Raiding super will not solve housing affordability crisis: ASFA

Allowing young Australians to tap into their superannuation to fund the purchase of a home would only benefit a minority of home buyers with higher super balances, new research has revealed.

The research, conducted by the Association of Superannuation Funds of Australia (ASFA), examined how far the combined super balances of first-home buying couples aged 25-35 would go towards meeting the deposit needed for median-priced homes in each capital city.

In many cases the research found that the funds a couple would be able to pull together from their super (if withdrawals were permitted) would fall well short of the money needed for a 20% deposit on a unit, let alone a house, though.

ASFA also noted that the increased purchasing power that some buyers would be able to access through their super would likely drive up property prices over time - leaving those with lower incomes and smaller super balances even less likely to be able to afford a home.

"Accessing superannuation is not the silver bullet to solving Australia's housing crisis," says Mary Delahunty, the chief executive of ASFA.

"While superannuation may seem like a tempting pot to raid, our analysis shows it will only benefit those young people who are already more likely to be able to afford a home, and not solve the crippling supply-side deficit that is fuelling our housing crisis."

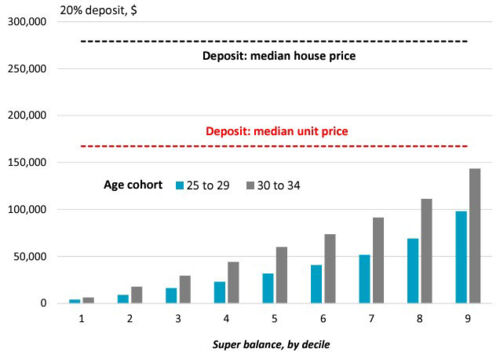

How far could a super-charged deposit go?

Though ASFA found sizeable differences in both the value of super balances for couples across the country, as well as the median price of houses and units in each city, younger Australians with lower super balances consistently fell short of the money needed to fund a deposit with their super alone.

That was particularly true in Sydney. With a median house value of around $1,4000,000 and a median unit value over $800,000, even the decile of young Sydneysiders with the highest super balances wouldn't have enough to fund a 20% deposit on a unit, according to the research.

Buyers in Melbourne wouldn't fare much better, as 30 to 34 year olds in the two highest deciles for superannuation balances would be the only ones able to use their super to pay for a deposit on the median $600,000 unit.

With relatively higher super balances on the one hand and a lower barrier to entry thanks to cheaper median prices on the other, buyers living in Perth would see their deposits go further than those in most other cities though.

Having said that, only those with the highest super balances for their age would have enough super to fully fund a deposit on a median-priced house in Perth, though a larger number would have enough to be able to fund the deposit on a unit.

Do early super withdrawals impact retirement income?

Even if younger Australians did have the opportunity to tap into their super in order to get into the property market, one of the big questions is: should they?

A report put out by The McKell Institute in late 2021 concluded that, when looking at the relative performance of the housing market and superannuation over the 30 years prior, people who dipped into their super were 'likely to end up financially worse off' over time.

Away from housing specifically, an analysis by Industry Super Australia on the Early Release of Super Scheme - which was introduced during the pandemic - found that a 30-year-old who withdrew $20,000 will end up being $80,000 worse off come retirement.

So could a super-for-housing scheme actually become a reality?

The federal Labor government has previously come out against the idea of people using superannuation for housing.

On the other side of the aisle though, the Liberal Party has a Super Home Buyer Scheme as part of its current policy platform which would allow first-time buyers to take out up to $50,000 towards the purchase of a home.

And just last week, Andrew Bragg, the shadow assistant minister for housing affordability, announced that a Senate Inquiry looking into Australia's Retirement System would be extended for 12 months in order to examine - among other issues - how super could be used to boost home ownership levels.

Get stories like this in our newsletters.