Why ASIC is suddenly ramping up its investigations

The country's largest superannuation fund, AustralianSuper, found itself in the headlines for all the wrong reasons in February this year.

The Federal Court ruled that the super giant had breached one of its fundamental duties by failing to merge multiple accounts held by more than 90,000 members between July 2013 and March 2023 - a failure that cost members millions of dollars in fees and lost returns.

As a result, AustralianSuper was ordered to pay a $27 million fine in addition to providing remediation to the members who were affected.

This is just one example of the many cases taken on by the Australian Securities and Investments Commission (ASIC) every year. After all, the regulator filed the initial civil proceedings against AustralianSuper in 2023.

Why is ASIC taking on more investigations?

In the 2024-25 financial year alone, the regulator commenced more than 250 new investigations. This was a notable jump from 168 the year before, and it was no accident.

ASIC chair Joe Longo says that the increase in investigations is a direct result of the reform agenda the regulator has embarked on in recent years - reform that has seen the organisation restructured and its executive refreshed, and that has ushered in a greater embrace of technology.

"A whole lot of changes have been made, but what's really driving them is my desire to ensure that ASIC acts as a whole of agency," says Longo.

"So what we're doing is being cleverer and more sophisticated about bringing together all the data we've got and working more effectively internally to identify matters that ought to get quicker attention."

Part of the new approach is ensuring that the regulator is more scrupulous about how it uses its resources in going after big and small fish.

"One of the issues ASIC faces is that a lot of our cases are big and ugly," says Longo. "We don't shy away from those, but you can only run so many big cases before they take resources from everything else, so what we try to do is be very strategic in what we choose to litigate and investigate.

"So what you're seeing, which I'm proud of, is a diversity of cases where we're taking on the big end of town that might lead to trials that go for months and months and take a long time to prepare for.

"But there will also be a whole range of smaller matters across every aspect of our work that we can bring on more quickly and that have a lot of impact."

What is ASIC's role?

Stepping back, it's fair to say that, for some Australians, ASIC will just be another, vaguely familiar name in the jumble of regulator acronyms that also includes APRA, ACCC and AUSTRAC.

They may even be familiar with some of ASIC's work, but not entirely across its scope as a regulator.

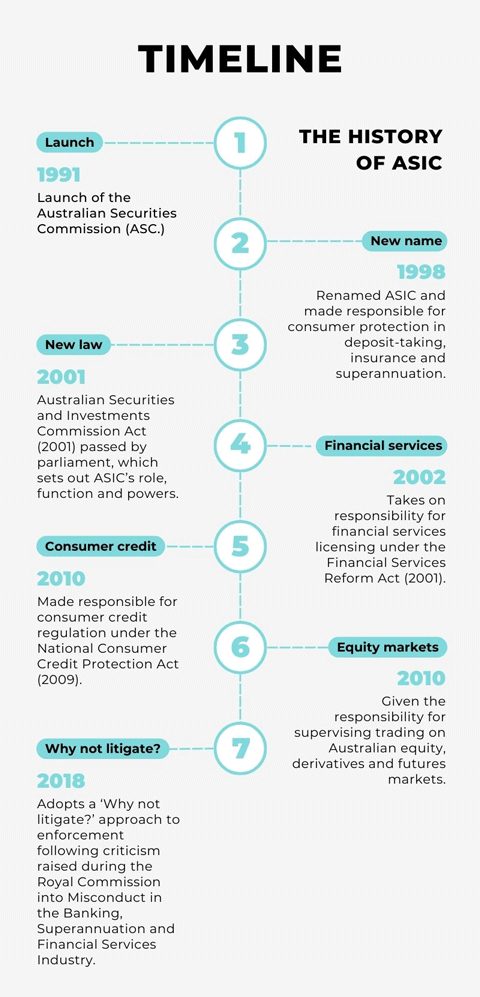

It all started in 1991 with the launch of the Australian Securities Commission (ASC), and in 1998 ASIC took on its current name after it was made responsible for consumer protection in the deposit-taking, insurance and superannuation sectors.

Fast forward to the present day and ASIC has more than 1600 employees based in offices in each State and Territory. At its core, ASIC is the national corporate, markets, financial services and consumer credit regulator.

That means that it is responsible for maintaining the integrity and trust of the financial system and the entities that operate within it by taking action to ensure that the relevant laws are upheld.

To put that responsibility into perspective, ASIC oversees the country's superannuation funds, exchanges (such as the ASX and Cboe), plus more than 6000 financial services licences and 4500 credit licensees.

ASIC isn't just in the business of launching civil or criminal proceedings against organisations and individuals who have done the wrong thing.

The organisation issues financial services and credit licences. It maintains registers. It produces reports and discussion papers. It facilitates broader conversations about relevant topics (for example, its recent work related to public and private markets).

It also acts as an educator. ASIC's Moneysmart website, for instance, is designed to provide tools and guides to help Australians navigate the world of consumer finance and to improve their financial literacy.

How is ASIC funded?

It's important to note that ASIC is an independent body whose commissioners are appointed by the Governor-General rather than by parliament. However, the regulator does get its funding from the Federal government.

For the 2024-25 financial year, $592 million worth of funding was made available to ASIC to cover its day-to-day and regulatory costs. However, it recovers a significant portion of those regulatory costs through fees and levies via an industry funding model. For the 2024-25 financial year, ASIC estimates that it will recover more than $400 million.

What about the penalties paid by companies that ASIC has launched civil proceedings against?

For example, the $27 million fine handed down to AustralianSuper by the Federal Court.

These fines don't end up in the regulator's coffers. Instead, the money is directed back into the Official Public Account which is, essentially, the Federal government's main bank account held by the Reserve Bank of Australia.

