Why CSL might be undervalued right now

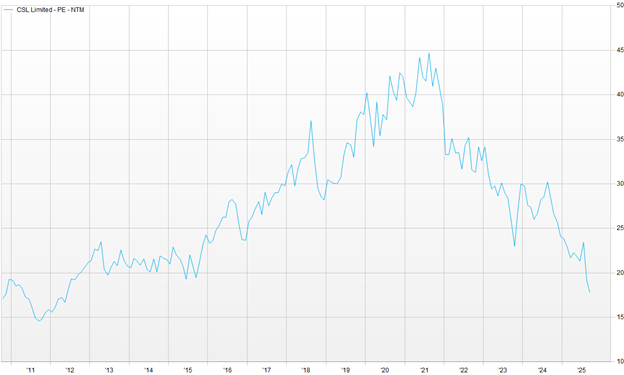

CSL, a great Australian success story, has captured the market's attention with its recent fall in price and an even more pronounced fall in its price-earnings multiple (P/E).

Its current P/E multiple is 17 times, the lowest in 13 years.

When you consider the stock has almost always traded at a premium to the market and is now trading at a discount, in the face of still-strong fundamentals, in our view, the stock currently offers an attractive entry point.

CSL, a growing business

CSL collects blood plasma, distills it, then manufactures it into products that treat immunological and other diseases.

With only a handful of competitors, CSL ranks highly in the therapeutic market in which it operates. Similarly, CSL has a vaccines manufacturing business and is a key player in the market for influenza vaccines.

CSL grew these core businesses through investment and a series of acquisitions bought at good prices from 2000 through to 2015. For the most part, this gave the company a cost advantage. With unmet need for CSL's products, the company grew faster than Australia's GDP.

More challenging times

The fall in CSL's P/E reflects concerns about a slowdown in vaccine appetite in the US and increased competition in the blood plasma business.

More recently, the company has shown some change in strategy, too, with a costly acquisition into an adjacent business and a rationalisation of research and development.

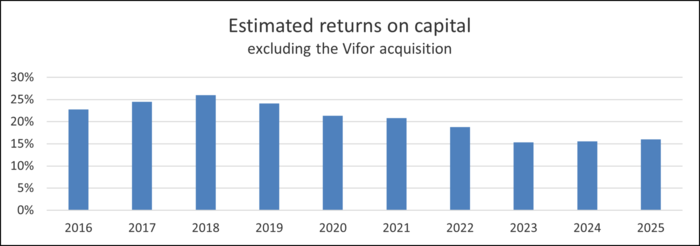

The company's returns on assets have fallen over time, largely reflecting the tougher market for securing plasma donations post-COVID-19.

Still a high-returning business

Our look at CSL's returns on capital suggests that at its core, the company's returns, while lower, are still at about 15%.

This is an enviable position that demonstrates the company's competitive advantages. And with scope to improve the cost of plasma collections, returns on capital are, we believe, likely to expand over time.

Not a discount stock

As previously mentioned, CSL is trading at a discount to the ASX200.

By trading at discount, CSL is viewed as riskier than the average stock in the market, or a slower-growing one, or both.

However, CSL still offers highly sought after medicines, retains strong positions in its markets and continues to be exposed to mid-to-high single digit end market growth.

The real opportunity is in total returns

As such, the real opportunity lies in total expected returns. Expected returns are a function of earnings yield, reinvestment return and growth.

We know earnings yield is already above the market; CSL also has high returns on investment, and its growth outpaces the market. Taken together, total returns, we believe, should then be above the market.

Get stories like this in our newsletters.