Niche firm bucks downward trend for travel agencies

Key statistics: Corporate Travel Management (ASX:CTD) Closing share price 23.11.16: $17.33 52-week high: $19.25 52-week low: $10.50 Most recent dividend: 15c Annual dividend yield: 1.42% Franking: 100%

The travel industry has undergone major disruption over the past 10 years as online offerings have driven down the margins available to travel agencies.

In this challenging environment, some firms have managed to innovate and thrive while others have suffered.

One firm that has found a niche and prospered is Corporate Travel Management (CTD).

As the name suggests, Corporate Travel Management focuses on the travel needs of the corporate sector with only a small leisure business.

It has built technology that is specifically tailored to business customers and makes it easy for travel managers to organise travel for their staff. It also has business units that are dedicated to the needs of the mining sector as well as events.

CTD is not an Australia-centric business.

Its revenue is well spread across North America, Asia and Europe as well as Australia and New Zealand.

North America is the largest segment at 30%. Australia and New Zealand account for 29% of CTD's revenue and CTD has managed to capture 12.5% market share.

In the larger markets of USA, Asia and Europe CTD's business accounts for 1% or less of the market, leaving a lot of scope to grow.

Profits have been growing at 26%pa over the past five years and are forecast to continue growing at 22% over the next three and 80% of this growth is organic growth, meaning that it is derived from the existing business.

The rest is from acquisitions. CTD has acquired 10 companies since listing in 2010, including two in North America.

CTD has a strong balance sheet with cash far exceeding debt. Return on equity (ROE) is the most effective way to measure a company's profitability and CTD's ROE is forecast to grow from 17% to 20% next year.

In a world where banks are paying 2% to 3% that is a very good return. Importantly, cash flow is also strong.

That means we can be confident that the profits are genuine and not accounting creations as they are translating into cash in the bank.

CTD is a genuine growth stock. The revenue and earnings are growing strongly.

The dividend yield is fairly low at 1.8%, allowing CTD to reinvest about half its profits back into the business in pursuit of that 20% ROE.

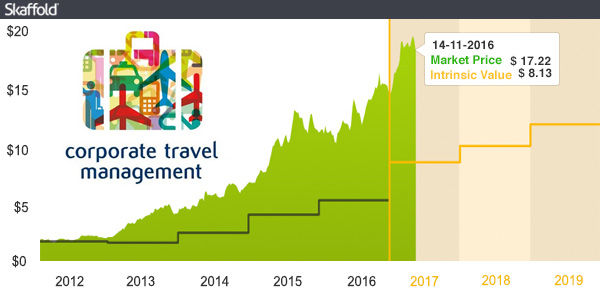

The forecast price to earnings ratio is high at 30 times, and right now the stock is trading at about twice the level of its estimated intrinsic value.

Everything is hinging on its growth prospects. Having listed for $1 in 2010 the rise to $17 has been spectacular.

For those investors with a strong appetite for risk there is clearly the potential for growth to continue.

Data accurate as at 21 November, 2016.

Chris Batchelor is a chartered financial analyst from Skaffold.

Get stories like this in our newsletters.