Is Monash IVF a buy, hold or sell?

Monash IVF Group (MVF) is the second largest provider of assisted reproductive services in Australia, offering the full suite of fertility and associated diagnostic services.

The company has a 50-plus-year history, dating back to 1971 when it was founded and 1973 when an MVF pioneer achieved the first in vitro fertilisation (IVF) pregnancy in the world.

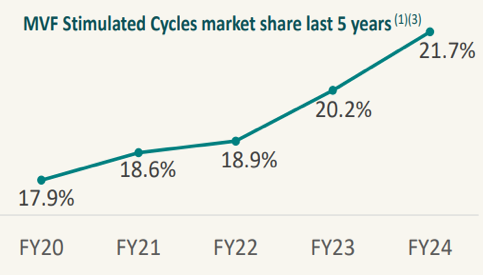

Over this time, the company has grown to occupy around 22% market share in Australia across 23 clinics and four service centres and has an emerging presence in south-east Asia with five clinics.

While the progressive increase in maternal birth age has been a structural tailwind for MVF's business over the past 20 years, the company's ability to improve pregnancy success rates to industry-leading levels (around 40.5% in 2024) has seen the company well placed to capture market share over this period.

More recently, demand from LGTBQIA+ patients and single parents, the addition of genetic testing and egg freezing have all added to MVF's growth story. While IVF is partly funded by the Medical Benefits Scheme, at 1.2% of total MBS funding, we view risks to funding cuts as relatively low.

Strategy

Consistently delivering market share growth through the cycle

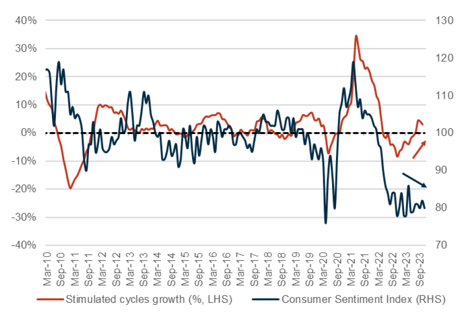

Demand for IVF has increasingly become less discretionary over time. In the chart below, we outline industry IVF growth relative to consumer sentiment.

While industry volumes have exhibited some cyclical characteristics in the past, the recent cycle has seen IVF demand hold up reasonably better than expected likely reflecting the time-critical nature and increased importance for those requiring IVF.

The company's ability to improve IVF success rates in addition to adding new facility experts through bolt-on mergers and acquisitions where it has minimal representation, has helped the company grow market share consistently irrespective of the cycle.

The company has recently expanded into day surgeries to enhance flexibility for doctors and patients.

Expanding into complimentary fertility services in Australia

MVF has successfully expanded into new growth verticals, adding egg freezing services and more recently genetic testing to the company's product offering.

In the egg freezing business, demographic tailwinds such as increased awareness, rising demand from the LGBTIQA+ population and new patient acquisition channels (sport and corporate) are all driving strong growth in medical and elective egg freezing.

Egg freezing now represents around 17% of MVF's stimulated cycles.

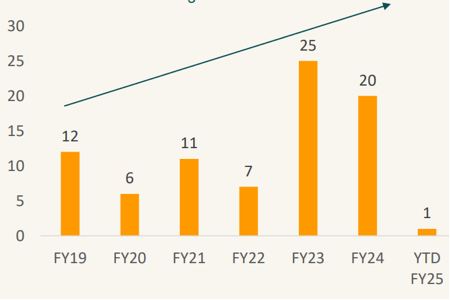

In the genetic testing business, the government recently committed $149 million of funding towards Medicare rebates for genetic testing from November 1, 2023. The most significant component of this package is a new $300-340 rebate for the reproductive carrier test (available for women who are pregnant or planning pregnancy).

This test (which screens for cystic fibrosis, spinal muscular atrophy and fragile X syndrome) is now bulk billed by providers. The introduction of this rebate has seen a strong uptake, with 60,000 three gene carrier screening tests taken in the eight months to June 2024.

Overseas expansion also on the agenda

Through MVF's ARS International arm, Monash has a fast-growing IVF business spanning markets in Malaysia, Singapore and Indonesia after recent success in turning around the business' fortunes. While growth is coming off a low base, the pace of growth should mean it will be a meaningful contributor in the medium term.

Outlook

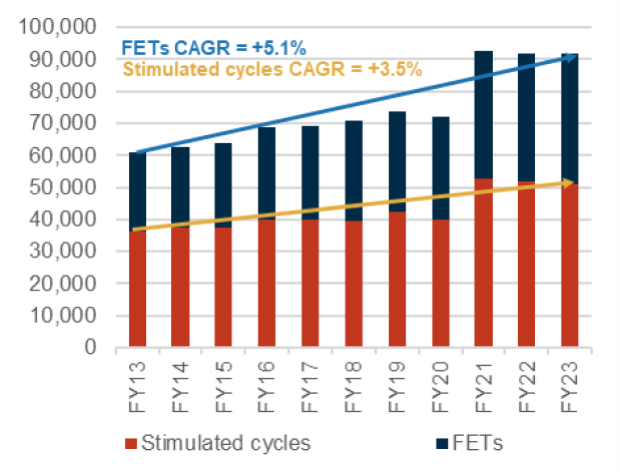

We anticipate MVF to be well-placed to capture the structural drivers of IVF growth going forward. IVF volumes and frozen embryo transfers (FETs) have delivered healthy CAGRs over the past decade and we anticipate this will continue.

The median age of Australian women giving birth has increased by around two years over the past 20 years (now at around 32). This has been driven by longer female workforce participation rates, increasing costs of living for families and improving contraception (amongst other trends).

Natural conception rates decline with age (lower number and quality of egg follicles) and the likelihood of needing ARS increases. MVF's average maternal age is currently 37.

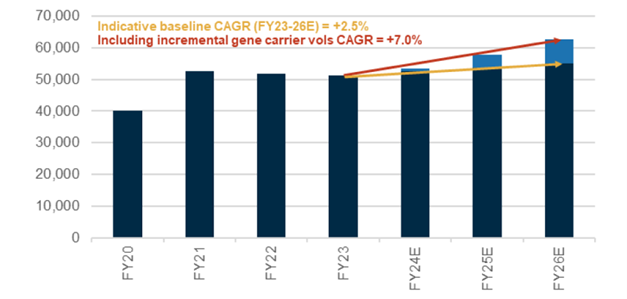

Meanwhile, we believe the outlook for newer drivers of demand are potentially underestimated and can meaningfully strengthen the earnings growth outlook for Monash. Making some reasonable assumptions around penetration rates in carrier screening for example, could yield outcomes such as those in the graph below.

Monash IVF returns

Monash IVF has a strong history of growing earnings, and while delivering an 8% compound annual growth rate (CAGR) over the past five years including dividends is respectable, this was diluted by a recapitalization of the company due to COVID-19 lockdowns.

The outlook for the business has multiple growth drivers and we anticipate upside to its previous return profile.

Recommendation

Monash IVF currently trades on a 12-month forward price-to-earnings multiple of 15x, 3% above its 10-year average.

It is forecast to yield a dividend of 5.5 cents per share for yield of 4.6% fully franked at current prices.

We anticipate the company can maintain a medium-term growth rate in the low double digits, which would likely see a re-rating of the shares higher. We can foresee a potential upside of around 26% in the not-too-distant future. Our recommendation is a 'buy'.

Get stories like this in our newsletters.