'Coffee will cost more': the truth about the surcharge ban

On the corner of Sydney's Margaret and Clarence streets, Marius Beullens serves the CBD's morning brew from his coffee cart, Margot Espresso.

"Five bucks that'll be," he tells a bleary-eyed customer, tapping an order into the machine. The payment terminal flashes $5.08.

"What's with the extra eight cents?" the suit asks.

"It's just the card surcharge," Beullens replies. "Pay cash and it's five."

Those eight cents - a cost for using cards rather than cash - could soon disappear.

The Reserve Bank of Australia (RBA) wants to scrap merchant surcharges altogether, estimating shoppers would save $1.2 billion a year, or around $60 per card-using adult.

The central bank says small businesses would also be better off by $185 million annually, leading to a fairer and more competitive payments system.

But Beullens - and many small business owners like him - disagrees.

"The surcharge ends up being paid by someone," he says, "If I can't pass on those fees, I'll have to put prices up. That $5.08 coffee becomes $5.50. No one wins but the banks."

Why the RBA wants to remove surcharges

The RBA first allowed surcharges in 2003 so customers could see the true cost of different payment methods.

In theory, this encouraged cheaper options like cash or Eftpos and discouraged expensive ones like premium credit cards.

But in its July consultation paper, the RBA says surcharging is "no longer achieving its intended purpose".

With cash use plummeting, many businesses now apply the same flat surcharge to both debit and credit cards, making it hard for customers to avoid fees.

In October, the government cited similar concerns and announced it was "prepared to ban" debit card surcharging.

"Consumers shouldn't be punished for using cards or digital payments, and at the same time, small businesses shouldn't have to pay hefty fees just to get paid themselves," Treasurer Jim Chalmers said.

And it appears the ban has support from both major parties, with Liberal senator Dave Sharma penning an op-ed in the Australian Financial Review.

In the article published in July, Sharma called the proposed reforms a "considered way forward toward a more modern and competitive system that is more friendly to consumers and small businesses".

Since the RBA has limited authority to enforce a surcharge ban on businesses, bipartisan political support could be crucial if the central bank recommends government legislation to implement it.

The hidden fees when you pay by card

Small business groups agree with the need for greater transparency but argue the surcharge ban will simply hide (and not remove) the cost of card payments.

When you pay with a card, there are behind-the-scenes fees that get charged between banks and payment providers (like Visa or Mastercard).

These surcharge fees typically make up 1-1.5% of the purchase price.

The largest part of this amount is the interchange fee. This happens when the small business' bank processes the payment and your bank charges a fee for handling the transaction.

The interchange fee is currently capped at 0.5% for debit cards and 0.8% for credit cards.

Additionally, Visa and Mastercard take their cut called a scheme fee (around 0.1-0.2%).

However, they also add a bunch of other fees - cross border fees, network assessment fees, processing fees and foreign exchange fees.

Many of the fees involved in card payments are hidden from public view, but they ultimately flow from banks and payment providers to small businesses, and then to consumers through higher prices.

Why don't small businesses agree with the RBA's proposal?

Apart from the surcharge ban itself the RBA is proposing two key changes:

- Increase transparency around these hidden charges.

- Lower the cap on interchange fees.

While the Council of Small Business Organisations Australia (COSBOA) supports the lower interchange cap, it warns that removing the right to surcharge means small businesses will be forced to absorb the remaining costs or pass it onto the customer.

"The reality is that these fees will still be paid, just not disclosed," says Mathew Addison, chair of COSBOA. "That cost will be baked into the price of coffee, groceries, and services across the country."

Coffee cart owner Marius Beullens says he's unlikely to raise the price of a cup of coffee to exactly $5.08 and will instead opt for a rounder figure like $5.50.

"There will some of my customers that won't accept this price increase and go elsewhere; others may choose to forgo their morning coffee altogether," he says.

"Ultimately, it means I will have less customers and my customers will be paying more for the same cup. And it won't be just me."

Why small businesses pay more fees than Coles

Crucially, the interchange fee is far from equal. Big retailers like Coles and Woolworths pay as little as 0.1% in interchange, due to special deals with banks.

Under the RBA's proposal, small businesses will still pay more than three times that amount.

The Australian Lottery and Newsagents Association (ALNA) says removing surcharges without tackling this gap would wipe out up to 7% of profit margins on fixed-price products like lottery tickets.

"The RBA are protecting the status quo while small businesses, paying 300-400% higher card fees than large retailers, may effectively subsidise the low rates negotiated by giants like Coles and Woolworths," says ALNA CEO Ben Kearney.

As newsagency owner Mark Fletcher puts it, "the Reserve Bank is treating the symptom, not the disease: wanting to ban $1.2b in surcharges while allowing high merchant fees to continue."

"The RBA claim to eliminate the cost of surcharges on consumers is nonsense unless small business retailers are given payments costs that match the sweetheart deals given to big business," Fletcher wrote in his blog.

Payments giant Mastercard agrees consumers won't be better off, warning banks will claw back lost revenue by raising annual fees, introducing debit account charges, hiking credit card interest rates, and cutting rewards.

"We also think small businesses will put up prices by the amount of the costs they are going to wear," says Richard Wormald, Mastercard's Australasia division president.

"So, the net outcome will be no savings for consumers, who will be paying the surcharge today and the higher price tomorrow that is just built into the cost of goods."

What consumers can do

Unlike the banks or major retailers who can level out the cost, small business owners like Marius Beullens have less levers to pull.

He sells coffee and a ban on surcharges would mean he would have to increase the price of his product.

With margins tight, absorbing the cost is not an option.

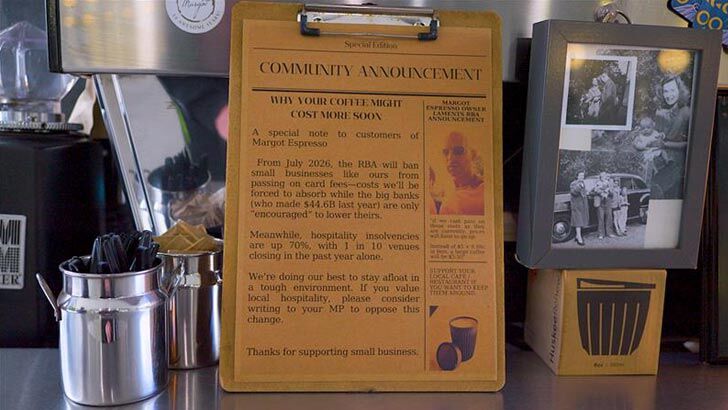

Hospitality insolvencies have surged 70% in the past year and Beullens worries about ending up like the one in ten venues that have shut up shop.

"We're doing our best to stay afloat in a tough environment," he says.

If you value local hospitality, please consider writing to your MP to oppose this change."

The RBA is taking feedback on the proposed policy options until August 26.

Get stories like this in our newsletters.