Should you buy, hold or sell Macquarie Bank shares?

Founded in 1969, Macquarie Group has developed into one of Australia's best known diversified financial companies alongside the big four banks.

The group offers banking, investment and funds management and financial advisory services across multiple asset classes (equities, commodities infrastructure, fixed income) for individuals, businesses and institutions.

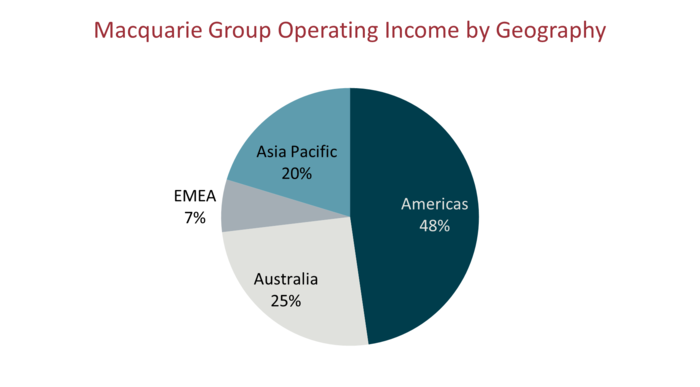

It makes its money from charging management and advisory fees and commissions for its services as well as making net interest and trading profits. Macquarie is a global institution. The below chart shows the group income from each region.

In all, 75% of operating income is sourced from outside of Australia, with offices in over 30 countries and employing more than 18,000 staff.

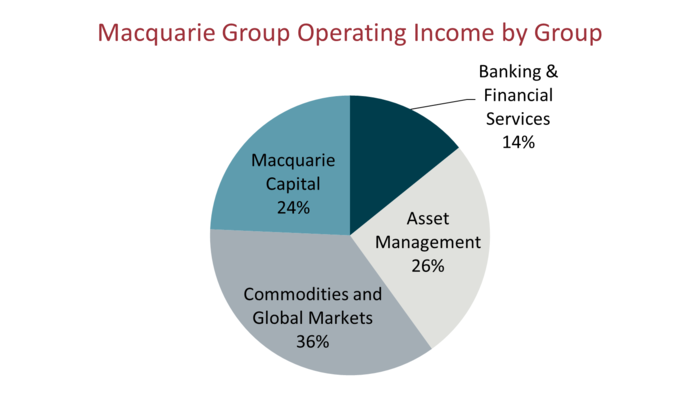

Macquarie splits its operations into four distinct groups. Given its diverse nature, competitors come in multiple forms including Australian retail banks, global investment banks, fund managers and international commodity traders such as Glencore and Cargill.

The Banking and Financial services division would be the group most recognised by readers, offering personal banking, home loans, business banking and wealth management services.

Macquarie Asset Management offers clients a range of capabilities in private markets and listed markets across numerous asset classes including infrastructure, real estate, equities and fixed income amongst others.

The commodities and global markets group offers financing, risk management market access and physical execution in commodities and other asset classes.

Macquarie Capital is an advisory and capital raising business for clients across a range of sectors. In addition, the group develops and invests in energy and infrastructure projects. The equities brokerage business also resides here.

The below chart shows the percentage of each group's contribution at an operating income level and highlights a diversified exposure across business segments.\

Recent result

Macquarie's business model has been well placed to benefit from the multiple tailwinds of a low interest rate environment and strong markets, high market activity and solid commodities pricing.

In its recently announced result Macquarie made a profit of A$4.7 billion in its 2022 financial year, up 56% from 2021, with the best performance coming from its market facing divisions (Macquarie Capital and Commodities and Global Markets).

Stock returns

Over the past 10 years Macquarie's shareholders have received an impressive annual return of 26% a year, when reinvesting the dividends, which compares to the ASX200 return of 11% a year. Capital returns (share price appreciation) have formed the bulk of this return.

The company's current dividend yield is just under 3.4% and this has been growing at over 4% a year. The dividend is 40% franked, which represents the fact that Macquarie earns most of its profit from outside of Australia. Macquarie pays out approximately 60% of its profit as a dividend and retains the rest to reinvest into the business.

ESG considerations

Macquarie scores highly on our ESG metrics and in particular the corporate governance rating which is crucial for a financial services firm. It has a clear focus on stakeholder engagement, including clients, staff and shareholders, evidenced in numerous client experience and employer awards.

Macquarie's environmental commitments aligned to net zero by 2050. It's worth noting that the company is enabling the energy transition through significant development of and investment in renewable energy projects.

Recommendation - HOLD

Our current analysis places Macquarie on a hold. We rate the stock highly on its growth metrics. Macquarie has built a strong franchise, robust business model and has an excellent track record of creating shareholder value, alongside a history of stable earnings and practical capital management.

Its diverse nature, both in terms of geography and operations allows Macquarie multiple opportunities to grow profits and it is uniquely positioned to be able to capitalise on structural changes such as increased global spending in infrastructure and the energy transition.

After a stellar year of high earnings growth and market outperformance in 2021, we view Macquarie as fairly valued notwithstanding that it has since corrected from its 2021 highs.

Key risks include the increasing interest rate environment and the possibility of stagflation in some parts of the world. Macquarie has benefitted from a low interest rate environment which has increased asset values and thus management fees for Macquarie. This effect now looks to be diminishing, at least in the short term.

Macquarie's guidance in the recent result was more cautious in its tone and any pullback in the market will see Macquarie's share price correct alongside this, as witnessed recently.

As equity markets adjust to a new interest rate environment there is scope for share prices to fall further and this could well provide an opportunity to buy shares in this high-quality business at an attractive price.

Get stories like this in our newsletters.