How ASIC decides what to investigate?

With such an extensive purview, the regulator is forced to be selective about its priorities. In saying that, the areas of focus set out in its 2024-28 corporate plan cover a lot of ground.

Among the target areas that may be of more interest to consumers, ASIC says that it will be focusing on financial hardship assistance, insurance-claims handling, greenwashing, services for super fund members as well as scams, misconduct and the poor use of artificial intelligence.

"We can't solve every problem. We can't take on every theme. So I think the reasonable expectation of ASIC is that we take on significant problems that are going to help the most people," says Longo.

Identifying problems in the financial space and locking on to specific issues is not only a continuously evolving process, Longo says - it's also a collaborative one.

"We have a number of external panels that help us. One is the Consumer Advisory Panel, which meets three or four times a year and is made up of a very senior, diverse group of consumer advocates and stakeholders.

"And all of my commissioners are constantly engaging with stakeholders. What I say to all of them is that I want you to spend at least 50% of your time talking to people and listening to what's going on.

"Another source of feedback is reports of misconduct. We get more than 10,000 of those a year and we also get data from the Australian Financial Complaints Authority and a whole range of schemes."

From there, Longo says that all that intelligence and data is synthesised and absorbed in-house and used to form ASIC's priorities.

"But we don't stop there. We're very open as a regulator. When we talk to panels and the media and stakeholders, we tell them what we're thinking, what our priorities are and why we think they're our priorities.

"And so one of the reasons I'm pretty confident we've got the right priorities and we're looking at the right problems is because people are giving us

that feedback."

What powers does ASIC have?

High-profile cases that result in large penalties - like that involving AustralianSuper earlier this year or the $15 million penalty ANZ received in 2023 for misleading credit card customers - grab the headlines.

But not every action taken by ASIC is a civil proceeding. The regulator can - and often does - seek criminal prosecutions against individuals who have broken the law.

ASIC can also disqualify company directors and cancel or suspend the financial services or credit licences held by firms. It can even hand down temporary or permanent bans to some people working in the financial services space.

In one recent case, ASIC issued a permanent ban to a financial adviser who operated an advice firm in NSW, Queensland and Victoria.

The regulator determined that the advisor had misused client funds and concealed information from clients, among a litany of other infractions.

ASIC can also choose to issue warnings to participants in the financial services sector who may not be doing the right thing.

As a part of an international crackdown on financial influencers (often known as finfluencers) conducted by ASIC and regulators from Canada, Italy, Hong Kong, the United Arab Emirates and the UK in June, 18 finfluencers received warning notices from ASIC.

The regulator noted that the finfluencers were suspected of having unlawfully promoted high-risk financial products

and provided unlicensed financial advice to Australians on social media.

Why was ASIC under fire?

Like any regulator, ASIC doesn't always get its way. While there's no shortage of cases it has successfully argued in court, plenty of others have been unsuccessful.

Some argue that the regulator also doesn't always get things right.

Or that it has - at times - fallen short of expectations.

The most obvious example of widespread criticism directed at ASIC came amid the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which ran from 2017 to 2019.

During and after the commission, ASIC received backlash for its perceived failure in preventing some of the misconduct that was found to have taken place.

The regulator copped flack for being too slow to act, for being overly co-operative with some of the institutions involved and for taking an approach that too often favoured settlement over litigation.

Since taking over the reins as chair of the regulator in 2021, Longo believes that the reforms undertaken throughout the organisation have already started to bear fruit.

Longo has a list of successes and examples which, he says, demonstrate the ways that ASIC is making the financial landscape fairer and safer for everyday Australians.

Among those, he says that he's pleased with the way the regulator has approached enforcement and regulatory initiatives.

"When I step back, I like the fact that we're doing strong enforcement and what I would call strong regulatory impact initiatives that affect all Australians. And one supports the other. That's how we bring about change.

"I think one is the cumulative effect of the strategic litigation we've been running over the past couple of years.

"I'm proud that our investigation and litigation activity has become a lot more focused, strategic, timely and impactful."

Then there's the regulatory work that ASIC has been doing - work that Longo says doesn't get talked about as much as its investigations.

"We have a strong enforcement capability, but look at our work in the regulatory space. There's a whole range of reports and activities arising from our surveillance that are having direct impacts on consumers.

"I'll never forget when we launched the financial hardship report last year because I was really struck by the positive reaction of the consumer groups - they were so pleased that we called out the problem.

"We'd done all this work and we said to the banks, 'You've got to do something about this'. And it had a real impact. I had banks calling me saying, 'Okay, we get it, we're going to do something'.

"So that wasn't litigation, that was a really strategic, data-driven report that had a lot of impact.

"I think you'll see ASIC doing more and more of that."

Notable ASIC-driven cases

Active Super

In March 2025, the Federal Court imposed a $10.5 million fine on Active Super after finding that the fund had presented misleading claims related to the ethical nature of part of its investments.

ANZ

In September 2023, the Federal Court ordered ANZ to pay a $15 million fine after the bank admitted that it had misled some credit card customers about the funds available in certain accounts.

AustralianSuper

In February 2025, the Federal Court ruled that the trustee of AustralianSuper should pay a $27 million fine after finding that the fund had failed to merge multiple accounts held by 90,700 members.

Mercer Super

In August 2024, the Federal Court ordered Mercer Super to pay a $11.3 million penalty after the fund admitted to making misleading statements about the sustainable characteristics of some of its investment options.

Vanguard

In September 2024, the Federal Court ordered Vanguard to pay a $12.9 million fine after it found that the firm had made misleading claims related to ESG screening for investments in one of its bond index funds.

Get stories like this in our newsletters.