How to protect your investments during a pandemic

Health experts call it a pandemic, economists call it a recession flirting with a depression, and doomsday preppers call it vindication.

It can all seem rather hopeless.

But just as there are measures you can take to safeguard your health, there are things you can do to protect your wealth from the impact of the virus.

Battle stations

"The news on coronavirus and its economic flow on just seems to go from bad to worse and so its little wonder shares, commodity prices and bond yields have remained under pressure," says AMP chief economist Shane Oliver.

Governments are spending fiscally, while central banks cutting monetarily.

The Australian government has released a $17.6 billion stimulus package, while the Reserve Bank of Australia has cut rates to 0.5% and injected $8.8 billion into the market through short-term bank funding.

The US Federal Reserve is marching to a similar beat. It's cut its rate to near zero and will pump $700 billion worth of liquidity into the market through the purchase of bonds and mortgage-backed securities.

Unfortunately, while many of these measures mainly boost demand, they do little for the supply side-side problems we're seeing.

Australia's tourism and the education sectors are largely propped up by Chinese visitors and students respectively, so they've been hit hard by travel restrictions.

Other industries should be more resilient.

"Australia's trade - particularly in commodities like iron ore - will keep going to stoke the powerful Chinese industrial engine," says Tim Harcourt, host of The Airport Economist.

More broadly, Australia's economy "is resilient and it is well placed to deal with the effects of COVID-19," the Council of Financial Regulators said earlier this month.

"The banking system is well capitalised and is in a strong liquidity position. Substantial financial buffers are available to be drawn down if required to support the economy."

Safeguarding your investments

Now is a good time to review your portfolio, if you haven't already. High growth strategies, left unchanged during a crisis, can quickly turn into high loss realities.

Events such as coronavirus are referred to in finance as 'tail' events - they're unlikely, but always happen eventually.

Cue Coronavirus.

Tail events such as this one can smash investors approaching or in the early stages of retirement. In short, drawing down on your assets (as retirees typically do to help fund retirement) during a down market will have knock-on effects on the value of the investment. Worse still, retirees can feel like they need to sell out of their investment to 'avoid' further losses, but this essentially locks in the losses.

Upping the diversification and increasing exposure to defensive assets is always good hygiene against a market downturn. But it can only go so far.

"While these more defensive allocations will usually help defend capital during a tail event, in the more recent low-interest rate environment these allocations have also come with significantly diminished returns," says Alastair MacLeod from Wheelhouse Partners.

"Within equities, increased allocations to more defensive sectors such as utilities and consumer staples can also assist. However, there comes a point where correlations for all stocks and sectors increase, something we have witnessed in the past week or so."

There are further measures investors can take to safeguard their portfolios.

Some funds employ active tail risk measures - complex insurance mechanisms such as derivative overlays.

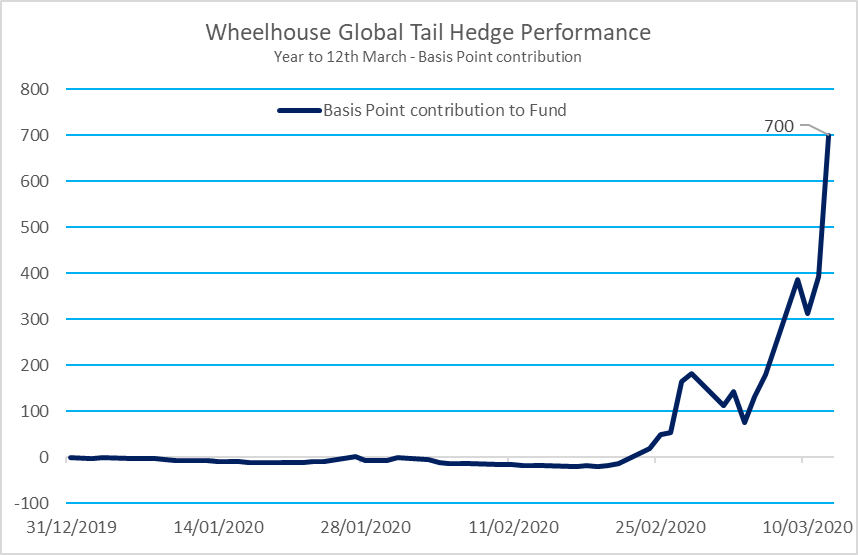

"Our tail protection strategy, once engaged, physically increases in value for every move down in the market," says MacLeod.

"In fact, the way our strategy is designed is that the hedge increases in value at a faster rate than the market is falling. This means that the worse the market falls, the more our hedge goes up."

The proof is in the pudding.

While the mechanisms described above cost the fund about 1-1.5% a year in performance (no free lunch in finance), they pay for themselves - and then some - when the market falls.

The graph below shows the 700 basis points the safeguards provided the fund in the year to March 12. It's easy to see the correlation with the spread of the coronavirus.

Beware of imitations

Sometimes so-called balanced portfolios can include high yielding defensive assets - such as bank hybrids, high yield debt, and listed property - that during a crisis can be anything but.

John Dyall, head of investment research at Rainmaker Group, points out that before the global financial crisis (GFC), listed property had a three year correlation with equities of 30%, but during and after the crisis that correlation rose as high as 80%.

Dyall says the only purely defensive asset class is government bonds.

"If you look back at the past 20 years of returns you will see that the average three-year correlation between Australian equities and the Bloomberg Ausbond Composite Index (which is dominated by government bonds) was -23%, with a high of 36% in 2015 and a low of -75% in 2013."

"And just to show that it is defensive, Australian equities had their lowest three-year return at the end of February 2009 with a return of -7%pa; the return from bonds over the same period was 9.5%pa."

Rebalancing super

Most super funds, and all MySuper funds, are diversified products with a number of asset classes. They're labelled according to their risk profile, such as growth, balanced, and moderate.

However, these labels can be vague at the best of time; sometimes they're redefined on the fly by fund managers in a thinly-veiled attempt to explain away poor performance.

Nor are these labels always a good reflection of what's under the hood. You could, for instance, have a balanced fund option made up mostly of growth assets.

"This ambiguity may seem absurd to many fund members but it happens because a super fund may invest into property because it delivers a capital growth return as well as a rental income return," says the director of research at Rainmaker Information, Alex Dunnin.

"As a result, how you split it between growth versus defensive income investing can be very subjective."

Still, re-balancing your super is straightforward - it can be easily done through the fund's online account portal or app.

But just because you can, doesn't mean you should.

"Investors should think through why they would want to do this," says Dunnin.

"For example, are they chasing higher returns, or are frightened they may be investing too much in high risk assets."

SMSFs

John Maroney, CEO of the SMSF Association, says the best bet for trustees is to engage a specialist SMSF adviser.

"The reality is investment markets do fluctuate wildly, especially when a global phenomenon such as the COVID-19 coronavirus hits, so having access to trusted advice is a prudent course of action for most trustees."

"It should set out why and how you've chosen to invest your retirement benefits in order to meet these goals. It is not a valid approach to merely specify investment ranges of zero to 100 per cent for each class of investment."

Get stories like this in our newsletters.