Will the First Home Super Saver scheme push up property prices?

Will the First Home Super Saver scheme push up prices? Ben Kingsley, chair of Property Investment Professionals of Australia and founding director of Empower Wealth

First-home buyers should welcome the federal government's new superannuation savings scheme, which will provide income tax reductions to help them save a deposit for their first home.

From July 1 this year, aspiring buyers can contribute up to $15,000 a year into their super accounts. The maximum for each first-home buyer will be set at $30,000, with the first withdrawals permitted from July 1, 2018.

But what will happen to house prices? Given the large focus on our two biggest markets - Sydney and Melbourne - some commentators will argue that this will add to the demand side of the ledger and push prices higher.

However, we see this as unlikely, especially when compared with previous governments' preference to splash out cash in the form of one-off grants, which many argued only found their way into vendors' pockets through higher property prices.

This initiative may not see a flood of buyers coming online at any one time, because each household is going to have to weigh up how much it is willing to put aside each year. And with a $15,000 cap each year and $30,000 cap overall, in some markets first-timers are going to need to save some funds outside this scheme if they want to pay a deposit of more than 10%.

So, yes, the new scheme will have some impact on demand, but I'd expect it will be a gradual increase as different individuals and couples start their savings journeys in different ways and with differing amounts over time.

I'm not expecting this will have any material effect on property prices in any one location. Locations with great lifestyle, infrastructure, amenity and conveniences will still attract high levels of buyer interest.

State governments will need to continue to do their bit in making sure more housing supply is made available to ensure prices stay within reach right across the country. First-home buyers might also still need to adjust their expectations when starting on their property journey.

I'm already salary sacrificing into super. Does that affect how much I can pay into the First Home Super Saver scheme? Dr Martin Fahy, CEO of ASFA

Individuals can contribute up to $15,000 a year to the first-home super saver scheme. The treasurer, Scott Morrison, says: "This one you just tick a form to say that in addition to your compulsory super deposit, you want 5%, 2% or 3% of your wage to go into this account."

If you salary sacrifice already, you will need to consider the new concessional contributions cap of $25,000 to determine how much you can further sacrifice. One potential benefit of this policy is that it will encourage young Australians to engage with their super earlier in life.

It would be important for the scheme not to involve any significant administrative burden on super funds because this would lead to higher costs for all fund members. In light of this, we will need to work with the government to address any administrative issues.

What should I do with the money if the equity released from downsizing is more than $300,000? Louise Biti, director of Aged Care Steps

Downsizing can help you move to more suitable accommodation as well as release equity to help fund living expenses, which may include much-needed cash flow to help pay for home-care services. So make sure you take into account aged care needs now and in the future when deciding what to do with the money.

Options include:

- Ordinary money annuity - to provide a regular and secure income stream to fund living expenses and home-care services.

- Low-risk (and low-returning) investments such as cash and term deposits for clients who favour security of capital.

- Australian shares to take advantage of the franking credits and capital growth to help deal with longevity risk and/or future aged care needs, subject to your risk tolerance and investment time horizon.

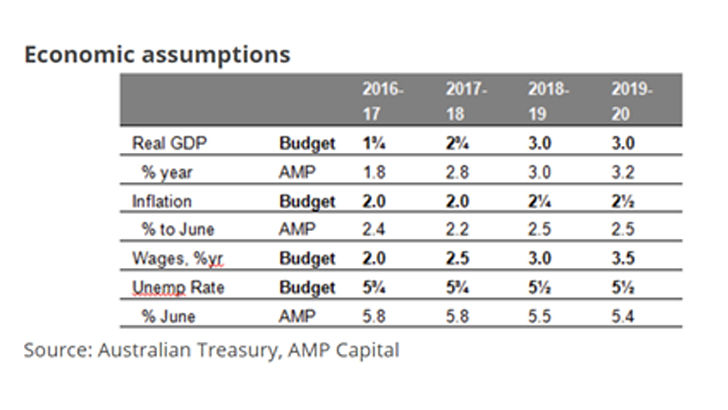

Is the projected wage growth of 3.75% in 2020-21 realistic? Dr Shane Oliver, chief economist and head of investment strategy for AMP Capital.

The major economic assumptions underpinning the Budget are shown in the table below.

Most of the assumptions look reasonable, except that the assumption that wages growth rises to 3.75% over the next four years looks too optimistic given unemployment is not expected to fall much.

The iron ore price is still expected to average $US55 a tonne over the next four years. This looks reasonable, albeit the recent volatility highlights the uncertainty around it.

Get stories like this in our newsletters.