Two cheap houses or one more valuable property: part two

Don't fear the gearBeing in debt does make you susceptible to rising interest rates and therefore greater overheads.

However it's a way of extending your reach. A classic truism with property or investing in general is "don't fear the gear".

If you want to get wealthy, getting over your fear of debt is probably your biggest hurdle.

The older generation always wanted to pay off their debts because paying interest was seen as bad debt, and they didn't feel totally financially secure until they'd paid off their home loan.

Concentrate on the big picture

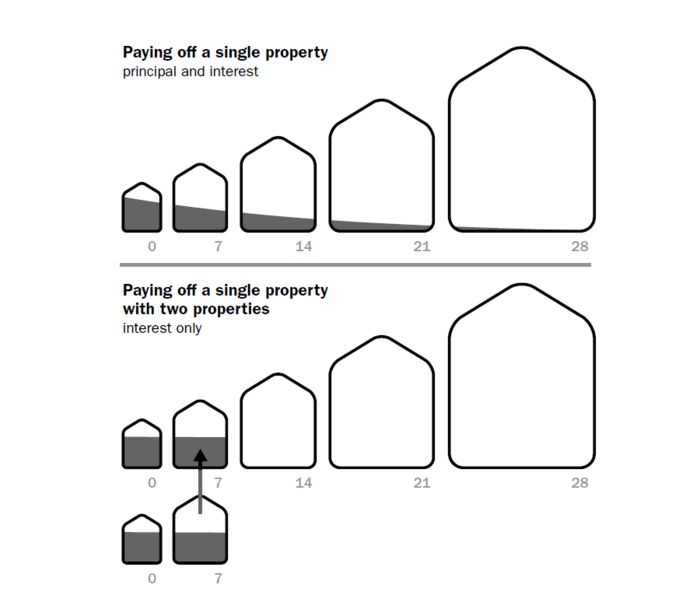

Under a normal principal and interest loan it takes most homeowners 25 to 30 years to pay off their mortgage, which is a long time.

If property values tend to double every seven to 10 years why not double your debt and buy two properties rather than one?

If you change both mortgages to interest-only your repayments will reduce and that will help pay any difference between the rent and mortgage interest on the second property.

If you lease out the second property you will have rental income to help pay the extra mortgage.

In seven to 10 years' time both properties should double in value but the mortgages will stay the same because you will have paid the interest.

You could then sell off the second property and use the profit to pay off your first mortgage leaving you debt free in seven to 10 years.

There would be capital gains tax to pay on the profit of the investment property so you may need an extra year or two of growth to cover it.

Nevertheless, you're still paying off your mortgage in a fraction of the time.

While being in debt can be seen as increasing your risk, this example shows that while it may be more risky in the first few years, once your equity has risen it can actually be less risky as your equity is rising and your debt is staying the same.

The numbers and why most people get them wrong

If buying two properties to pay off the first one is a good strategy - then why stop at one? Why not repeat the process? Why not buy three, four, five or six properties?

There's nothing wrong with borrowing if you're using the money to buy an appreciating asset.

So typically if you bought a $1m property, the downside is yes, it's going to cost you $20,000-$40,000 a year but if the asset is going to grow by $100,000 a year, you can treat the negative cash flow as the investment into your savings plan!

You've got to look at the big picture and rather than worry about paying more interest, if you're making money - who cares?

Each property I buy is going to cost me $2000-$4000 per month but at the end of an average year, I should be creaming $80,000-$120,000.

Fear of debt is the biggest thing to get over. If you're worrying about debt, walk through the numbers with an accountant who specialises in property investing.

As long as property continues to grow by at least 3-4%pa - if you can hold on, you will make money. So if you want to make a lot of money you shouldn't be worried about debt because banks, governments and every corporation use debt to grow their business.

Get stories like this in our newsletters.