What you need to know about lifetime annuities

A growing number of retirees face FORO-the fear of running out of savings in retirement. Lifetime annuities are touted as a potential solution, with 15 providers offering them in Australia and a government-backed option under consideration.

But despite their promise of a guaranteed income for life, awareness remains low. A UNSW study found that 57% of Australians have no knowledge of lifetime annuities.

Aaron Minney, head of retirement income research at Challenger, believes this knowledge gap needs closing.

"Many people don't know about the options available for generating retirement income. Australia has a world-class superannuation system, but the focus has traditionally been on saving and accumulating wealth," Minney says.

"The missing link is converting that nest egg into a reliable income stream, giving retirees the confidence that their money will last a lifetime."

However, annuities aren't without risks. Here, we explore their benefits, drawbacks, and whether they're a good fit for retirees.

What are lifetime annuities?

Minney describes lifetime annuities as an "insurance product for your retirement", offering retirees income for as long as they live, no matter how long that might be.

To purchase a lifetime annuity, retirees make a one-time upfront payment. The minimum required varies by provider, with some products, such as Allianz Retire+ AGILE, starting at $20,000. Once purchased, retirees receive regular income payments for life, which can be made monthly or annually, depending on their preferences.

The funds used to purchase the annuity are pooled with contributions from other investors, creating a shared fund that supports the income stream. Retirees can buy an annuity using their superannuation (if they meet access requirements) or their personal savings.

How are lifetime annuities regulated?

The promise of guaranteed income is only as strong as the company offering it, which is why lifetime annuities are subject to strict regulation by the Australian Prudential Regulation Authority (APRA).

APRA ensures that providers maintain sufficient capital to meet their obligations to retirees, even during extreme market events. Companies must hold enough reserves to withstand financial shocks expected to occur once every 200 years.

Unlike superannuation funds, which can be affected by stock market downturns, lifetime annuities are monitored closely to help protect retirees' income.

The pros and cons of lifetime annuities

This heavy regulation has its pros and cons. Ryan Watson, founder of Melbourne-based financial planning company Tribeca Financial, says these guaranteed income streams bring certainty and predictability.

However, lifetime annuities also have their drawbacks. Watson says the income returns that the investor receives via an income stream are quite conservative.

"This, in turn, can limit an investor's potential lifestyle options, as they have limited income to support their lifestyle, due to having no upside investment opportunity."

What happens if you die early?

A common concern among retirees considering annuities is the fear of losing their investment if they pass away shortly after purchasing the product. Some providers now address this by offering additional benefits or withdrawal options.

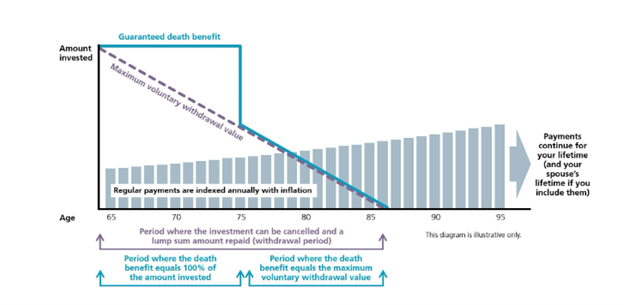

For instance, Challenger's Liquid Lifetime annuity offers a death benefit period based on the retiree's life expectancy. For a 65-year-old male, the death benefit period is nine years, while for females, it is 11 years.

The product also allows investors to withdraw their funds during an initial period if their circumstances change, shown in the image below.

Challenger's Liquid Lifetime option, along with other products such as Generation Life's LifeIncome, allows the income stream to be transferred directly to beneficiaries, providing loved ones with continued financial support.

Addressing inflation and market returns

One challenge with lifetime annuities is their potential to lose purchasing power over time due to inflation. While locking in a fixed income provides security, it can lead to reduced buying power if prices rise significantly.

To address this, some products offer inflation-linked options. Challenger's CPI-linked annuities adjust payments in line with inflation, and even peg the returns to the RBA cash rate.

Others, such as Allianz Retire+ AGILE, offer a two-phase structure.

"Your money keeps earning market-linked returns in the growth phase, and when you decide to transfer into the lifetime income phase you receive a fixed or rising guaranteed income for life," says Adrian Stewart, chief executive of Allianz Retire+.

Generation Life's LifeIncome product even frontloads the payments so retirees can enjoy more income in their earlier years of retirement.

What are government-backed annuities?

While the private market has a growing number of options, the Grattan Institute in January proposed a plan for the government to enter the annuities space.

The Melbourne-based think tank recommended that retirees should place 80% of their super balances above $250,000 into lifetime annuities.

Grattan argues that, like many other countries, the role in administering this should be taken on by the federal government in conjunction with an independent agency.

While Challenger agrees with the Grattan report highlighting the benefit of investing some of your retirement savings into a lifetime annuity, Minney believes the compulsory 80% allocation is too high.

"The majority of Australians can enjoy most annuity benefits with a capital allocation of just 20-30%," Minney says.

"In recent years, we have seen increased interest from the private market in managing annuities. With this in mind, we believe Grattan's call for Government involvement to drive annuity take-up is incorrect."

Will a lifetime annuity stop me from leaving an inheritance?

The retirement strategy to allocate only a portion of retirement savings also dispels the assumption that annuities prevent retirees from leaving an inheritance.

"This myth results from the assumption that all savings must be used to buy the annuity," says Minney from Challenger.

"When a retiree allocates a part of their retirement savings to a lifetime annuity, their estate balance is often higher. This is because of the regular income the annuity provides, meaning there is no need to draw down from savings."

Is a lifetime annuity right for you?

Watson says that lifetime annuities are best suited for retirees with a conservative risk profile. "They want certainty around their investment, want to take out any investment risk, and want a guaranteed income stream," he says.

However, making the right decision requires careful planning. Retirement strategies should take into account each individual's goals, risk tolerance, and income needs.

Minney and Watson both recommend that retirees consult with a financial adviser to assess whether a lifetime annuity aligns with their broader retirement plan and how it could work with their superannuation, savings, and pension.

Get stories like this in our newsletters.