Reverse mortgages: lifeline for retirees or risky move?

Reverse mortgages may be the lifeline that cash-strapped retirees need during this global pandemic and beyond, but they should proceed with caution.

Sometimes referred to as "lifetime loans", reverse mortgages use the equity in your property as security for a loan. In contrast to regular loans, reverse mortgage interest is added to the loan principal and the whole lot is paid off when you sell your home or die.

The amount you can borrow is a function of your age and the value of your home. The loan to value ratio (LVR) starts at 15% at age 60 before increasing in roughly 1% increments every year. So if you're 80, you'll be able to borrow up to 35%.

If your accumulated interest and principal reach the value of your home, you won't get kicked out due to a forced sale, nor have debt continue accumulating. The negative equity protections legislated in 2012 prohibit both of those scenarios. And if the home is sold for less than the amount of the principal and interest owed, the bank will be left holding the bag.

With fixed-income assets paying out next to nothing these days, reverse mortgages may be a useful way to fund everyday living expenses.

They can be paid out in lump sums, flexible drawdowns or, for those with a dangerous spending appetite, regular instalments similar to an annuity.

"In my experience, reverse mortgages are for people who carry debt or day-to-day expenses," says Bob Budreika, director and reverse mortgage specialist at Smooth Retirement. "The typical market is people who don't have enough liquid capital and don't find their income stretching far enough."

But cash-strapped doesn't mean asset poor.

"Australian retirees own over $1 trillion in home equity, and we need to find ways to allow them to access that to fund their retirement," says Household Capital chief executive Josh Funder.

Retirees lean on the pension and superannuation, but the billions of dollars tied up in property sits idle when they need it most.

"Baby boomers and retirees are among the wealthiest in the world," says Funder. "They've been great investors and savers and most of the capital they've accumulated is in the home.

"[But] they don't feel wealthy because our system's focused on superannuation and the pension, and those are only two of the three pillars of retirement funding." [The third pillar is voluntary savings, including the home.]

With appropriate research, retirees can have their cake and eat it too - in their own home.

"We have to help Australia realise that the home is the best place to live and part of their retirement funding - it can be both those things during retirement," says Funder.

However, reverse mortgages come with significant risks that are often underappreciated.

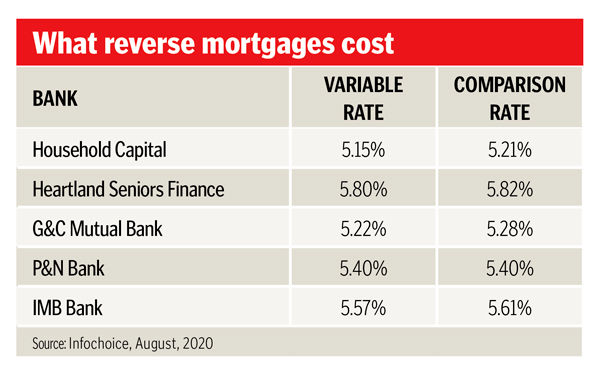

The main risk is that your loan principal increases as the interest payments are added to it (or compounded), and interest rates for reverse mortgages don't come cheap. At the time of writing, Household Capital had reverse mortgages with a variable rate of 5.15% and a comparison rate of 5.21%.

"If you borrow $50,000 on October 1, 2020 at a fixed interest rate of 5% per annum, your interest payment for the month of October will be about $208," says Tony Mitchell, from Stacks Law Firm.

"This means that on November 1, 2020 your loan principal will have increased to $50,208. Interest for the month of November will be calculated not on $50,000 but on $50,208. By the end of the 20 years, the principal will have grown to $135,632.01, comprising your initial loan principal $50,000 and compounded interest of $85,632.01."

Risk of family disputes

Eroded equity can also ignite estate disputes.

"Lawyers don't like giving advice on reverse mortgages because there's a degree of risk not just to the customers but also to their kids," says Mitchell. "There have been cases where lawyers have been sued by deceased estates: 'Mum and dad said we'd get the house, they'd never have signed up for this if they knew what they were doing, so we're going to sue the lawyers.' "

This is to say nothing about the costly red tape involved.

Lenders require customers to get the green light from accountants, financial advisers and lawyers. This takes considerable time and money.

Financial advisers, for instance, need to model possible scenarios that show what will happen to the client's equity over different timeframes, and this can set you back several thousand dollars.

Taking out a reverse mortgage can also impact your existing retirement income streams because the principle will be considered an asset (your primary residence is usually exempt from the assets test), which could reduce, or disqualify you from, the age pension.

"If a relationship breaks down or a partner dies, pensioners could find themselves needing an additional source of income because the asset limit on a single pensioner is much lower than a couple, and if they have $500,000 in super then the pension is gone," says Budreika.

The reverse mortgage may leave you with far less money to live out your life when it does come time to sell up. "If you have to sell your home some years after you have taken out a reverse mortgage loan and move into an aged care facility, your obligation to repay the reverse mortgage loan when you sell your home will reduce the amount you have available to contribute to an ongoing contribution for an aged care facility," says Mitchell.

Big banks pull out

There is also a lack of market competition among reverse mortgage providers. The industry has contracted significantly in recent years, which may partly explain why interest rates on these products are so high. The big four banks have left the market completely, leaving only Household Capital, Heartland Seniors Finance, G&C Mutual Bank, P&N Bank, and IMB Bank.

"Reverse mortgages are heavily regulated," says Mitchell. "One of the effects of that is to take players out of the market because the cost of compliance is so high. Reverse mortgages are very boutique products these days."

Nicole Pedersen-McKinnon, author of How to Get Mortgage Free Like Me, says there was a huge contraction in the market after the GFC. Banks became increasingly risk adverse, and the open-ended nature of reverse mortgages equates to risk they don't want to warehouse on their books, she says.

"They don't have a set date for repayment, so a lot of providers disappeared."

As with all financial decisions, learning about the risks and how they impact you is the best precaution against unwanted surprises down the road. Financial advisers, accountants and lawyers worth their salt should be across this, but it doesn't hurt to go through some obvious questions before you engage professional help.

Some things to consider:

- Calculate how much you may need for aged care.

- Is downsizing or selling down super a better option?

- Does the contract permit alterations to the home?

- What are the contract clauses?

- Do you want a fixed or variable rate?

- Are there residents in the home aside from your spouse who will be forced out by a sale if you die?

It's also worth considering what may happen to property prices. "If property prices drop, equity will be subsumed more quickly," says Pedersen-McKinnon.

The MoneySmart website has a useful reverse mortgage calculator that shows how much of your home you'll own after different loan durations based on factors such as age, home value, interest rate and fees.

The market for reverse mortgages is small and equity can be unknowingly eroded if you're not careful, but for those who are well informed these products could provide the key to the retirement you deserve.

Get stories like this in our newsletters.