Should you buy, hold or sell Fisher & Paykel Healthcare?

Fisher & Paykel Healthcare (ASX: FPH) has consistently demonstrated an impressive growth trajectory, boasting double-digit sales growth over the past 15 years.

This success story began in the early 2000s with its humidification solution for hospital ventilators, which became a global leader.

Building on this foundation, Fisher & Paykel introduced its groundbreaking nasal high flow therapy, offering a more comfortable and effective alternative to traditional respiratory care methods.

This innovation has solidified the company's position as a leader in the respiratory segment.

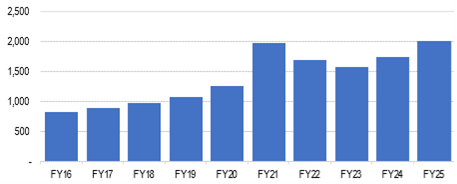

The COVID-19 pandemic, while challenging for many, provided a significant boost to Fisher & Paykel's revenues as demand for respiratory care products surged.

The company's ability to rapidly scale up its manufacturing in New Zealand, Tijuana, and Mexico, showcased its agility and operational excellence.

Post-pandemic, Fisher & Paykel has maintained its momentum, expanding its core respiratory range into anaesthesiology and delivering strong revenue growth from its home care division, thanks to innovative new sleep masks.

Fisher & Paykel - Revenues back to pandemic peak

Headquartered in Auckland, Fisher & Paykel has translated its robust sales growth into even stronger earnings growth.

The management team is optimistic about the future, aiming to double sales approximately every seven years, thanks to continued double-digit growth.

The intense 2024/25 flu season in the US and Europe, the most severe in over a decade, should bolster Fisher & Paykel's sales in FY25, potentially pushing them above the upper end of the projected $1.9-$2 billion range.

This, combined with the continued growth in utilisation of its respiratory range in hospitals, positions the company for a strong FY25 performance, potentially exceeding its revised net profit guidance of $320-370 million.

Looking to next year and beyond, Fisher & Paykel's earnings growth should be supported by a recovery in both gross and operating margins.

The company recently reported a gross margin of 62%, with expectations to return to pre-pandemic levels of over 65% within 2-3 years.

However, US President Donald Trump's planned 25% tariffs on Mexican imports are set to delay this recovery by a couple of years.

Yet the market has already factored in this tariff headwind, and any positive developments could lead to a sharp recovery in the share price noting the mercurial US President did exclude medical equipment from tariffs during his last term.

In conclusion, Fisher & Paykel Healthcare stands out as a resilient and innovative leader in the healthcare sector.

With a proven track record of growth, a strong pipeline of innovative products, and strategic global expansion, Fisher & Paykel is well-positioned for continued success. Buy.

Get stories like this in our newsletters.