It's time to rethink your Big Four bank shares

The storm at Westpac over its alleged breach of anti-money laundering laws plus three of the big four banks cutting dividends or franking credits has left investors to reconsider their exposure to the big banks.

As profitability falls and negative headlines continue, more pressure will be put on dividends and share prices.

Even before AUSTRAC claimed Westpac did not comply with anti-money laundering laws 23 million times, the company shocked investors when it announced that it was cutting dividends for the first time since 2008, after its full-year 2019 cash profit fell 15% to $6.85 billion. The bank slashed its final dividend to 80 cents from 94 cents a share.

ANZ too recently cut the level of franking of its dividends to 70% from 100%, while NAB cut its final and interim dividends to 83 cents a share from 99 cents for 2019.

The big banks will find it difficult to maintain existing payouts to shareholders given the economic climate of historically low interest rates and lacklustre economic growth.

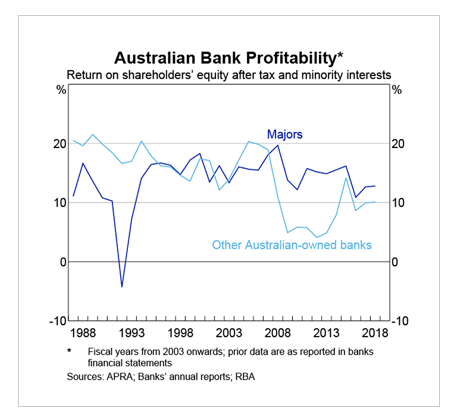

The graph below highlights that the big banks are much less profitable now than 10 years ago. Their return on equity to shareholders has fallen from around 20% in 2008 to close to 10% at current levels.

This is sounding alarm bells for investors looking for reliable income and capital growth. As the banks' profitability falls, the risk is that shareholders will see more dividend cuts and more capital losses on top of those they have already endured.

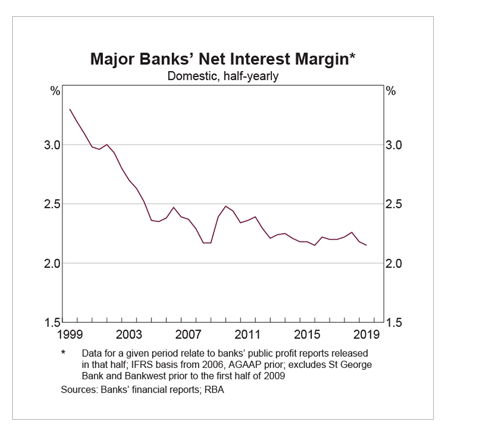

The chart below highlights that net interest margins (NIM) at the big banks have also dropped to their lowest level of around 2%, which is putting downward pressure on profits.

Falling NIMs and a rising regulatory spend in the aftermath of the banking royal commission are combining to reduce banks' profits.

The outlook for profitability is not good. Low interest rates are likely to persist for a long time in Australia and abroad. High levels of household debt in Australia will inevitably hamper future growth in earnings from mortgages and households saving more. Household debt sits at around 190% of household income, higher than in most other countries.

While most households are comfortably making their debt repayments now, any shocks to the economy such as a significant rise in unemployment could push some households over the edge.

Added to this are remediation costs for the banks associated with poor customer outcomes and regulatory non-compliance, which, according to Reserve Bank figures, have amounted to $7.5 billion across the financial sector over the past two years and are still rising.

That figure does not count Westpac's likely escalation in remediation costs, law suits and a potentially record-breaking fine following AUSTRAC's prosecution.

APRA has also imposed additional capital requirements on the major banks to account for poor risk management practices. All of these are weighing on the banks' ability to make money.

This is sobering news for shareholders. Dividend cuts and falling profits are alarming outcomes for the many Australian investors whose portfolios have significant exposure to the big four, which represent around one quarter of the S&P/ASX 200.

In other words, if you hold a blue-chip portfolio or are invested in an active or passively managed Australian equity fund that tracks or is benchmarked to the S&P/ASX 200, $1 out of every $4 is likely to be invested in banks and therefore vulnerable to the risks they face.

To reduce the concentration risk inherent in the Australian market, an investor may consider investing in VanEck Vectors Australian Equal Weight ETF (ASX: MVW), which recently surpassed $1 billion under management.

MVW equally weights the largest and most liquid stocks on the ASX at each rebalance. As at October 31, 2019, MVW's portfolio was 17.17% underweight the big banks compared to the S&P/ASX 200. This has led to a convincing outperformance of the ASX 200 over five years and since inception.

The time maybe ripe for Australian investors to act and lighten their bank concentration, a risk inherent in the S&P/ASX 200, and most Australian portfolios.

Get stories like this in our newsletters.