financial year. Investors should therefore understand that it doesn't tell you what you will pay for the year ahead.

In addition, investors need to take into account the performance of the fund during that 12 month period. The ICR may look high, but were returns strong? It would be a mistake to dismiss a fund from consideration simply because of a high ICR without also taking into account what the performance has been like - that is, making a comparison on price and not a comparison on the value that has been delivered.

Determining active versus passive value

In the current environment, focusing on value rather than price is likely to become more and more important.

During a downturn, investors tend to focus on protecting their wealth and minimising losses as much as they focus on achieving decent returns.

Many investors who have taken a "low-fee" approach to investing and gone into index funds in recent years - benefiting from the bull market of the past decade - may discover things are now very different. They are exposed to the whole market, without any levers to pull to adjust their position, regardless of any views they may hold on themes, sectors or individual stocks.

The "active versus passive" management debate has raged for a number of years, and is likely to continue for many more. For most investors, there is no simple answer and it may be the case that a combination of both approaches will serve them best, both in terms of price and value.

After all, the levers available to an active manager give them much more flexibility in adjusting their exposure to the stocks they hold (or don't hold) to take advantage of economic themes in the current environment.

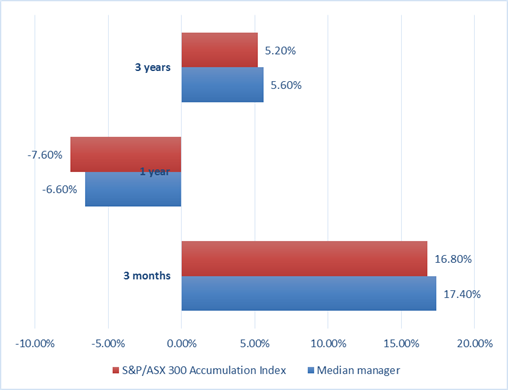

The benefit of this approach has been confirmed recently, with the latest Morningstar survey showing that fund managers have outperformed the index (on both the upside and the downside), including over the last three months when markets have been most volatile (see table below).

The important thing for investors is understanding the difference between active and passive investing, between the fees being paid and what those fees give them, and why and when the merits of one approach over the other can be most beneficial.

But in the end, the decision to invest either way should be made by considering more than just the cost.

Get stories like this in our newsletters.