The number that shows why property investors shouldn't panic right now

As with most assets, property has felt the effects of the COVID-19 pandemic. Values are dipping into the negative, migration has ground to a halt and at a certain point the banks will be forced to wind back mortgage relief.

All of these factors are headwinds, to be sure. But does that mean you should sell up and leave the market? There's certainly light at the end of this dark tunnel, but not without some hurt first.

S&P Global Ratings predicts national house prices will sink 10% before turning the corner in mid-2021.

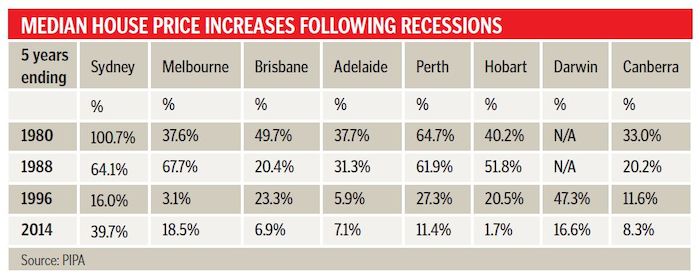

However, research by the Property Investment Professionals of Australia (PIPA) found that prices increased by as much as 100% in the five years after the most recent recessions (see table).

"In fact, looking back over the past nearly 50 years, house prices were higher five years after a recession or downturn each time," says PIPA chairman Peter Koulizos. "Some locations performed better than others, most likely due to local economic factors after each period.

"However, the research shows that talk of impending property doom has never happened in recent history - and these recessions or downturns lasted multiple years rather than a few months.

"The moral of the story is don't panic. Property has shown its resilience through economic shocks before and we have no reason to expect it won't do so again."

Still, this recession is like none other, so the nature of the post-crisis recovery is uncertain.

The first thing to do is take a step back and breathe. Panic doesn't lead to clear decision making.

"COVID is a prime example of emotions getting in the way," says Your Empire founder Chris Gray.

He warns against selling in a down market and crystallising a loss. "In the stockmarket I know people who sold out of their super, but every single economist I know would say don't sell if the market is falling," he says.

Gray also notes the costs involved in selling and buying property are there irrespective of the market level.

"If you add up what it costs to sell a property and buy another, at the end of the day it doesn't make any sense [in a falling market]," he says.

These costs can add up to tens of thousands, and include agent fees, marketing, conveyancing, possibly a mortgage break fee and capital gains tax.

"In a way, that's the advantage with property over other asset classes. Because it's so hard and expensive to sell and buy, it dissuades people from making rash decisions," he says.

It's equally important to put the current property pain in context. This means pulling out the pad and pen and working out the property's performance over an extended time horizon.

Sometimes poor growth doesn't reflect the quality of the investment. Returns could be concentrated over a short time.

"Property returns aren't necessarily linear, so it's possible that you could have the best investment property out there but not see growth for five years," says Stuart Wemyss, financial adviser and director at ProSolution Group. "Most people haven't worked out average percentage growth over a period of time."

It's about identifying what's driving returns, and whether these returns are dislocated from the market. "If you have, say, a property in Melbourne, which has overall appreciated 10% over 10 years, and my property hasn't, then I have a problem that needs to be identified," he says. "If your property has underperformed the market it's in, something has gone wrong."

Wemyss cautions against divesting unless you can point to the factors that have driven poor returns. "It could be location, orientation, changes in the area, land value underperformance," he says. "Nine times out of 10 it's easy to find the reason why. Unless you can pinpoint the problem, don't sell."

Gray agrees that poor performance needs to be historically contextualised. But this should go beyond the home value and cash flow alone to include the borrowing environment.

"It's misleading to talk only about rents or interest rates - it's the differential between the two that matters," says Gray.

He believes the current environment isn't as bad as it appears at face value. "If you go back to the year 2000, rent could've been $500 a week if the house was worth $500,000, so you'd have a classic 5% rental yield," he says.

"But rates were 7%-8%. So that means you were dropping 2%-3% gross. Today, rental yield is 2%-3% but interest rates are the same or lower. So now you have a net zero or net positive rental yield. So in terms of cash flow this is still one of the best times we've ever had."

In many cases, when you factor in interest rates you now have a net positive yield rather than a net negative yield.

It's also crucial to prepare for the worst. This means preparation before you invest in the first place. The risks posed by recessions specifically, and market falls generally, can be partially mitigated by careful property selection.

A good way to guard against unforeseen circumstances is to invest in properties that appeal to more than one market. For instance, a property that can serve as a share house for students and also a family home can provide protection against the loss of international students.

Another example is to avoid towns that rely on one industry, such as mining. As we've seen with the pandemic, recessions affect different sectors differently. And it's not just during a recession that sectors can fall on hard times.

"I bought in Blackwater, a mining town," recounts Lloyd Edge from Aus Property Professionals. "It had 23% growth at the time so I thought I was onto a winner, but then in 2012 the mining boom ended and rents and values dived. It reinforced the need to avoid buying in locations supported by a single industry."

Likewise, one can easily be distracted by shiny things. Sometimes if it seems too good to be true, it is.

"A lot of people see things like Airbnb, see a 10% rental yield, and think things will be rosy," says Gray. "But then it turns to winter or COVID and it all comes undone."

In this case, it's better to have steady, dependable rental yield rather than a potentially higher but volatile yield.

Any good plan starts with a strategy, which should be top-down, with individual properties defined by the overarching goals, rather than the other way around.

"Start with a strategy with a set of goals, and work backwards," says Edge. "Investing in cash flow properties serves a different goal to investing in properties with capital growth potential. Cash flow properties can look attractive in the short term, but without capital growth you're not going to increase your wealth."

Gray goes a step further. "No matter what the pain is, even if it's a few hundred thousand dollars, if the property is performing well in terms of capital growth, then weathering the pain is worthwhile."

However, Edge points out that finance will be easier to manage if your portfolio has properties with a healthy cash flow.

"You shouldn't just buy all your properties in, say, Sydney or Melbourne," he says. "It's better to balance the capital growth you get from the city centres with the cash flow found in regional centres."

But though it's a good idea to hold onto an investment property through the hard times, you shouldn't "set and forget". Successful property investing is a hands-on process, now more than ever.

Get stories like this in our newsletters.